Buy Avenue Supermarts Ltd for the Target Rs 4,800 by Motilal Oswal Financial Services Ltd

Growth decelerates; margins remain resilient

* Avenue Supermarts (DMART) revenue growth moderated to ~15% YoY in 1QFY27, as like-for-like (LFL) growth decelerated to 5.5% (vs. 10.8% in 4QFY26). Management indicated that revenue growth for older stores in large metros was flat, while non-metro stores’ revenue grew well.

* Profitability was in line with expectations as ~45bp YoY gross margin expansion (~20bp beat, ~75bp YoY increase in the share of higher-margin GM&A category) was offset by higher employee costs (+32% YoY).

* After accelerated store expansion in 4QFY26, the pace of store additions moderated to three stores in 1QFY27 and remains a key growth lever. DMart Ready continued to rationalize its footprint, exiting seven additional cities with marginal contribution and limiting its presence to just 11 cities.

* Our FY27-28E EBITDA/PAT estimates remain broadly unchanged. We build in a CAGR of 18%/19%/16% in DMART’s consol. revenue/EBITDA/PAT over FY26- 29E, driven by a 15% CAGR in area additions and high-single-digit LFL growth.

* We assign a ~40x Sep’28 EV/EBITDA multiple (implying ~72x Sep’28 P/E) to arrive at our revised TP of INR4,800. We reiterate BUY on DMART.

In-line results; old stores revenue in large metros remained flat in 1Q

* Standalone 1Q revenue grew ~15% YoY to INR183b (already disclosed) as LFL growth moderated to 5.5% (vs. 7.1%/10.8% in 1Q/4QFY26). ? Management indicated that revenue in older stores in large metros was flat, while non-metro stores continued to grow well.

* After significant store additions in 4QFY26, the company added modest 3 stores/0.1m sqft area in 1Q to reach 503 stores and 20.7m sqft area. This implies addition of an average 33.3k sqft stores in 1QFY27 (lower than the average store size of 41.2k sqft).

* DMart’s store count/area grew ~19%/18% YoY, while annualized revenue per store declined ~4% YoY to INR1.46b and annualized revenue/sqft was down ~3% YoY at INR35.5k.

* Standalone gross profit came in at INR27.7b (up 19% YoY, our est. INR27.3b) as gross margin (GM) expanded ~45bp YoY to 15.1% (~20bp beat).

* Share of the higher-margin general merchandise and apparel (GM&A) category rose ~75bp YoY to 25.5%, while Foods share contracted ~65bp YoY to 54.9% and non-food FMCG share moderated ~5bp YoY to 19.6%.

* Standalone EBITDA at INR15.3b (in line) rose ~16% YoY, as margins expanded ~10bp YoY to 8.3%. Better GM was offset by higher employee costs (+32% YoY, 6% ahead).

* Other expenses grew ~18% YoY as the cost of retailing per sqft inched up ~3% YoY (~4% above our estimate).

* Standalone PAT at INR9.4b (in line) rose ~13% YoY, with PAT margin moderating ~10bp YoY to 5.1% as interest cost surged (+90% YoY).

* DMart board approved the issuance of NCDs worth INR10b, which should help in accelerating the pace of store additions (vs. 85 in FY26)

Losses increase YoY in subsidiaries

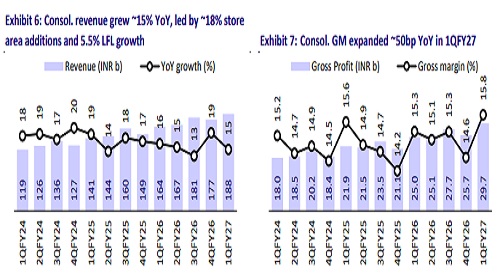

* Consolidated revenue grew 15% YoY to INR188b (in line).

* Consol. GP grew 19% YoY to INR29.7b (vs. our est. INR29.3b) as margins expanded ~50bp YoY to 15.8% (~25bp beat).

* Consol. EBITDA rose ~15% YoY to INR15b (in line) as margins remained stable YoY at 8% (in line). Operating loss in subsidiaries increased to 6.1% (vs. 3.3% YoY and 4.3% QoQ).

* Consol. PAT grew 11% YoY to INR8.6b (in line). PAT margin contracted ~15bp YoY to 4.6% as finance cost surged (+85% YoY)

Valuation and view

* Given significant store additions in 4QFY26 and an overall inflationary environment, growth deceleration to ~15% in 1QFY27 is a dampener and has reignited concerns about DMart losing market share to quick commerce (QC) in large metro cities.

* Commentary on store additions, impact of competitive intensity in large metros and performance of recently opened stores in tier 2 cities remain key monitorables during the upcoming Analyst Day (typically held in the last week of July). We continue to build in 85-90 annual store additions in FY27-29.

* While the competitive intensity from QC could remain elevated in the near-tomedium term, we believe DMART’s value-focused model and superior store economics would ensure its competitiveness and customer relevance over the long run, especially in tier 2+ towns.

* Our FY27-28E EBITDA/PAT estimates remain broadly unchanged. We build in a CAGR of 18%/19%/16% in DMART’s consol. revenue/EBITDA/PAT over FY26-29E, driven by a 15% CAGR in area additions and high-single-digit LFL growth.

* We assign a ~40x Sep’28E EV/EBITDA (earlier ~41x Jun’28) multiple (implying ~72x Sep’28 P/E) to arrive at our revised TP of INR4,800 (earlier INR4,750). We reiterate BUY on DMART.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412