Buy Siemens Energy India Ltd for the Target Rs.3,300 by Motilal Oswal Financial Services Ltd

Ramping up execution and margin performance

Siemens Energy India (ENRIN) reported 2QFY25/1HFY25 financials, which were better than our estimates. The comparable numbers for the previous period are not available. Revenue growth improved 24% QoQ and EBITDA margin stood strong at 19.1% for the quarter, driven by strong margins in the power transmission segment. Margins were soft in the power generation segment. EBITDA margin has been continuously improving for the company for the past two quarters even after adjusting one-off items. Based on 1HFY25 performance, we raise our estimates by 13%/6%/8% for FY25E/FY26E/FY27E to bake in improved execution and margin in the power transmission segment. We expect ENRIN to continue to benefit from a strong addressable market in T&D as well as its planned capacity expansion in the transmission segment. Accordingly, we estimate a CAGR of 27%/29% in revenue/PAT over FY25-27. Retain BUY with a revised TP of INR3,300 (from INR3,000), based on 60x Sep’27E EPS.

Strong 1H performance

ENRIN reported a strong set of results. Revenue for 2QFY25 stood at INR18.9b, led by strong QoQ growth across segments. EBITDA stood at INR3.9b, growing 7% QoQ, while margin for the quarter contracted 300bp QoQ. Other income remained low, though we expect other income to increase going forward. The company has receivables from Siemens Ltd, which would aid other income once received. PAT increased 6% QoQ. For 1HFY25, revenue/EBITDA/PAT stood at INR34b/INR6.9b/INR4.8b, while EBITDA margin stood at 20.4%, which was higher than our previous FY25 estimates. OCF stood strong at INR1.9b and capex stood at INR922m during 1HFY25.

Segmental performance

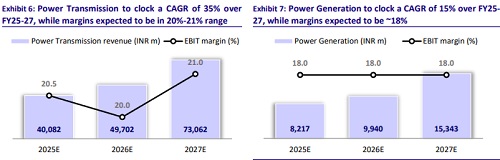

Power Transmission segment’s 2Q revenue increased 21% QoQ to INR10.1b, while EBIT stood at INR2.1b, leading to 10bp QoQ EBIT margin expansion to 20.3%. For 1HFY25, Power Transmission segment’s revenue/EBIT stood at INR18.5b/INR3.8b, while EBIT margin stood at 20.3%. Power Generation segment’s revenue rose 28% QoQ to INR8.7b, while EBIT declined 11% QoQ to INR1.3b, leading to a margin contraction of 650bp QoQ to 14.9%. For 1HFY25, Power Generation segments’ revenue/EBIT stood at INR15.4b/INR2.7b and EBIT margin stood at 17.7%.

Outlook remains healthy across segments

We expect ENRIN’s Power Transmission segment to grow much faster, as it is well-placed to benefit from planned investments of INR3t in T&D over FY25-30, primarily in HV lines of 400kV and 765kV, given their crucial role in inter-state transmission lines. Siemens is among the few players with a presence in highvoltage lines up to 765kV and is, hence, expected to benefit from planned investments. Additionally, state-wise ISTS strengthening initiatives are expected to drive investments worth INR120b in the sector. Along with this, ENRIN will also focus on HVDC projects, particularly on VSC technology. Power Generation segment of ENRIN focuses on industrial gas turbines and we expect it to be more dependent on private sector capex.

Financial outlook

Our assumptions for revenue growth take into account doubling of capacity for transformers and expansion in GIS, along with normal business growth for turbine business. We revise our FY25E estimates to factor in 1H performance and expect revenue/EBITDA/PAT CAGR of 27% over FY25-27E, led by strong growth across power transmission (35% CAGR) and power generation (15% CAGR). We expect EBITDA margin of 20.7%/20.5%/21.2% for FY25E/26E/27E.

Valuation and view

ENRIN is currently trading at 77.1x/55.4x P/E on FY26E/27E EPS. We increase our estimates by 13%/6%/8% for FY25E/26E/27E to factor in 1H performance. We value the stock at 60x on Sep’27E EPS and maintain our BUY rating with a revised TP of INR3,300.

Key risks and concerns

Key risks to our thesis can come from a slowdown in ordering and supply chain issues impacting margin.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412