Buy Zydus Wellness Ltd for the Target Rs 600 by Motilal Oswal Financial Services Ltd

Soft seasonal demand; new initiatives doing well

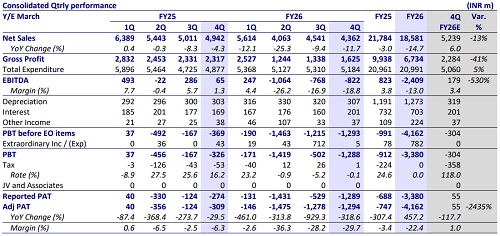

* Zydus Wellness (Zydus)’s consol. sales grew 63% YoY to INR14.8b in 4QFY26. Domestic business revenue grew 2% YoY in 4QFY26 (est. 8%; 2% in FY26), impacted by delayed summer and unseasonal rainfall in North and East India. Glucon-D and Nycil revenues declined 10% YoY in 4QFY26 (-19% in FY26). Management expects an improvement in seasonal product demand from May onwards; a harsh summer can lead to high double-digit growth.

* The non-seasonal portfolio remained healthy, with Everyuth revenue rising 40% YoY (22% in FY26) and the Food & Nutrition revenue rising 9% YoY (15% in FY26). Within the Food & Nutrition segment, Nutralite continued to report double-digit growth, Complan recorded near double-digit growth, while Sugar Free delivered low- to mid-single-digit revenue growth. RiteBite Max Protein continued to deliver healthy volume and value growth. International business revenue (including Comfort Click) rose 31% YoY in 4Q.

* EBITDA margin dipped 260bp YoY to 18.2% (est. 19.3%) due to weak seasonal portfolio performance (high-GM business). RiteBite’s EBITDA margin improved to double digits (from breakeven at acquisition). CC margins remain in line with company expectations. We model the domestic EBITDA margin of 14.5% for FY27 and 15.5% for FY28. International business’s EBITDA margin is likely to remain at 14-15%; we model a similar margin.

* The stock is at 23x FY27 and 18x FY28 EV/EBITDA. We model ~11% domestic revenue CAGR and ~20% EBITDA CAGR over FY26-28E. On a consolidated basis, we model ~26% revenue CAGR and 37% EBITDA CAGR. Zydus’ recent initiatives around RiteBite and CC are trending at an exciting pace, both in revenue and operating margin.

* Based on SoTP, we value India at 27x FY28E EV/EBITDA and International (Comfort Click) at 18x FY28E EV/EBITDA to arrive at our TP of INR600 (implied consolidated 23x EV/EBITDA and 30x P/E at FY28). Reiterate BUY

Highlights from the management commentary

* The company stated that geopolitical disruptions had a limited impact on operations due to proactive mitigation measures.

* Seasonal brands such as Glucon-D were impacted by delayed summer conditions and unseasonal rains, particularly in North and East India. Management highlighted that last year had an early summer, whereas this year witnessed a delayed summer onset.

* The consolidated tax rate for FY27 and FY28 is expected to remain around 25%.

* Management reiterated the long-term EBITDA margin aspiration of 17–18% under normal seasonal conditions.

* The company expects Comfort Click to become EPS accretive in FY27.

Valuation and view

* We broadly maintain our EBITDA estimates for FY27 and FY28.

* The valuation multiple is currently low given its low earnings delivery in the past decade (10-year CAGR of 7-8%). With stability in the core business (took the initial period to stabilize a sizable acquisition) and exciting new growth engines, we expect Zydus to deliver superior earnings growth vs. the past.

* The stock is at 23x FY27 and 18x FY28 EV/EBITDA. We model ~11% domestic revenue CAGR and ~20% EBITDA CAGR over FY26-28E. On a consolidated basis, we model ~26% revenue CAGR and 37% EBITDA CAGR. Zydus’ recent initiatives around RiteBite and CC are trending at an exciting pace, both in terms of revenue and operating margin.

* Based on SoTP, we value the India business at 27x FY28E EV/EBITDA and the International one (Comfort Click) at 18x FY28E EV/EBITDA to arrive at our TP of INR600 (implied consol. 23x EV/EBITDA and 30x P/E at FY28). Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412