Neutral Dabur India Ltd for the Target Rs. 535 by Motilal Oswal Financial Services Ltd

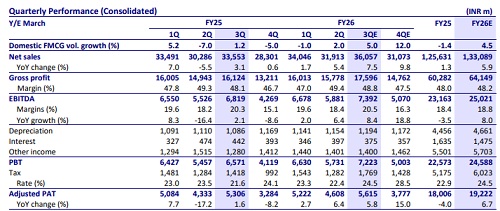

* We expect ~7.5 revenue growth, mainly backed by 5% volume growth in the India business. The growth will be led by the loading of the winter portfolio and some benefits of GST.

* GP margin is expected to expand 70bp YoY to 48.8% and EBITDA is expected to improve by 20bp YoY to 20.5%.

* Home and Personal Care (HPC) division is expected to perform well, driven by the oral, OTC, and Ethicals, home and skin care categories.

* International business is likely to deliver high single-digit CC growth, fueled by MENA, Turkey, Bangladesh, and the US Namaste business.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...