Company Update :CIE India Automotive Ltd by Motilal Oswal Financial Services Ltd

Beat on estimates due to upbeat EU performance

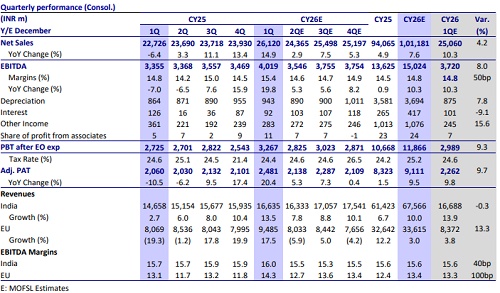

* 1QCY26 consol. revenue grew 15% YoY to INR26.1b, coming in slightly above our estimate of INR25b. Revenue growth was led by 15% growth in the India business and currency translation benefit in Europe business (17% benefit).

* EBITDA stood at ~INR4b (vs est. INR3.7b), growing 20% YoY. EBITDA margins stood at 15.4% (est. 14.8%), up 60bp YoY/90bp QoQ.

* Adj. PAT grew 20% YoY and stood at INR2.4b, ~10% above our estimates.

* Indian business performance: Revenue grew 13.5% YoY to ~INR16.6b (in line). India EBITDA margin stood at 16% (est. 15.6%), up 30bp YoY. Margins were slightly impacted by energy/gas/material costs due to geopolitical headwinds.

* EU business performance: EU business revenues saw a healthy 17.5% YoY growth to INR9.5b, above our estimates of INR8.4b. Entire revenue growth was driven by currency translation gains, while revenues in EUR terms were largely flat YoY. Margins expanded 120bp YoY to 14.3% vs est of 13.3%. Margin expansion was due to restructuring benefits of Legazpi and Metlascastello.

* The Board of Directors has approved the merger of CIE Aluminum Casting India into CIE Automotive India. The rationale for the merger includes: 1) Production and marketing synergies, 2) Cross Selling across OEM relationships, 3) Organizational and operating efficiencies, 4) Stronger financial position, and 5) Elimination of inter-company transactions. In CY25, CIE Aluminum casting posted revenue of INR11.7b, with PAT of INR948m.

* The stock currently trades at ~19.6x/18.3x CY26E/CY27E consol. EPS.

Key highlights from the presentation:

* India light vehicle forecast: IHS forecasts production growth of 8.8% for 2Q and 3QCY26 vs growth of 9.4% in 1QCY26.

* India MHCVs forecast: SIAM forecasts production growth of 7-10% in 2Q and 3QCY26 vs 25% growth in 1QCY26.

* India tractor forecast: TMA expects the strong growth to taper off from 3QCY26 onwards.

* India 2W forecast: SIAM expects an 8-10% growth for 2Q and 3QCY26 vs 20.7% growth in 1QCY26.

* EU (w/o Russia) light vehicles forecast: IHS Global projects light vehicle production to decrease in 2Q/3QCY26 by 5.2/1.1% vs a decline of 1.4% in 1QCY26.

* EU (w/o Russia) MHCV forecast IHS Global projects MHCV production to increase in 2Q/3QCY26 by 3-4% vs 6.5% growth in 1QCY26.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412