Neutral Craftsman Automation Ltd for the Target Rs. 4,641 by Motilal Oswal Financial Services Ltd

Strong end to the fiscal

Maintains FY26 guidance

* Craftsman Automation (CRAFTSMA)’s 4QFY25 performance was sharply ahead of our estimates, led by improved performance across all its segments.

* Given the better-than-expected performance in 4Q and an improved outlook, we raise our earnings estimates by 7%/6% for FY26/FY27. The key monitorables from here on include 1) the turnaround at Sunbeam and 2) stabilization of the greenfields. While these strategic initiatives appear to be in the right direction for the long run, they are likely to hurt returns for at least the next 12-15 months. The stock at 32x FY26E and 22x FY27E appears fairly valued. We reiterate our Neutral rating with a TP of INR4,641 (valued at 21x FY27E EPS).

Earnings beat led by improved performance across the board

* CRAFTSMA’s 4QFY25 revenue grew 40% YoY to INR11.5b, ahead of our estimate of INR9.4b. The revenue beat was driven by improved traction in all its key segments.

* YoY comparison is not meaningful given the Sunbeam acquisition.

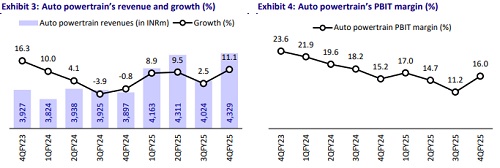

* The powertrain business posted 11% QoQ growth, the aluminum segment rose 10% QoQ, and the Industrial segment posted 17% QoQ growth.

* Given an improved pick up, the EBIT margin for the powertrain segment was up 220bp QoQ to 13.2%, was up 100bp QoQ to 8.8% for the aluminum segment, and expanded 550bp to 5.6% for the Industrial segment.

* As a result, consolidated margin improved 160bp QoQ to 14% (ahead of our estimate of 13%).

* Given the strong operational performance, PAT came in well ahead of estimates at INR275m (est of INR84m).

* For FY25, Craftsman posted 28% YoY growth in revenues to INR56.9b. Growth was boosted by acquisitions of Sunbeam and Frongberg.

* Organic growth for FY25 stood at 12% YoY. This was largely driven by 14% growth each in the Aluminium and Industrial segments and 8% growth in the powertrain segment.

* For FY25, the EBITDA margin sharply contracted by 510bp to 14.6% due to a weak demand environment, start-up costs of new facilities, and the acquisition of new companies highlighted above.

* As a result, PAT declined 28% YoY to INR2.2b for FY25.

* Management has incurred significant capex in the last two years worth almost INR16b, which has led to a negative FCF of INR8.2b in this period.

Highlights from the management interaction

* Management has maintained its guidance given in 3Q: revenue at INR70b for FY26E, EBITDA at INR11b, and EBIT at INR6.5-7b.

* The traditional powertrain business is likely to post double-digit growth in FY26 and expects margins to be better than even 4Q levels for FY26E.

* Sunbeam is likely to clock INR12b revenues in FY26E with margins of 8-10%.

* Standalone Al business is likely to clock a 20% revenue CAGR, driven by the ramp-up of plants at Bhiwadi and Hosur.

* Management has indicated that DRA can post double-digit growth going forward, viz., 8-10% for FY26 and higher in FY27.

* The storage solutions business is expected to grow in the high teens going forward.

Valuation and view

* Given the better-than-expected performance in 4Q and an improved outlook, we raise our earnings estimates by 7%/6% for FY26E/FY27E.

* Management is currently integrating multiple projects simultaneously, which include: 1) integration and restructuring of Sunbeam 2) ramp-up of new plants in Bhiwadi, Kothavadi, and Hosur, and 3) integration of Frongberg. While these strategic initiatives appear to be in the right direction for the long run, they are likely to hurt returns for at least the next 12-15 months, by which time we hope to expect: 1) a turnaround at Sunbeam, and 2) stabilization of the greenfields. If any of these timelines are not met, it will lead to further downside risk to our earnings. The stock at 32x FY26E and at 22x FY27E appears fairly valued. We reiterate our Neutral rating with a TP of INR4,641 (valued at 21x FY27E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412