Buy KEC International Ltd for the Target Rs 630 by Motilal Oswal Financial Services Ltd

Performance impacted by disruptions

KECI posted weak results in 4QFY26, affected by disruptions in supplies and dispatches due to the West Asia crisis, coupled with higher freight costs and RM prices. Order inflow for FY26 stood almost flat YoY at INR252b due to weakness in domestic T&D inflows, particularly after the PGCIL ban. Going ahead, we expect KEC to continue to ramp up execution across T&D and civil projects, while margin performance in the near term may remain impacted by labor issues and higher RM prices. We thus reduce our margin estimates and cut our EPS estimates by 19%/21% for FY27/28. We maintain BUY with a revised TP of INR630, based on 18x P/E Mar’28E earnings

Weak set of results

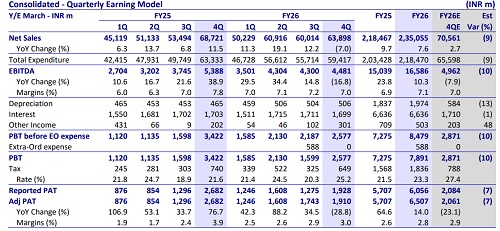

KECI reported weaker-than-expected 4QFY26 performance, with revenue/EBITDA/PAT coming in below our estimates. Revenue declined 7% YoY to INR64b, while gross margin contracted 200bp YoY to 20.2%. Absolute EBITDA declined 17% YoY to INR4b, with EBITDA margin at 7%. Due to lower-thanexpected execution, adjusted PAT declined 29% YoY to INR2b. Order inflow stood at INR60b during the quarter, taking the closing order book to INR363b, while OB plus L1 position stood at INR400b. For FY26, revenue/EBITDA/PAT increased 8%/10%/14% to INR235b/INR17b/INR7b, with EBITDA margin expanding 10bp YoY to 7.1%. However, cash flows remained weak, with OCF outflow at INR6b (vs. inflow of INR7b in FY25) due to higher NWC and FCF outflow at INR10b (vs. inflow of INR5b in FY25) owing to elevated capex.

Overall performance was impacted by geopolitical disruptions

KECI’s 4QFY26 performance remained impacted by geopolitical disruptions in the Middle East, freight inflation, labor shortages and supply chain disruptions, which are expected to continue affecting near-term execution and profitability. Net working capital remained high at 137 days, while net debt stood at INR67b due to delayed collections, higher inventory amid delayed dispatches in Dubai and strategic inventory build-up in cables, raw materials and steel due to volatile prices. Receivables were also impacted by slower collections in the water business and delays from certain large clients. While near-term challenges persist, recovery in execution and collections remains critical for improvement in margins and working capital going forward.

Financial outlook and valuation

We cut our estimates by 18%/21% for FY27/28 to factor in lower revenue and margins. We expect a CAGR of 16%/15%/19% in revenue/EBITDA/PAT over FY26-28. This will be driven by 1) order inflow growth of 21% on a strong prospect pipeline; 2) stable EBITDA margin at ~7% for FY27E/28E; and 3) stable NWC. KECI is currently trading at 17.2x/14x on FY27E/28E EPS. We maintain BUY with a revised TP of INR630 (from INR750 earlier) based on 18x P/E Mar’28E earnings.

Key risks and concern

A slowdown in order inflows, higher commodity prices, an increase in receivables and working capital, and heightened competition are some of the key risks that could potentially affect our estimates.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412