Buy Indian Bank Ltd For Target Rs.1,000 by Prabhudas Liladhar Capital Ltd

Profitability would help tide over ECL impact

INDIANBK saw a decent quarter; while loan growth and NIM were healthy resulting in higher NII/NIM, core PAT saw a drag as ECL provision of INR 10bn was made during the quarter. Management suggested that one-time ECL impact could be INR30bn, with incremental provision likely to be 12bps on standard assets. The bank continues to focus more on profitability than growth; we are factoring a loan/deposit CAGR of 12.5%/11.0% over FY26-28E. INDIANBK is a good quality PSB due to its management quality and earnings consistency. We expect core PAT CAGR of ~20% over FY26-28E, core RoA of 0.9% (FY28E) and negligible NNPA of 0.13%. We assign multiple of 1.3x on Sep’28 ABV to arrive at a TP of INR 1,000 and give a ‘BUY’ rating.

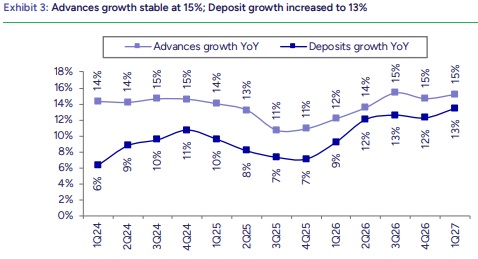

Good quarter with healthy loan growth/NIM; higher provisions drag core PAT: NII was higher at INR 74.3bn due to better NIM (calc.) at 3.21%; reported NIM up 6bps QoQ to 3.29%. Loan/deposit grew by 15.2%/13.5% YoY. CASA ratio was stable QoQ at to 37.8%. Other income was a tad better at INR 26.3bn; lower fees was offset by TWO recovery. Opex came in at INR 45.1bn; staff cost jumped by 13% QoQ that was offset by 11% QoQ fall in other opex. Core PPoP was INR 42.9bn. Asset quality was better; GNPA fell by 12bps QoQ to 1.86% due to lower gross slippages (INR 13bn) and better recoveries (INR 9.4bn), which was mainly due to recovery of a large account. Provisions were accelerated at INR 12bns, which includes INR 10bn for ECL. Core PAT was a drag at INR 20.1bn due to higher provisions.

Loan growth was mainly led by retail/agri: Loan growth was healthy at 2.8% QoQ that was mainly led by retail (+3.8%) and agri (3.5%); corporate and SME growth was softer at 1.8%/1.9% QoQ. The bank has mobilized ~USD 150mn of FCNR deposits so far, with an additional USD 1bn pipeline; it expects to raise USD 1.5–2.0bn through FCNR deposits and ECBs during FY27. ECLGS loans of ~INR50bn have been disbursed out of the eligible pool of INR 110bn. Credit growth for FY27 is guided at 11–13%, with gap between credit/deposit growth to be range-bound. We are factoring loan/deposit CAGR of 12.5%/11.0% over FY26-28E.

Reported NIM improved QoQ; credit cost to increase by 12bps due to ECL: NIM (reported) improved 6bps QoQ to 3.29% due to (1) selective lending and avoiding thinly priced corporate loans, (2) focus on CASA mobilization and (3) opting low-cost borrowings over bulk deposits. On ECL, bank expects ~12bps incremental provision on standard assets due to the new norms. Bank reported no visible SME stress from the USIran conflict, citing economic resilience and exporters’ ability to diversify geographically; buffer provision of INR 130mn was created during Q1’27. Any likely MSME stress is expected to be largely mitigated through ECLGS.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271