Buy ICICI Prudential AMC Ltd for the Target Rs 3,800 by Motilal Oswal Financial Services Ltd

In-line revenue/EBITDA; higher other income drives PAT beat

* ICICI Prudential AMC’s (IPRU) operating revenue grew 18% YoY (flat QoQ) to INR15.6b (in line) in 1QFY27. Yields came in at 56.1bp vs. 56.4bp in 1QFY26 and 55.9bp in 4QFY26.

* Total opex came in at INR4.3b, up 12% YoY/15% QoQ. Employee costs at INR2b rose 11% YoY/45% QoQ, while other expenses came in at INR1b, up 6% YoY but down 12% QoQ. EBIDTA came in at INR11.3b (in line), up 20% YoY but declined 3% QoQ. EBIDTA margin was at 72.4% vs. 71.1% in 1QFY26 and 75.7% in 4QFY26.

* PAT stood at INR9.6b (6% beat mainly due to higher-than-expected other income due to MTM gains), up 23% YoY/26% QoQ. PAT margins came in at 61.7% vs. 58.9% in 1QFY26 and 49.8% in 4QFY26.

* Management indicated that the recent TER regulations will have no impact on earnings as the reduction is passed on to distributors. IPRU maintains a strong product pipeline with recent and upcoming launches across life-cycle funds, ETFs, SIF strategies, commercial real estate and real estate alternate funds, alongside the launch of its first GIFT City inbound offering.

* We have broadly maintained our FY27/FY28 earnings estimates, as higher employee costs and lower debt AUM assumptions are offset by higher other income and lower operating expenses. We project a CAGR of 15%/14%/15% in AUM/revenue/PAT over FY26-FY28E and maintain a BUY rating with a TP of INR 3,800, based on 47x FY28E core EPS.

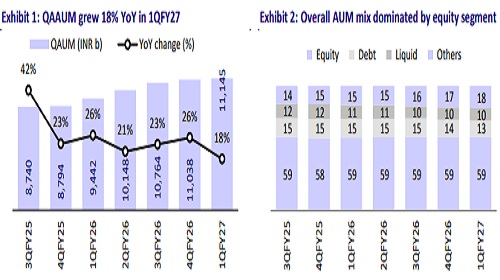

Market share continues to expand

* Total MF QAAUM grew 18% YoY (flat QoQ) to INR11.1t. Equity/Hybrid/ETFs/ Index/Liquid segments grew 17%/23%/45%/16%/9% YoY, but debt remained flat YoY in 1QFY27, led by higher redemptions by corporates.

* The share of Equity/ETF/Debt/Liquid in the total QAUM stood at ~59%/ 13%/13%/10% in 1QFY27 vs. 59%/11%/15%/11% in 1QFY26.

* Alternates QAAUM grew 3% QoQ to INR794.5b, driven by PMS (INR290b; +8% QoQ) and AIF (INR227.4b; +7% QoQ), partly offset by a 5% QoQ decline in assets under advisory (INR277.1b). Yields declined sequentially, with AIF/PMS yields at 95.2bp (vs. 106bp in 4QFY26) and advisory yields at 29.9bp (vs. 34.2bp).

* SIP inflows rebounded in Jun'26 vs. Apr-May’26 (in line with industry trends) to INR48.7b in 1Q, although remained marginally below Mar’26 levels of INR51b in 4Q. The bulk of SIP inflows continued to come from equity funds.

* The company also recently launched its first inbound offering in the GIFT City, i.e., the ICICI Prudential Smart Navigation Fund.

* On the distribution front, MFDs remained dominant in the equity AUM mix at 36.2%, followed by direct at 29.5%, national distributors at 15.9%, and banks at ~18.4% in 1QFY27 vs. 36.7%/28.9%/15.5%/18.9% in 4QFY26.

* Unique customer base grew 2% QoQ to 17.3m as of Jun’26, with 7 out of every 10 new industry customers added by the company.

* The total investment book stood at INR42.3b as of Jun’26, with 72.9% in MFs (57.1% equity, 42.3% liquid & debt, balance others), 23.5% in AIF/other equity/REITs, and the remainder in corporate bonds vs. 75.2% in MFs and 20.9% in AIF/other equity/REITs as of Mar’26. ? Opex-to-AUM ratio at 15.5bp vs. 16.3bp in 1QFY26 and 13.6bp in 4QFY26.

* Operating expenses rose 12% YoY/15% QoQ, primarily driven by 11% YoY/45% QoQ growth in employee costs. The QoQ jump was owing to a one-off reversal in 4QFY26 and new ESOP costs accruing from 1QFY27.

* ESOP expense would be in the range of INR640-680m in FY27, with total ESOP cost of INR1.25-INR1.30b spread over three years.

* Fees and commission expenses increased 20% YoY, reflecting higher distribution payouts in the fast-growing AIF and PMS businesses.

* Other income came in at INR1.8b vs. our est. of INR1.1b, led by MTM gains.

Valuation and view

* The absence of any material earnings impact from TER revisions, coupled with improving contribution from alternatives, AI-led operating efficiencies, and new product launches, strengthens confidence in the company's long-term growth trajectory and valuation.

* We have broadly maintained our earnings estimates for FY27 and FY28, factoring in higher employee costs and lower debt AUM assumption, which should be offset by higher other income and lower other expenses. Over FY26- FY28E, we project AUM/revenue/PAT CAGRs of 15%/14%/15%. We maintain our BUY rating on the stock, with a TP of INR3,800, based on 47x FY28E core EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412