Buy Godrej Consumer Products Ltd for the Target Rs. 1,450 by Motilal Oswal Financial Services Ltd

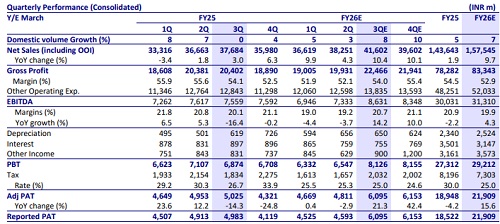

* We expect 8% volume and revenue growth in the India business. Soaps portfolio (1/3rd of India) impacted in 2Q due to GST will see improvement. Home care expected to deliver double-digit growth.

* We model revenue growth of (-2%)/23%/(-5%) in Indonesia/ GAUM and other international businesses.

* India business gross margins expected to be stable YoY at 54.8 while EBITDA margin expected to improve 180bp YoY to 24.4% on a favorable base (22.7% in 3QFY25). Indonesia and other international business EBITDA are expected to decline, while GAUM EBITDA is expected to rise in double digits. Consolidated EBITDA is expected to grow 14% YoY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Retail Sector Update : QSR - QSR at an inflection point; risk-reward favorable By Motilal O...