Buy Amber Enterprises Ltd for the Target Rs 8,450 by Motilal Oswal Financial Services Ltd

Commodity headwinds amid strong demand

Amber Enterprises (AMBER)’s 4QFY26 result was ahead of our estimates, driven by a better-than-expected performance across allsegments. RAC industry demand remained strong, and the company outperformed industry growth in FY26. The electronics segment has benefited from the recent acquisitions, and its marginsremained in double digits. However, high commodity prices could weigh on FY27 margins. The company continues to invest in capex across segments, benefits of which will start yielding from FY27-28. We factor in improved demand and higher prices in RAC segment and lower margins across divisions amid commodity pressure. We cut our estimates by 6%/2% for FY27/FY28. Retain BUY with a revised DCF-based TP of INR8,450

Strong set of results; beat across revenue, EBITDA and Rep. PAT

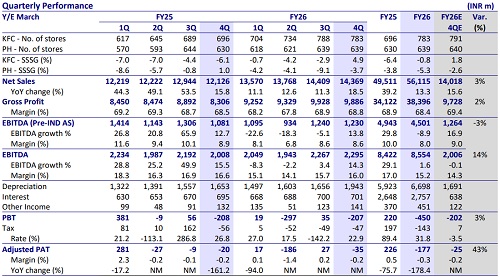

For 4QFY26, consolidated revenue grew 11% YoY to INR41.5b, 10% above our estimate. This was supported by growth seen across all the segments. Gross margin expanded 220bp YoY to 18.8% (vs. est of 17.4%). Absolute EBITDA increased 22% YoY to INR3.6b, beating our estimates by 22%, while margins expanded 70bp YoY to 8.6% (vs est of 7.8%) due to better-than-expected margins across all segments. Adj PAT declined 39% YoY to INR704m vs. our estimate of INR1.1b, mainly due to losses booked in a subsidiary’s JV. Adjusting that, PAT increased 16% YoY to INR1.3b (~15% above our estimates). For FY26, revenue/EBITDA/PAT grew 22%/25% YoY, adj. PAT declined 11% YoY, and EBITDA margin expanded 10bp YoY. OCF declined 66% YoY to INR2.4b mainly due to higher working capital requirements, while the company reported a net FCF outflow of INR10b due to higher capex done during the year toward capacity expansion

Outlook across segments remains strong

The company expects RAC industry growth to recover to ~12-13% YoY in FY27 (vs. flat trends in FY26), with 1QFY27 industry volumes likely up ~20% on a weak base, while Amber is expected to broadly grow in line with industry demand, supported by deeper ODM integration and higher finished goods contribution. Electronics division is targeted to deliver ~40% growth in FY27, driven by expansion across PCBA, PCB, industrial automation, automotive and power electronics. In railways and defense, the company expects revenue to grow ~30-35% YoY, backed by the INR26b+ order book, metro expansion, defense opportunities and the scale-up of higher-value products such as doors, gangways and data center cooling.

Compressor QCO impact remains limited

The recent compressor QCO notification was aimed at tightening localization and quality standards for RAC compressors, particularly below 2 tons, where the government is encouraging domestic manufacturing. While the move initially raised concerns around potential supply shortages for the RAC industry, the government subsequently allowed imports of up to 30% of prior-year imported volumes to bridge any near-term gaps. Current domestic RAC compressor manufacturing capacity stands at ~7.5-8.0m units, while it stands at ~10m units including Highly’s expansion. Alongside the government’s allowance for imports of up to 30% of prior-year volumes (~4m units), the available supply ecosystem appears broadly sufficient to support the industry’s expected ~12-13% growth trajectory. Domestic capacity addition announcements by GMCC, Highly, LG, Daikin and Mitsubishi will further improve India’s compressor manufacturing ecosystem. Amber continues sourcing compressors through long-term agreements with GMCC, LG, alongside other suppliers, limiting direct operational impact.

Key risks and concerns

Key risks and concerns include lower-than-expected demand growth in the RAC industry; a change in BEE norms making products costlier; a change in the announced capex policy; and increased competition across the RAC, mobility, and electronics segments.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412