Neutral Dabur Ltd for the Target Rs.515 by Motilal Oswal Financial Services Ltd

Steady improvement in India; geopolitics weigh on RM costs and global business

* We interacted with Mr. Ankush Jain, CFO of Dabur India (Dabur) to discuss industry trends, the company’s growth outlook across verticals, global volatility, and its longterm strategies. Amid supply chain disruptions, Dabur’s international business has taken a hit (MENA accounts for 8% of consol. sales), which we believe could weigh on Dabur’s near-term consolidated performance.

* The company’s India business continues to witness sequential improvement in demand trends. Domestic business is expected to show better YoY growth in 4QFY26 as compared to 3QFY26. Global uncertainties have not impacted consumption as of now. The company has not taken any price hikes yet, though it continues to monitor commodity price movements closely. Looking ahead, management expects FY27 growth to be largely led by volume growth, subject to commodity volatility.

* Category trends remain broadly healthy across the portfolio. Dabur is seeing healthy growth momentum in oral care (~16% market share) and hair care (strong doubledigit growth) segments. Healthcare demand remains relatively muted, but there is sequential improvement. In home care, growth is expected to move toward high single digits, aided partly by a favorable base. The foods portfolio is growing steadily, while beverages are expected to grow in low single digits in the near term. A favorable outlook for beverages in FY27 is well supported by a weak base.

* On profitability, management expects steady margins in the near term. The company may consider price hikes mid-April onward if input costs remain elevated. Packaging material (PM) costs account for ~15% of sales and 25-30% of total raw material (RM) costs. EBITDA margins are expected to expand YoY in the near term.

* Quick commerce (QC) continues to gain traction and now contributes 4-5% of India revenue (50% of ecomm), accounting for roughly half of total ecommerce sales. The growth trajectory remains strong (30-40%) in QC channel.

* Dabur posted muted growth in FY25 (1.3%) and 9MFY26 (4%), with mid-single-digit growth expected in 4Q despite high-single-digit growth in India. Given its leadership transition from Mr. Mohit Malhotra to Mr. Herjit Bhalla, we will watch for any strategic priority changes by the new CEO. Apparently, Mr. Malhotra will continue to be part of Dabur and may look after M&A, strategy and international fronts.

* Domestic macro indicators are supporting a gradual consumption recovery, though persistent execution challenges keep us cautious. Factoring in near-term headwinds in Dabur’s international markets, we trim our EPS estimates by 2-3% and maintain Neutral with a TP of INR515 (40x Mar’28E EPS).

Geopolitical uncertainties to weigh on consol. performance in near term

* Dabur stated that supply-chain disruption has emerged across key shipping routes, particularly around the Red Sea and the Strait of Hormuz, affecting product movement in the GCC markets.

* Moreover, the company is seeing softened consumption trends in the region as residents remain indoors and the tourist population has declined.

* From a revenue mix perspective, the MENA region contributes ~8% of Dabur’s consolidated revenue, while Turkey accounts for ~3-4%.

* While the company entered the quarter with strong momentum, the ongoing conflict has led management to moderate growth expectations for international business.

* Given the emerging headwinds, management has lowered its near-term consolidated growth guidance from high single digits to mid-single digits, largely reflecting the slowdown in international markets.

India FMCG business continues to see sequential improvement

* Rural demand continued to outperform urban demand. However, the ruralurban growth gap has narrowed to ~250bp from ~500bp earlier, indicating a gradual improvement in urban demand. The company is seeing a recovery in urban demand.

* Domestic FMCG growth stood at 6% in 3QFY26, which management expects to improve ahead. Encouragingly, as per Dabur, the first 10 days of March have not shown any material slowdown in consumer demand.

* The company has not implemented price hikes currently but continues to monitor commodity price movements.

* Management expects growth in FY27 to be led by volume, subject to commodity volatility.

Healthy growth across categories

* Oral Care: Dabur maintains a ~16% market share in oral care (No. 2 player in the space), with household penetration of ~52-53%, implying every second household in India uses a Dabur oral care product. Management sees significant headroom for further market share gains.

* Hair Care: The segment is witnessing strong double-digit growth, supported by a structural shift in consumer preference from coconut oil toward perfumed hair oils, which also carry higher margins for the company. Coconut hair oil makes up 20-25% of its overall hair oil mix.

* Healthcare: The category remains relatively muted but is expected to see gradual improvement ahead. Dabur indicated that select over-the-counter (OTC) brands like Pudinhara and Honitus are reportedly showing sequential improvement.

* Home Care: While the category had previously been seeing low single-digit growth, management now expects it to reach near high single digits. That said, the current improvement is partly due to a favorable base; in the previous year, there were supply issues in GT. The company is continuing to see market share gains in this category.

* Foods & Beverages (F&B): The foods portfolio continues to grow at a healthy pace. In the near term, Dabur expects beverages to grow at a low single-digit rate, while the combined F&B category is projected to grow at a mid-single digit rate. For FY27, management anticipates a better trajectory for F&B category, noting that the base is quite favorable due to the poor summer performance in the previous year. Management further noted that the beverages portfolio should at least grow in mid-single digits.

Dabur expects steady margins in near term

* Dabur has not increased prices currently, as the company carries FG/RM inventory, along with healthy inventory at trade channel. However, management indicated that price hikes may be considered from mid-April onward if crude-linked input costs remain elevated.

* PM costs account for ~15% of sales and 25-30% of total RM costs. Earlier estimates assumed 2-2.5% RM-PM inflation (excl. coconut); hence, the company was expecting a limited price hike requirement in FY27. However, given current geopolitical volatility, there could be a change in the price hike outlook.

* EBITDA margin is expected to improve in the near term; however, commodity volatility can change the outlook for FY27.

Quick commerce makes up 4-5% of India business sales

* QC continues to gain traction and currently contributes 4-5% of Dabur’s India revenue. It now accounts for ~50% of total e-commerce sales.

* Management highlighted that QC and e-commerce channels typically skew toward premium product formats (bottles, larger packs) compared with general trade, which is largely driven by sachets.

* Dabur continues to focus on strengthening its distribution reach. It expanded its total reach (urban + rural) to over 8.5m outlets, making it the second-most distributed FMCG company in India.

Valuation and view

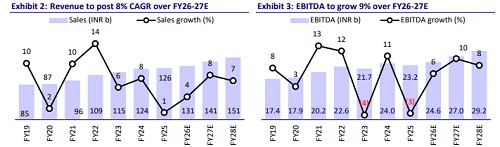

* The company has been reporting muted sales growth over the past two years. After delivering 1.3% growth in FY25, revenue growth improved modestly to 4% in 9MFY26. Management is guiding for mid-single-digit growth in near term (high-single-digit growth for India).

* Considering leadership changes from Mohit Malhotra to Herjit Bhalla, we will watch for any strategic priority changes by the new CEO. Apparently, Mr. Malhotra will continue to be part of Dabur and may look after M&A, strategy and international fronts.

* We remain positive on consumption recovery, supported by improving domestic macros, but cautious on global uncertainties. However, Dabur’s consistent weak execution, despite macros turning positive, is concerning, in our view. The stock has remained range-bound over the last five years. Factoring near-term headwinds in Dabur’s international markets, we trim our EPS estimates by 2-3% and maintain Neutral with a TP of INR515 (40x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041