Neutral Power Grid Corporation of India Ltd for the Target Rs 305 by Motilal Oswal Financial Services Ltd

FY27/28 guidance maintained

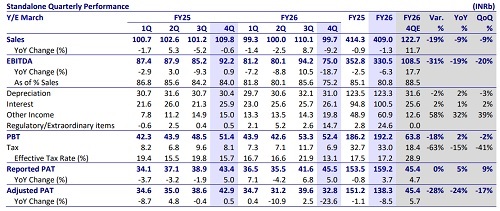

* Weak 4QFY26: Power Grid Corporation (PWGR) reported a standalone revenue of INR99.7b, 19% below our estimate. Reported PAT was in line with our estimate at INR45.5b (boosted by a deferred tax asset of INR52.8b, while there was a negative movement in the regulatory deferral balance amounting to INR38b). APAT was significantly below our estimate at INR32.7b. Standalone FY26 Revenue/EBITDA stood at INR409/330b (- 1.2/6.3% YoY), while Consol. Revenue/EBITDA stood at INR439/352b (- 5/11% YoY).

* Key things we liked about the result:

1) FY26 capex/capitalization stood at INR399/282b, surpassing guidance of INR350b/250b

2) Management reiterated FY27/28 capex guidance of INR370/450b and capitalization of INR300/350b, while indicating potential upward revisions ahead

3) 22 HVDC projects are at various stages of bidding and planning (HVDC capacity of ~127GW)

4) the company highlighted a long-term opportunity pipeline of ~INR15t across renewable energy evacuation, the Brahmaputra hydro corridor, and OSOWOG interconnections (India–Sri Lanka, India–Singapore, etc.).

* Key monitorables:

1) PWGR won 9 out of 28 TBCB projects awarded during the year, implying a market share of 32%, below its historical share of 50- 60%

2) EBITDA declined YoY in FY26 as several regulated tariff mechanism (RTM) projects crossed the 12-year mark

3) Bid wins in the annual expected bid pipeline of INR800-1,000b; incremental transmission demand arising from emerging load centers such as data centers and green hydrogen projects.

* Valuation : We reiterate our Neutral rating and derive our TP of INR305 based on Dec’27 BVPS and a P/B multiple of 2.5x.

Miss on EBITDA and PAT estimate Standalone (SA) Performance:

* PWGR reported SA revenue of INR99.7b (-9% YoY & QoQ), missing our estimate by 19%.

* SA EBITDA came at INR75b (down 19% YoY/20% QoQ), 31% below our estimate, mainly due to revenue coming in below our estimate and elevated other expenses.

* SA’s reported PAT came in line with our estimate at INR45.5b (+5% YoY, +9% QoQ), boosted by a deferred tax asset of INR52.8b.

* Deferred tax balances have been re-measured at the new applicable tax rates, following the company's expected transition to the new tax regime under the Income Tax Act, 2025.

* There was a net negative movement in the regulatory deferral balance amounting to INR38b.

* APAT stood at INR32.7b, significantly below our estimate.

Consolidated Performance:

* PWGR’s consolidated revenue for 4QFY26 came in at INR116.7b (-5% YoY), while reported PAT grew ~10% YoY to INR45.5b.

Other Matters:

* The Board of Directors approved the payment of final dividend of INR1.25/share, translating into a full-year dividend of INR9/share.

Valuation and view

We derive our TP of INR305 for PWGR based on Dec’27 BVPS and a P/B multiple of 2.5x

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412