2025-12-31 04:55:20 pm | Source: Motilal Oswal Financial Services Ltd

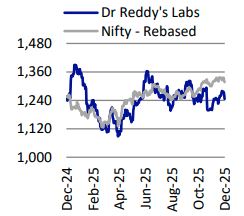

Neutral Dr Reddy`s Labs Ltd for the Target Rs. 1,250 by Motilal Oswal Financial Services Ltd

Growth levers in place, but near-term earnings drag limits upside

We recently met with the management of Dr. Reddy’s Labs (DRRD) to understand the company’s business prospects in detail:

- While increased competition in g-Revlmid would weigh on DRRD’s near-term performance, the company is implementing efforts to improve growth prospects over the next 2-3 years.

- Product-wise, Semaglutide and Abatacept present promising opportunities from FY27 and FY28 onwards, respectively.

- In addition, execution is underway to drive growth, with the aim of achieving double-digit performance in the remaining businesses – India, EU, Emerging Markets, and the PSAI segment.

- The company is also implementing cost-rationalization measures to support better margins going forward.

- Further, there is scope to utilize cash reserves (INR28b at the end of 1HFY26) for inorganic opportunities in its focus markets.

- While the all-round efforts of DRRD are encouraging, we estimate earnings to remain under pressure in FY27 due to limited levers available to offset the impact of reduced business from g-Revlimid. However, FY28 may witness an earnings recovery, driven by: a) improved growth in the base business, b) scaling traction in Semaglutide across key markets, and c) the potential approval of Abatacept.

- Excluding the Semaglutide/g-Revlimid and yet-to-be-accounted-for Abatacept opportunities, EV/EBITDA of the base business is 16x 12M forward EBITDA. We believe the current valuations adequately factor in the upside. We reiterate a Neutral stance (TP of INR1,250 on 19x 12M forward earnings).

Reinventing India’s growth: DRRD’s multi-lever strategy to outperform a slowing market

- Compared to mid-single-digit YoY growth in FY23/FY24, DRRD has progressed well in the Indian segment (16% YoY/12% YoY in FY25/1HFY26). It has been focusing on new launches while driving traction in existing products. FY25 YoY growth was partly led by the promotion/distribution of Sanofi vaccine portfolio.

- Specifically, over the past 12M, DRRD witnessed 5%/5%/2% growth from new launches/price hike/volume expansion in the Prescription (Rx) business.

- The company had 23/12 launches in FY25/1HFY26, respectively, and the launch momentum is expected to sustain over the medium term.

- Considering the overall slowdown in the Rx India industry’s growth (from 13- 15% YoY a decade ago to 8-9% currently), DRRD has revised its business strategy over the past couple of years by adding new growth drivers, such as on-patent innovative drugs, the Sanofi vaccine portfolio, and a tie-up with Nestle for nutraceutical and nutritional health brands, with the aim of outpacing industry growth in the Indian segment.

- DRRD continues to expand its innovative, on-patent portfolio in India through licensing and partnerships, having added several differentiated products in recent years, including Toripalimab, Tegoprazan, Colozo, and Vonoprazan.

- Toripalimab was launched in India in the same year as in the U.S., making India the third country globally to access this new biological entity. DRRD’s agreement with Shanghai Junshi Biosciences granted the company exclusive commercialization rights across 21 countries, with the option to expand into Australia, New Zealand, and nine other markets. Toripalimab replaces chemotherapy (gemcitabine/cisplatin) as the first-line treatment for metastatic or recurrent locally advanced NPC, in combination with these agents. GLOBOCAN 2022 reports over 120,000 new NPC cases globally and 6,519 in India. DRRD garnered INR800m revenue over the past year and aims to achieve annualized revenue of INR1b over the medium term from this product.

- The company launched Tegoprazan in India, following an exclusive partnership in CY22. Tegoprazan, a next-generation potassium-competitive acid blocker, is indicated for acid peptic disease (APD), which affects an estimated 38% of India’s population.

- Although the Sanofi portfolio is lower-margin due to DRRD’s limited role (promotion and distribution), it broadens the company’s offerings. Under this partnership, DRRD recently introduced Beyfortus, a novel RSV preventive therapy for infants.

- For the Nestlé portfolio, consumer research and regulatory processes are underway to enable commercial rollout. While Nestlé has seen limited traction in its consumer division, DRRD’s strong doctor reach is expected to improve portfolio performance.

- Further, DRRD has reorganized its MR structure and added ~1.5k MRs over the past two years, bringing the total to ~8k to enhance focus on the Rx segment of its Indian business.

- Profitability in the Indian business exceeds the company’s corporate margins.

- DRRD expects to grow at a double-digit rate and outperform the industry over the next 3-4 years.

