Neutral Union Bank of India Ltd for the Target Rs. 155 by Motilal Oswal Financial Services Ltd

NII in line; business growth remains tepid

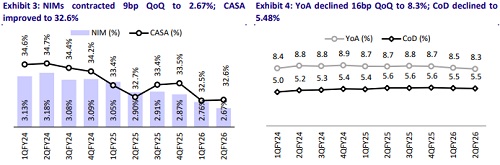

Margin contracts 9bp QoQ

* Union Bank of India (UNBK) reported 2QFY26 PAT of INR42.5b (down 10% YoY/ up 3% QoQ, 20% beat), backed by better other income (amid interest on tax refund), lower provisions, and lower tax rate.

* NII declined 2.6% YoY and 3.3% QoQ to INR88.1b (largely in line with MOFSLe). NIMs stood at 2.67% (down 9bp QoQ, vs our est of 2.67%).

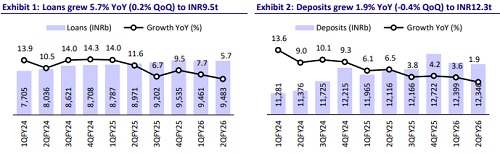

* Loan book grew 5.7% YoY/0.2% QoQ to INR9.48t, while deposits grew 1.9% YoY/ declined 0.4% QoQ. CD ratio increased to 76.8% (up 51bp QoQ).

* Fresh slippages declined 8% QoQ to INR21.5b from INR23.5b in 1QFY26. GNPA/NNPA ratio improved 23bp/7bp QoQ to 3.29%/0.55%. PCR increased to 83.8%.

* We increase our earnings estimate slightly by 3%/2.5% for FY26/FY27E earnings and estimate FY27E RoA/RoE at 1.1%/14.4%. We expect loans to post a 9% CAGR over FY25-27E. We reiterate our neutral rating on the stock with a revised TP of INR155 (0.9x FY27E ABV).

Asset quality improves; IT refund drives earnings beat

* UNBK reported 2QFY26 PAT of INR42.5b (3.2% QoQ, 20% beat). NII declined 2.6% YoY/ 3.3% QoQ; NIMs contracted 9bp QoQ to 2.67%.

* Other income increased 11% QoQ (down 6% YoY) to INR49.9b (9% higher than MOFSLe), amid HIGHER fee income and interest refund on income tax.

* Opex grew 12% YoY/4.6% QoQ to INR69.9b (in line). C/I ratio increased 146bp QoQ to 50.7%. PPoP declined 16% YoY/1.4% QoQ to INR68b (5% beat on MOFSLe).

* Business growth was sub-par yet again, with advances standing flat QoQ (up 5.7% YoY) at INR9.48t. Of this, retail grew faster at 24% YoY/4% QoQ and MSME grew 4.7% YoY/2% QoQ, while large corporate and agri segments continued to decline 1.3% QoQ and 1.9% QoQ, respectively.

* Deposits grew 1.9% YoY/declined 0.4% QoQ to INR12.3t, led by a reduction in CA as well as bulk deposits. CASA grew 1.4% YoY/declined 0.3% QoQ. As a result, CASA ratio stood stable at 32.6%, while CD ratio increased to 76.8% (up 51bp QoQ).

* Deposits grew 1.3% YoY and declined 5.3% QoQ to INR12.4t, led by a reduction in CASA and bulk deposits. CASA ratio decreased 100bp QoQ to 32.5%, while CD ratio increased 350bp QoQ to 76.3%.

* Fresh slippages declined 8.3% QoQ to INR21.5b, while healthy recoveries and upgrades led to an improvement in the GNPA/NNPA ratio by 23bp QoQ/7bp QoQ to 3.29%/0.55%. PCR ratio increased to 83.8%.

Highlights from the management commentary

* The bank aims to achieve growth above the system level going forward and has already identified and addressed the root causes behind the slower deposit growth.

* The sequential contraction in NIMs has been narrowing, with stabilization expected from 3Q onwards and an improving trend likely from 4Q.

* PSLC sales are expected to resume by 4QFY26 or early FY27, at a similar quantum as in FY25.

Valuation and view

UNBK reported an earnings beat, led by healthy other income, lower tax rate, and lower provisions. However, business growth remained tepid, with muted QoQ trends in both advances and deposits, while CASA growth stood flat. NIMs were broadly in line with our expectations, as management has recently prioritized margins over growth, leading to a reduction in bulk deposits during 1HFY26. With business growth being sub-par for the past two quarters, the bank aims to revive momentum. Asset quality ratios continue to improve, led by controlled slippages and in-line provisions. We increase our earnings estimate slightly by 3%/ 2.5% for FY26/FY27E earnings and estimate FY27E RoA/RoE at 1.1%/14.4%. We expect loans to post a 9% CAGR over FY25-27E. We reiterate our Neutral rating on the stock with a revised TP of INR155 (0.9x FY27E ABV)

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412