Buy LTM Ltd for the Target Rs 4,900 by Motilal Oswal Financial Services Ltd

On a stronger footing Stable revenue and beat on margins; well set up for FY27

* LTM reported revenue of USD1.2b in 1QFY27, up 0.3% QoQ in constant currency (CC) vs. our estimate of flat revenue QoQ CC. EBIT margin at 15.5% was above our estimate of 15.1%. Adj. PAT came in at INR14.7b, up 9.5% QoQ/17.1% YoY and in line with our estimate of INR15b.

* In INR terms, revenue/EBIT/adj. PAT grew 18%/27.9%/17.1% YoY in 1QFY27. In 2QFY27, we expect revenue/EBIT/adj. PAT to grow 13.6%/14.6%/14.2% YoY. We maintain BUY with a TP of INR4,900 (valuing at 21x FY28E EPS), implying ~21% upside.

Our view: 2Q recovery on track; margins surprise positively

* Revenue growth came in flat (+0.3% QoQ CC) due to a seasonal passthrough decline in Production (-5.7% QoQ) and a delayed India PAN card deal ramp-up impacting the Consumer segment (-0.7% QoQ). However, BFS (+3.2% QoQ) and Tech & Services (+3.4% QoQ, +10% YoY) grew well, aided by broad-based momentum across top 5/top 10 client categories (+4.5%/+4.3% QoQ).

* Margins came in better than expected at 15.5% (+40bp QoQ) as wage hike impact (~100bp) was almost entirely offset by currency gains and operational efficiencies helped as well. Margin performance was commendable. Though we expect some headwinds from Randstad once it is integrated, we expect organic margins to expand by 60bp YoY in FY27.

* Cash flow metrics worsened optically – OCF/PAT at 79%, down from 96% in 4Q; FCF/PAT at 63%, down from 75%, but this was largely due to a one-time non-cash valuation gain on the Voicing AI investment, which inflated the PAT base. Adjusted for this, OCF/PAT and FCF/PAT would have been 88% and 70%, respectively, largely in line with 4Q. We do not read this as a deterioration in operational cash conversion.

* The PAN card deal ramp-up remains on track to resume in 2Q, contingent on hardware/memory chip shipment timelines normalizing over the next month or two.

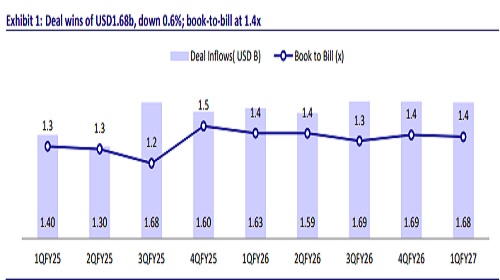

* Management's confidence that FY27 growth will be "better than FY26" is encouraging, and if delivered, it would put LTM among the fastest-growing names in the top six IT services peers. LTM has gone through the difficult transition of up-fronting productivity pass-throughs in its key BFS/Hi-tech accounts, and this creates a slight advantage over peers in FY27.

Valuation and view

* We believe LTM’s estimated EPS CAGR of 13% for the next two years remains meaningfully better than that of large-caps. Productivity pain for key accounts is behind, which could be positive vs. peers in the next couple of years. While growth acceleration remains measured at ~7-8% over FY27-FY28 and the recovery in the top BFSI account recovery is likely to be gradual, strong deal wins and a robust pipeline provide visibility. We raise our estimates by 1-2% for FY27/FY28. In addition, stable margin execution and improving visibility on growth lead us to raise our target multiple to 21x FY28E EPS (19x earlier). This results in a revised TP of INR4,900, implying ~21% upside. We reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Buy Raymond Lifestyle Ltd for the Target Rs 880 by Motilal Oswal Financial Services Ltd