Company Update : Reliance Jio by Elara Capital

From disruptor to digital infra powerhouse

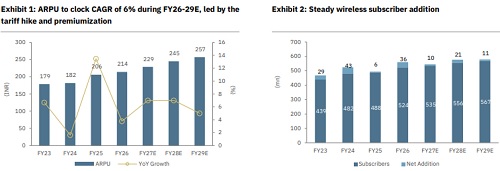

Reliance Jio Infocomm (Jio), India’s largest telecom operator with a subscriber base of 524mn as on FY26, (Source: Company, TRAI) has reshaped India’s telecom landscape by offering some of the world’s most affordable tariffs. That disruption has turned the sector into a quasi-duopoly and positioned Jio to capitalize on rising tariffs and persistently high data consumption. Continued ARPU expansion should be supported by value-added digital services across the Jio Platforms (JPL) ecosystem. Jio’s technology leadership and network design have allowed it to add subscribers without a proportionate increase in recurring investment. We value Jio at enterprise value (EV) of ~INR 12-13tn based on 13x FY28E EV/EBITDA. JPL’s EV is ~INR 13-14tn based on 13x FY28E EV/EBITDA, consistent with a SOTP valuation prepared by our Oil & Gas Analyst Gagan Dixit for Reliance (RIL IN, Rating, CMP: INR 1,298, TP: INR 1,619), subject to the stated assumptions. From scale to monetization: Jio is moving from a market share acquisition phase to a monetization-led growth model, aided by industry consolidation and stronger pricing power. Jio is expected to post ~6% ARPU CAGR during FY26–29E, driven by tariff increases, premiumization, higher data use, and upgrade to postpaid plans. Jio’s large 5G subscriber base and standalone network architecture create significant monetization upside via premium 5G plans and network slicing capabilities. Additionally, accelerating enterprise and B2B traction across connectivity, IoT, cloud, and managed services should raise higher blended monetization, stronger earnings visibility, and improved revenue quality in the medium term.

Home broadband: Jio’s next growth engine:

India’s home broadband market is still underpenetrated, with sub-~18% household penetration across ~350mn homes, presently a large long-term growth opportunity (Source: Elara Securities Estimate). Jio is scaling rapidly via its wireless-first JioAirFiber model, which lowers deployment cost and speeds rollout beyond fiber constraints, especially in Tier II & III and rural areas. Jio’s fixed broadband base has surpassed ~27mn subscribers, driven by JioAirFiber, making it one of the largest global fixed wireless access (FWA) platforms. Moving mobile-only users to home broadband can raise household ARPU by 3-6x and increase data consumption by 8-10x, supporting structurally stronger monetization. Technology upgrades --nLOS hardware and proprietary UBR -- expand Jio’s addressable market and improve rollout economics, enhancing visibility toward Jio’s medium-term target of 100mn home connections

Technology-led execution -- scale and cost leadership:

Jio’s integrated technology stack is a structural advantage that enables lower cost, faster rollout, and superior monetization vs peers reliant on external vendors. Its Cloud-native 5G standalone (SA) network, proprietary UBR & nLOS technologies, and AI-led JioBrain platform improve broadband economics and network efficiency at scale for ~524mn users. Exclusive pan-India 700MHz spectrum provides durable coverage and indoor connectivity advantages while reducing rural rollout cost. Backed by a ~500,000km fiber backbone and in-house home connectivity ecosystem, Jio is assembling a scalable digital infrastructure platform that is hard to replicate.

Transitioning to a monetization-driven digital platform:

Jio is shifting from a scale-based telecom operator to a monetization-led digital platform, driven by tariff hikes, premiumization, enterprise business expansion, and growing adoption of high-ARPU home broadband. Supported by an integrated technology stack, Jio is building a scalable, structurally differentiated digital infrastructure ecosystem with strong long-term earnings visibility. We expect JPL to post a top-line CAGR of 11% and an EBITDA CAGR of 14% during FY26-29E. EV is set to be ~INR 12-13tn based on 13x FY28E EV/EBITDA, and JPL’s EV could be ~INR 13-14tn on the same multiple.

Please refer disclaimer at Report

SEBI Registration number is INH000000933