Buy Canara HSBC Life Insurance Ltd for the Target Rs 180 by Motilal Oswal Financial Services Ltd

Consistent outperformer with improving profitability

* We had initiated coverage on Canara HSBC Life Insurance (CANHLIFE) in Jan’26 as a multi-year compounding story, consistently outperforming industry growth over the past few years with an alpha of 700-800bp, resulting in a private market share of 2.6% in FY26 (vs. 2.2% in FY22).

* While near-term growth has moderated (Apr’26 APE growth of 11% YoY vs. 38% YoY growth for the industry) amid product mix recalibration and implementation of revised underwriting processes, we expect the insurer to maintain a 20% APE growth trajectory.

* The insurer benefits from the strong operational integration within the Canara Bank ecosystem (72% of APE in FY26) with multiple initiatives underway to improve the branch activation (54% in FY26) and harness the underpenetrated opportunity (<2% penetration within Canara Bank’s ~85m customer base). Further, the exclusive relationship with the expanding HSBC network (14% of FY26 APE) and the gradual expansion of the agency provide a strong growth lever. * The aggressive shift towards traditional products, robust operational efficiency, and rising rider attachments have led to a 320bp YoY expansion in FY26 VNB margin (to 22.4%), despite GST-related headwinds and investments toward agency scale-up. We expect the VNB margin to improve 10bp/50bp in FY27/ FY28, reaching 23% in FY28 with the impact from rising traditional contribution apart from agency channel scale-up.

* Given relatively disciplined payout structures (commission ratio of 6.4% in FY26 – second lowest in the industry) and strong operational positioning within banca ecosystems, the possible commission regulations could potentially improve competitive positioning and partnership accessibility over time rather than structurally impairing the franchise.

* With one of the most underpenetrated PSU-bank funnels and clear visibility on branch activation, product mix upgrades, and operating leverage, we expect the company to deliver high-teens operating RoEV going ahead despite near-term ITC and agency drag. We estimate a CAGR of 20%/22% in APE/VNB. Maintain BUY with a one-year TP of INR180 (based on 1.7x FY28E P/EV).

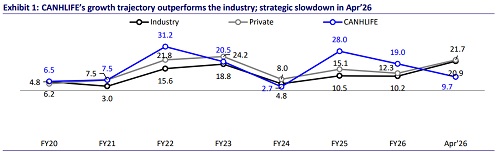

Poised for an industry-leading growth momentum

* CANHLIFE has grown better than the industry with an FY22-26 APE CAGR of 16% compared to 11% for the industry, resulting in market share gain from 2.4% in FY22 to 2.6% in FY26 among private players. Individual APE continues to outperform the industry with a five-year CAGR of 20%.

* The GST exemption (implemented from 22 Sep’25) further boosted the growth momentum for the insurer with total APE growth of ~26% for 2HFY26 compared to industry growth of ~20%.

* However, the insurer experienced a slowdown in momentum in Mar’26/ Apr’26, with APE declining 4% YoY/rising 11% YoY vs. the industry growth of 20%/38%. The slowdown was largely because of a strategic transition towards traditional products over ULIPs, as the focus has increased on balancing growth with long-term sustainability, predictability, and quality of earnings.

* Additionally, CANHLIFE implemented underwriting-related operational guidelines required by IRDAI from Apr’26, which possibly led to temporary policy issuance delays and business deferral.

* With customer preference robust for linked products through most of FY26, the focus on non-par, protection, and annuity products impacted near-term growth for the company. We expect the moderation to subside and APE to grow at a FY26-28 CAGR of 20%, likely outperforming the industry by 400-500bp

Maintaining high-teens operating RoEV

* CANHLIFE’s EV sensitivity has improved significantly recently owing to the expansion in hedging capacity. After the launch of non-par business in 2018, sensitivity was higher due to lower capacity of hedging, though the business has grown over the years, contributing 19% of APE in FY26.

* Generally, EV of life insurers is inversely related to the change in the reference rate. However, the high share of ULIP (~51% in FY26) for CANHLIFE has resulted in a positive relation with a change in the reference rate for the insurer.

* With better hedging and strong headroom for improvement in VNB margin, we expect the insurer to maintain operating RoEV in the range of 18-19%.

Valuation and view

* CANHLIFE offers a rare multi-year compounding opportunity anchored in a structurally improving banca engine, rising contributions from premiumized HSBC flows, and disciplined agency expansion.

* CANHLIFE enters its listed journey at a point where both its distribution architecture and financial model are undergoing structural strengthening. The recent exemption of GST from life insurance has given a boost to the growth trajectory of the insurer. The differentiated dual-bank partnership with mass scale from Canara Bank and premium affluence from HSBC creates a distribution backbone that only a few private life insurers possess.

* The launch of the agency channel, while margin-dilutive in the near term, adds distribution resilience and long-term optionality.

* With one of the most underpenetrated PSU-bank funnels and clear visibility on branch activation, product mix upgrades, and operating leverage, we expect the company to deliver high-teens operating RoEV going ahead despite near-term ITC and agency drag. We estimate a CAGR of 20%/22% in APE/VNB. Reiterate BUY with a one-year TP of INR180 (based on 1.7x FY28E P/EV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412