NRT scale-up, footprint expansion, and brand investments to accelerate EU growth prospects

- DRRD is on track to transfer the nicotine replacement therapy (NRT) business from Haleaon, with about 30% of the business still managed by Haleaon. The entire shift is expected to be completed by the end of FY26.

- Notably, the portfolio is growing at a better-than-expected rate post the acquisition.

- ~65% of the NRT business comes from the EU and has experienced no price erosion. This provides cushion for growth, given that the non-NRT portfolio is subject to price erosion.

- The NRT portfolio demonstrates stronger margins compared to corporate margins.

- DRRD plans to invest in advertising for the NRT portfolio, which was previously considered a tail product by sellers and received limited focus. DRRD believes that there is strong consumer loyalty for smoking cessation products, and NRT is well-positioned for healthy growth through increased awareness and promotional activities.

- As far as the generics segment is concerned, DRRD continues to expand its EU portfolio by adding products sourced from its US lineup.

- In addition to increasing contracts for existing products, the company is strengthening its presence in the European region. With operations across 18 countries, DRRD is enhancing its offerings in these markets.

- DRRD expects double-digit growth in the EU segment over the next 3-5 years.

PSAI growth sustains on new API launches and CDMO recovery

- PSAI has been on a healthy growth path in FY25 and 1HFY26, supported by the launch of new products in the API sub-segment. Additionally, the CDMO segment is witnessing growth, partly on a low base of the past year.

- While certain one-offs impacted this segment’s gross margin in 2QFY26, it is expected to improve going forward, led by new launches and better operating leverage. Semaglutide: Multi-market launch pipeline on track; Canada approval by Mar-Apr’26

- Considering the additional information and clarifications sought by the Canadian regulatory authority, DRRD has submitted its response and is now awaiting approval. The regulator typically takes 5–6 months to provide feedback, though the timeline could be shorter if the review is expedited.

- The company is focusing on markets like India, along with emerging markets such as Brazil and Turkey, for the Semaglutide launch following patent expiry (Mar’26).

- In India, Novo Nordisk has launched an injectable weight-loss formulation, Wegovy, and an oral prescription formulation, Rybelsus, both based on Semaglutide. The company also introduced Ozempic this month, an injectable formulation for diabetes management, even though its patent is set to expire in three months.

- DDRD also plans to launch its Semaglutide injectable version for diabetes. Following regulatory approval, it plans to launch an injectable version for weight loss as well as an oral solid version.

- Overall, DRRD expects 12m pens to be sold in FY27.

Abatacept: High-complexity biosimilar with clear first-mover advantage for DRRD

- Abatacept is a recombinant fusion protein. Developing biosimilars for Abatacept has proven to be challenging due to its molecular complexity and regulatory requirements.

- Interestingly, the smaller market size of USD2.8b/USD912m (US/Ex-US) compared to other potential drugs like Keytruda, coupled with higher development costs (USD100-120m), has made Abatacept a lower priority for developing the biosimilar version for many companies.

- As a matter of fact, only DRRD and Kashiv Lifescience (Subs of Amneal) have crossed phase I trials to date.

- DRRD is confident in submitting the BLA of Abatacept by Dec’25, giving it a lead of 12-18M compared to any peer in developing the biosimilar version of Abatacept.

- The US intravenous (IV) and EU subcutaneous (SC) patents will expire in Dec’26. The IV version patent in the EU has already expired, while the US SC version patent will expire in Feb’28.

- DRRD intends to sell the IV version in the US following patent expiry, reducing the likelihood of litigation with the innovator.

- Accordingly, DRRD believes this to be a potential opportunity from FY28 onwards.

- Notably, ex-potential molecules (like g-Revlimid/bAbatacept, g-Semaglutide), DRRD expects single-digit YoY growth in the base business of North America.

Valuation and view

- We value DRRD at 19x 12M forward earnings to arrive at a TP of INR1,250.

- We expect earnings to remain stable over FY25-28, as a significant reduction in the g-Revlimid business (3QFY26 onward) is expected to be offset by new launches and a higher off-take of legacy products in key markets.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Ameenji Rubber trades higher on the BSE

ChatGPT outage disrupts Codex, Custom GPTs and works...

India's UPI to link up with Indonesia's payment syst...

Faalcon Concepts hits upper circuit on bagging work ...

NSE?s Rs 30,000 crore IPO faces questions after deca...

Apoorva Mukhija: The Rebel Kid Who Became a Voice of...

Weak monsoon may fuel inflation in India, hit rural ...

Euro Panel Products rises as its brand secures NABL ...

Trent shares sink 12 pc as Q1 revenue growth disappo...

Kutch Copper Ltd's 'Adani Copper' becomes London Met...