Neutral Vodafone Idea Ltd for the Target Rs 10 by Motilal Oswal Financial Services Ltd

Everything must go right for the long-term revival

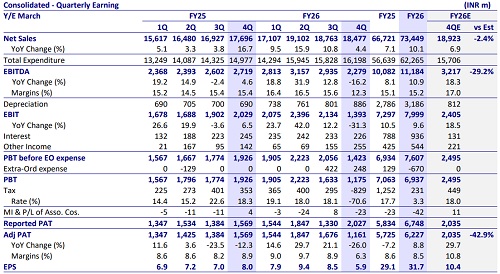

* Vodafone Idea’s (Vi) 4QFY26 pre-IND AS EBITDA rose ~3% QoQ (+5% YoY) to INR24.3b (vs. our est. INR23.7b), driven by subscriber mix improvement (customer ARPU up ~2% QoQ to INR190), stabilization of the subscriber base (incl. M2M subs), and robust cost control (+65bp QoQ, 60bp beat).

* Wireless revenue grew ~3% YoY in FY26, driven by ~8% YoY growth in wireless ARPU to INR170, as paying subs base declined ~5.4m YoY (8.7m YoY decline in consumer SIMs excl. M2M).

* FY26 pre-IND AS EBITDA remained broadly stable YoY at INR92.2b, as margins contracted ~55bp YoY to 20.5%, due to network rollouts.

* Management reiterated its guidance of increasing pre-IND AS EBITDA by 3x to ~INR270b by FY29, driven by its capex plans of ~INR450b over FY26-29.

* Further, management believes the company’s internal cash generation (INR600b cumulatively over FY26-29), bank funding (INR250b funded and INR100b letter of credits or LCs), settlement agreement with Vodafone Plc, potential income tax refunds, and promoter infusion from Aditya Birla Group (ABG; ~INR100b put together) should be sufficient to meet the ~INR1.05t cash requirement over FY26-29 toward capex (INR450b), GoI payments (~INR500b), and servicing interest on bank loans (~INR100b).

* Compared to management’s aggressive estimate of ~INR600b cumulative cash EBITDA over FY26-29 (vs. INR92b annual run rate), we build in lower ~INR345b cumulative cash EBITDA over the same period, which necessitates the need for an expedited and larger fund raise to support the company’s capex plans.

* Further, we believe Vi’s revival hinges on:

1) sustained tariff hikes or a change in tariff construct,

2) stabilization in consumer wireless subs trends,

3) more rational competition on subscriber acquisition

4) continuation of a benign regulatory regime, with further relief on spectrum payments.

* We note that not all of these variables are within management’s control. Moreover, if Vi begins to emerge as a competitive third player, we would expect peers with superior FCF generation, network, and product offerings to respond with heightened competitive intensity.

* Our FY27 estimates remain largely unchanged, while we raise FY28E revenue /pre-IND AS EBITDA by 3-6%, driven by ~2.5% higher ARPU (subscriber mix improvements) and stabilization of the overall subs base.

* We reiterate our Neutral rating on Vi with a revised TP of INR10, based on DCF implied ~14.5x FY28E EV/EBITDA, implying ~24x+ FY28 pre-IND AS EBITDA, which is at a significant premium to Vi’s larger peers.

4Q operationally in line; debt lower due to one-time AGR dues reset

* Reported subscriber base (incl. M2M) was stable QoQ at 192.8m; however, consumer SIMs/data subs (excl. M2M base) declined ~0.9-1.1m QoQ.

* Despite two fewer days QoQ, wireless ARPU rose 1% QoQ at INR174 (+6% YoY vs. flat to -1% QoQ for RJio and Bharti), with customer ARPU rising ~2.1% QoQ to INR190, driven by subscriber mix improvements

* Monthly churn moderated QoQ to 3.9% (vs. 4.4% QoQ, still higher vs. 2.4%/1.7% for Bharti/RJio), likely due to seasonality, and remains a key monitorable.

* Wireless revenue was flat QoQ at INR100.7b (+3% YoY, in line, vs. 0.6%-1.9% QoQ for peers) as subscriber mix improvements offset two fewer days QoQ.

* Pre-Ind-AS 116 EBITDA at INR24.6b rose ~3% QoQ (+5% YoY), as EBITDA margin expanded ~65bp QoQ to 21.5% (+40bp YoY, ~60bp above our estimate).

* Reported EBITDA at INR48.9b (+1.5% QoQ, +5% YoY, vs. ~0.9%/2.1% QoQ for Bharti/RJio) was broadly in line with our estimate.

* Adjusted losses stood at INR55.2b (vs. INR63.6b QoQ) but were higher than our estimate of INR49b loss, primarily due to lower reduction in interest cost to INR48.9b (vs. INR56.4b QoQ, ~16% higher than our est. INR42.2b).

* Vi reported a net exceptional gain of ~INR575b (pertaining to the accounting treatment of the one-time reset of AGR dues on an NPV basis).

* Net debt (excluding leases but including interest accrued) declined ~INR500b QoQ to INR1.53t, primarily due to the accounting treatment of the AGR reset. Vi still owes ~INR1.27t/INR249b to GoI for the deferred spectrum and AGR dues on an NPV basis. External/banking debt stood at ~INR41.3b (vs. INR44b QoQ).

* 4Q capex rose ~2% QoQ to INR22.9b, leading to an INR87.5b capex for FY26 (lower vs. INR95.6b YoY).

* FY26 pre-IND AS EBITDA was broadly stable YoY at INR92.2b, as margin contracted ~55bp YoY to 20.5%, due to network rollouts. Management is aiming to expand pre-IND AS EBITDA margins to 35%+ by FY29 (our estimate is ~23%).

Valuation and view

* Management’s ambitions of double-digit revenue growth and increasing cash EBITDA 3x over FY26-29 remain a tall ask and would require several things such as

1) closure of the debt raise,

2) sustained tariff hikes or a change in tariff construct,

3) stabilization in subscriber trends,

4) more rational competition in subscriber acquisition, and

5) continuation of a benign regulatory regime, including likely relief on spectrum repayments.

* We note that not all of these variables are in management’s control. Moreover, if Vi were to emerge as a competitive third player, we would expect peers with superior FCF, network, and product offerings to raise competitive intensity. * Our FY27 estimates remain largely unchanged, while we raise FY28E revenue/pre-IND AS EBITDA by 3-6%, driven by ~2.5% higher ARPU (subscriber mix improvements) and stabilization of the overall subs base.

* We reiterate our Neutral rating on Vi with a revised TP of INR10 (earlier INR9.5), based on DCF-implied ~14.5x FY28E EV/EBITDA, implying ~24x+ FY28 pre-IND AS EBITDA, which is at a significant premium to Vi’s larger peers (~10.5x implied FY28 pre-IND AS EBITDA for Bharti’s India operations at CMP).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)