Neutral BSE Ltd for the Target Rs. 4,400 by Motilal Oswal Financial Services Ltd

In-line 4Q; broad-based growth in transaction charges

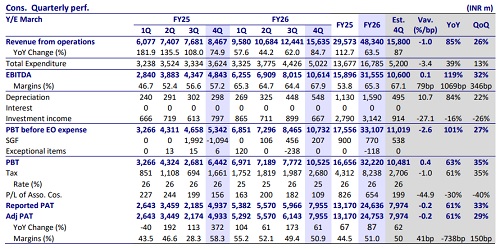

* BSE reported an operating revenue of ~INR15.6b (in line), reflecting a growth of 85% YoY/26% QoQ. This was driven by 114% YoY growth in transaction charges, while revenue from services to corporates declined 5% YoY. For FY26, revenue grew 63% YoY, to INR48.3b.

* Opex came in at INR5b, up 39% YoY/13% QoQ (in line), leading to an EBITDA of INR10.6b, which more than doubled YoY. EBITDA margin was at 67.9% vs. our expectations of 67.1% and 57.2% in 4QFY25.

* PAT grew 61% YoY to ~INR8b (in-line). For FY26, PAT was at INR24.75b, growing 87% YoY.

* The exchange aims for an improvement in cash market share from 7-8% to double-digits. An increase in participants in the derivatives segment from 587 to target of 700 should further boost volumes. Additionally, FPI participation (increased from 100 to 520) and a target of 800 FPI should provide a fillip to monthly contracts.

* We raise our earnings estimates by 17%/20% for FY27E/FY28E, factoring in higher volume assumptions based on the robust Mar’26/Apr’26 run rate. However, we have not baked in any impact from the RBI regulations on proprietary trading. We reiterate our Neutral rating on the stock with a TP of INR4,400 (premised on 40x FY28E EPS).

Derivative activity continues to thrive

* Strong growth in transaction charges of 114% YoY to INR13.1b was driven by 138%/24%/35% YoY growth in derivative/cash/Star MF revenue. However, cash revenue declined slightly owing to higher investments in less volatile large-cap/mid-cap stocks, which traded across both exchanges and have lower rates.

* Cash ADTO grew 65% YoY to INR89.9b, while premium ADTO rose 145% YoY to INR289b in 4QFY26, backed by an increase in trading of longer-tenure monthly contracts.

* STAR MF achieved another record quarter, with total transactions growing 34% YoY to ~239.7m. Mar’26 witnessed record-high transactions of 82m.

* Revenue from services to corporates declined 5% YoY to INR1.2b, owing to 34% YoY decline in listing processing fees. However, a strong IPO pipeline for FY27, with more than 250 applications lined up, provides visibility of revenue growth.

* Other operating income at INR935m grew 43% YoY, largely driven by strong expansion in the colocation facility. For FY26, colocation contributed a revenue of INR1.7b compared to 740m in FY25.

* Treasury income declined 9% YoY to INR403m. Investment income stood at INR667m (27% miss), declining 16% YoY.

* SGF contribution came in at INR207m for the quarter (vs. our estimates of INR538m), with profits allocated towards SGF being reduced to 3.5% from 5% earlier after crossing the INR1.5b threshold.

* Among subsidiaries, BSE Index Service has a total AUM of INR9.15t across 200+ indices and witnessed 100% revenue growth from core index operations.

* ICCL has significantly scaled capacity, with daily trade capacity in equity increasing to 100m from 20m and in derivatives to 90m from 40m.

* Trades/second per member surged 9x to 27,000, enabling faster trade processing and attracting large-scale participants.

Key takeaways from the management commentary

* The exchange plans to expand into commodity derivatives soon. The focus on commodities will be on building differentiated products rather than competing solely on expiry-day positioning.

* BSE received approvals for the launch of three new monthly index derivatives. BSE’s IT-focused index derivatives are scheduled to launch on 11th May’26.

* Monthly contracts continue to gain traction, with the exchange aiming to further deepen participation. Several large market participants are still not members of BSE, though onboarding is underway, and it is expected to support monthly volume growth.

Valuation and view

* BSE continues to demonstrate broad-based growth across key segments, supported by improving institutional participation, stable retail activity, and structural expansion in STAR MF and index businesses. The exchange’s continued investment in technology, data infrastructure, and product diversification is expected to strengthen its competitive positioning and support long-term earnings visibility.

* We raise our earnings estimates by 17%/20% for FY27E/FY28E, factoring in higher volume assumptions based on the robust Mar’26/Apr’26 run rate. However, we have not baked in any impact from RBI regulations on proprietary trading. We reiterate our Neutral rating on the stock with a TP of INR4,400 (premised on 40x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)