Sell Deepak Nitrite Ltd for the Target Rs 1,450 by Motilal Oswal Financial Services Ltd

Stable operating performance amid persistent macro headwinds Operating performance beats estimate

* Deepak Nitrite (DN) reported a healthy operating performance, with EBIT growing 18% YoY to INR3.1b, led by 20% YoY EBIT growth in the Phenolic segment. This growth was driven by strong pricing gains and stable plant operations, while Advanced Intermediate’s EBIT declined 25% YoY.

* While near-term performance may continue to see some pressure amid persistent industry-wide challenges and evolving geopolitical developments, the impact on overall performance is likely to remain limited, supported by continuous process refinements and cost optimization initiatives.

* Factoring in the better-than-expected margin in 4QFY26, we increase our FY27/FY29 estimates by 7%/9% and expect a CAGR of 11%/19%/23% in revenue/EBITDA/PAT over FY26-28. We value the stock at 24x FY28E EPS to arrive at our TP of INR1,450. Reiterate Sell.

The intermediate segment continues to face margin headwinds

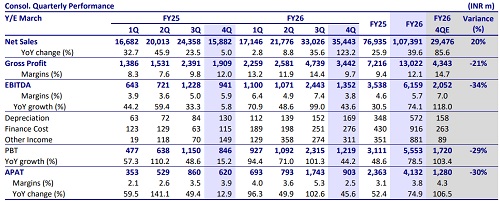

* DN’s 4Q revenue declined 3% YoY to INR21.2b (est. in line), primarily due to a 7% YoY decline in phenolics to INR14.3b, while advanced intermediates’ revenue grew 8% YoY to INR7.1b.

* Gross margin came in at 34.9% (up 430bp YoY), while EBITDAM stood at 17.7% (up 320bp YoY). Employee costs as a % of sales stood at 5.2% (vs. 4.7% in 4QFY25), while other expenses stood at 12% (vs. 11.4% in 4QFY25).

* EBITDA grew 19% YoY to INR3.7b (our est. INR2.5b), and EBIT for Phenolics grew 20% YoY, while EBIT for advanced intermediates declined 25%.

* EBIT margin for advanced intermediates contracted 210bp, while EBIT margins for Phenolic expanded 440bp YoY to 20%.

* Adjusted PAT stood at INR2.2b (est. of INR1.5b), up 8% YoY.

* In FY26, DN’s revenue/EBITDA/adj. PAT declined 5%/10%/20% to INR78.9b/ INR9.8b/INR5.6b.

* CFO stood at INR5.4b as of Mar’26 compared to INR6.2b as of Mar’25.

Valuation and view

* The global chemical industry continues to face a challenging operating environment characterized by persistent global challenges, uneven recovery in demand, and the West Asia crisis, leading to disruption in established supply chains, challenges to logistics, and volatility of crude oil prices.

* The company’s focus on continuous process refinements and cost optimization initiatives is expected to drive operational performance and fortify its competitive positioning. Further commercialization of new products, along with the commercialization of MIBK/MIBC projects by early 2QFY26, is also expected to drive earnings growth.

* Factoring in the better-than-expected margin in 4QFY26, we raise our FY27/FY29 estimates by 7%/9% and expect a CAGR of 11%/19%/23% in revenue/EBITDA/ PAT over FY26-28. We value the stock at 24x FY28E EPS to arrive at our TP of INR1,450. Reiterate Sell.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412