Buy Suryoday Small Finance Bank Ltd For Target Rs. 226 by Centrum Broking Ltd

.jpg)

Balance Sheet Fortified, Growth Engine Reignited

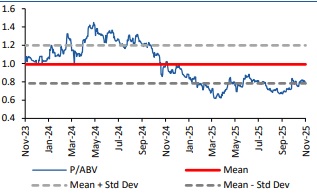

Suryoday SFB delivered steady improvement across key segments, with CE strengthening in the MFI portfolio and management indicating confidence in a stronger 2HFY26 driven by both growth and asset quality gains. The Retail Assets (RA) segment maintained healthy traction, particularly in the CV and mortgage portfolios. The bank received the full Rs313cr (third instalment) under the CGFMU scheme and continues to maintain nearly 100% coverage on its unsecured portfolio. The proceeds were utilized to write off NPAs in the MFI segment (Rs432cr), thereby reinforcing the balance sheet - GNPA/NNPA at 5.9%/3.8% vs. 8.5%/5.6% in Q1. On asset quality trends, MFI gross slippages moderated sharply to Rs170cr (from Rs237cr in Q1), with management guiding a further reduction to ~Rs175cr in H2. Similarly, the RA portfolio saw gross slippages ease to Rs36cr (vs Rs42cr in Q1), though PAR 30+ witnessed a marginal seasonal uptick – 10bps. Management reiterated that credit costs in the RA book will remain contained owing to its secured nature. In terms of mix, RA now accounts for 55% of the overall portfolio and MFI 45%. Overall, the improving momentum— especially in MFI—along with stabilizing asset quality and expected recovery in profitability (RoE to reach 12-13%) going ahead, supported by lower credit costs, easing CoF, and operating leverage, positions the bank well. Against this backdrop, we revise our valuation multiple upward from 0.8× to 1.0× on 1-year forward P/ABV, leading to a higher Target Price of Rs226 (earlier Rs178), while maintaining our BUY rating.

Core earnings remain strong

Interest income came in at Rs5.2bn (up 4.9% QoQ), while interest expenses rose ~5.4% QoQ amid strong deposit accretion. Consequently, NII stood at Rs2.58bn (up 4.5% QoQ). However, non-interest income declined (Rs0.8bn vs Rs1.1bn in Q1) sequentially, mainly due to lower PSLC income. Resultantly, NTI for the quarter stood at Rs3.4bn (down 5.0% QoQ), similarly PPOP moderated to Rs792mn, constrained by higher operating costs as the bank continues to invest in Tech and Retail expansion. CTI increased sharply to 76.6% (up 720bps QoQ). The bank’s PAT contracted 14% QoQ to Rs304mn, resulting in an ROA of around 0.8% and ROE of 6%. Going forward, operating leverage, recovery from written-off pools, and reduction in credit costs are expected to support gradual margin and return expansion.

GNPA declines sequentially; asset quality stabilizing

GNPA improved to 5.9% (vs 8.5% in Q1FY26), while NNPA stood at 3.8% (vs 5.6% in Q1FY26), reflecting benefits from the third CGFMU claim of Rs3.13bn received during the quarter. Of the Rs4.11bn NNPA, Rs3.78bn remains receivable under various CGFMU cohorts, indicating limited residual unsecured stress. Management guided that the bank is now fully provided on the unsecured book (including CGFMU cover), and going forward, asset quality pressure should remain contained with incremental provisioning largely for secured retail assets where performance continues to be stable.

Collection trends and portfolio mix improving

Collection efficiency in the current bucket remained stable at 98.6%, with the last 12-month originated portfolio at ~99.5%. Overall slippages eased sequentially from Rs2.8bn in Q1 to Rs2.1bn, led by improvement across both the unsecured and secured portfolios. Management highlighted that recoveries from the recent NPA pool and lower forward flows will drive credit cost moderation in H2FY26.

For More Centrum Broking Disclaimer https://www.centrumbroking.com/disclaimer/

SEBI Registration No.:- INZ000205331