2026-01-15 11:14:37 am | Source: Motilal Oswal Financial Services Ltd Ltd

Buy Adani Ports & SEZ Ltd for the Target Rs. 1,800 by Motilal Oswal Financial Services Ltd

Healthy volume growth continues in containers; closure of NQXT acquisition to support volumes ahead

- In Dec’25, Adani Ports & SEZ (APSEZ) completed the acquisition of the North Queensland Export Terminal (NQXT), Australia. NQXT has a contracted volume of 40mmt under a take-or-pay agreement, providing a sustainable cash flow from the port.

- APSEZ has revised its FY26 EBITDA guidance to INR223.5-233.5b from the earlier range of INR210-220b, and cargo volume to 545-555mmt from the previous estimate of 505-515mmt.

- APSEZ has issued 143.8m shares to Carmichael Rail and Port Singapore Holdings Pte Ltd (Promoter entity) as a part of the non-cash transaction, leading to an increase in promoter stake by 2.12%, from 65.89% to 68.02% as of Dec’25.

- In Dec’25, APSEZ reported a 9% YoY growth in cargo volumes, supported by an 18% rise in container volumes (driven by international volume and operationalization of new port). In 3QFY26, volumes grew ~10%, in line with our estimate. Total cargo handled by APSEZ in Dec’25/3QFY26 stood at 41.9/123.1mmt, while YTD volumes reached ~367mmt (up 11%), with container volumes recording a growth rate of ~21%.

- Indian port volumes remained healthy in Dec’25, with volumes handled at major ports standing at 81.6mmt, up ~13% YoY. Container cargo at major ports increased ~7% YoY to 18.8mmt. The growth in volume was supported by a rise in iron ore and coking coal volume by 38% and 63%, respectively. In 3QFY26, Indian port volumes grew by ~13% YoY, with petroleum products/coal/containers accounting for ~30%/~20%/~18% of the total cargo mix, growing ~14%/~5%/11%, respectively. On a YTD basis, volumes rose ~8% YoY.

- With an improvement in earnings visibility, driven by the acquisition of NQXT and expansion of integrated end-to-end offerings, APSEZ captures higher customer wallet share and builds cargo stickiness, while its diversified and scalable model underpins sustainable growth. This positions APSEZ to achieve its goal of becoming India’s largest integrated transport utility by 2029, with logistics and marine emerging as key growth engines alongside its dominant ports franchise. We reiterate our BUY rating on the stock with a revised TP of INR1,800 (premised on 16x FY28E EV/EBITDA).

Scale leadership and rising market share underpin long-term growth visibility

- APSEZ operates the largest private port network in India, with 15 ports and terminals across the west, south, and east coasts, offering a total capacity of 633mmt, along with four international ports in Israel, Sri Lanka, Tanzania, and Australia.

- APSEZ’s domestic market share rose to 28.1% as of Sep’25, from 27.4% in Sep’24. Management highlighted that its domestic port volume growth over the past decade has been nearly three times the industry growth rate.

- The container market share has also expanded steadily to 45.9% from 36% during Mar’20-Sep’25. Key capacity expansions, such as the automated Colombo West International Terminal and new berths at Dhamra, along with the rapid ramp-up of Vizhinjam, are strengthening APSEZ’s growth pipeline.

- Looking ahead, APSEZ maintains its target of 850mmt of domestic and 150mmt of international cargo volumes by 2030, with deeper integration into DFC-linked hinterland corridors and industrial clusters driving long-term growth

Logistics business – Accelerating the shift to a unified logistics ecosystem

- As APSEZ aims to become India's largest integrated transport utility company by 2029, it is strengthening its capabilities across all logistics segments (ports, CTO, warehousing, last-mile delivery, ICDs, etc.). This enables the company to offer end-to-end services, capture a higher wallet share, and ensure cargo volumes remain sticky.

- Adani Logistics Limited (ALL) has expanded its services to cover container train operations, container handling in logistic parks, and warehouses, offering storage and trucking solutions. With 12 multi-modal logistics parks, 132 trains, 3.1m sq. ft. of warehousing space, and 1.3mmt of grain silos, ALL aims to establish a nationwide presence by further developing logistics parks and warehouses.

- With significant capital investments planned for trucking operations—INR10-15b in FY26 and INR50b by FY30—APSEZ maintains a hybrid model, owning 937 trucks and operating over 26,000 via third parties. It is also expanding valueadded services like freight forwarding to improve RoCE

Marine services: A swiftly scaling high-margin growth engine

- Marine operations have emerged as another high-growth vertical within APSEZ, with a diversified fleet of 127 vessels (excluding 46 vessels operated by Adani Harbor across the APSEZ ports), including tugs, anchor handling tug supply vessels, multipurpose support vessels, workboats, and barges.

- The business has been strengthened by acquisitions such as Ocean Sparkle in 2022 and Astro Offshore in 2024, along with the establishment of TAHID to manage international operations in the MEASA region.

- In 2QFY26, marine revenue jumped 237% YoY to INR6.4b, with EBITDA surging to ~INR3.4b and margins expanding to 52.7%. The surge was driven by vessel additions, integration of acquired entities, and higher demand from Tier-1 customers.

- The marine business’s RoCE improved to 15% in 1HFY26 from 13% in FY25.

- Management is aiming to double its revenue from INR11.4b in FY25 (INR11.8b achieved in 1HFY26), positioning the segment as a profitable and capitalefficient business that complements port operations while extending APSEZ’s reach across global shipping routes.

Valuation and view

- With strong cash flows, a healthy cash balance of INR130b, and a net debt-toEBITDA ratio of 1.8x, APSEZ is well-positioned for further expansion. Capacity enhancements at key ports, ongoing infrastructure projects, and global port acquisitions provide visibility for steady growth in FY26 and beyond.

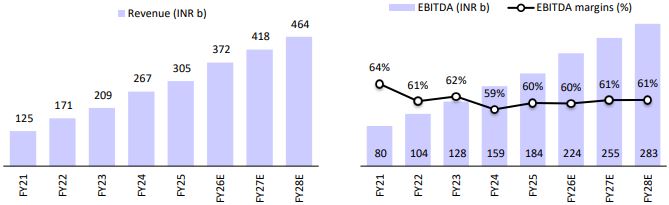

- APSEZ’s diversified cargo mix and ongoing infrastructure investments are expected to support its target of 505-515mmt (ex-NQXT) cargo handling in FY26. We expect APSEZ to report 8% growth in cargo volumes over FY25-28E. This would drive a CAGR of 15%/15%/18% in revenue/EBITDA/PAT over FY25-28E. We reiterate our BUY rating with a revised TP of INR1,800 (premised on 16x FY28E EV/EBITDA).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Auto & Auto Ancillaries Sector Update : Growth accel...

Yen slips but holds intervention gains, traders aler...

Buy Aptus Value Housing Finance India Ltd for the Ta...

India's Bharti Airtel posts profit rise on subscribe...

Evening Roundup : Daily Evening Report on Bullion, B...

Add GAIL Ltd for the Target Rs 200 by Emkay Global F...

Add Sun Pharma Ltd for the Target Rs 2,100 by Emkay ...

Add Shree Cement Ltd for the Target Rs 27,500 by Emk...

Buy ABB India Ltd for the Target Rs 7,600 by Emkay ...

Buy Dixon Technologies Ltd for the Target Rs 16,700 ...

More News

Buy Raymond Lifestyle Ltd for the Target Rs 880 by Motilal Oswal Financial Services Ltd

Buy Transport Corporation of India Ltd for the Target Rs 1,150 by Motilal Oswal Financial Services Ltd

Neutral Aditya Birla Lifestyle Brands Ltd for the Target Rs 105 by Motilal Oswal Financial Services Ltd

Neutral Central Depository Services Ltd for the Target Rs 1,200 by Motilal Oswal Financial Services Ltd