Hold Clean Science and Technology Ltd for the Target Rs. 1,002 By Prabhudas Liladhar Capital Ltd

HALS volume to pick going ahead

Quick Pointers:

* Performance Chemical 1 is undergoing chemical trials, revenue contribution expected from Q4FY26

* HALS monthly average volumes stood at 260tn, an increase of 25% sequentially

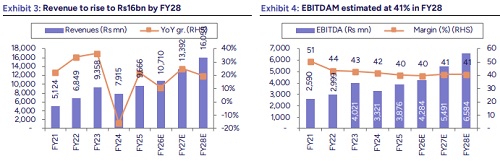

Clean Science and Technology (CLEAN) reported revenue of Rs 2.4bn in Q2FY26, registering a modest 2.7% YoY and 0.7% QoQ increase. Growth was impacted by a decline in revenue from established products, which contributed 80% of the revenue mix, down from 84% in Q1FY26. The FMCG chemicals segment saw the steepest drop, driven by backward integration by a key Chinese customer. HALS volumes averaged 260tn per month, reflecting a strong 25% sequential increase, and management expects continued volume growth in coming quarters. A reduction in raw material costs supported an improvement in HALS gross margins, rising from 31% to 35%. As per our calculation HALS subsidiary reported an EBITDA loss of 29mn in Q2FY26. On the capex front, chemical trials at Performance Chemicals 1 are underway, with revenue contribution expected from Q4FY26. Performance Chemicals 2 remains on schedule with water trials expected from April’26. Looking ahead, these upcoming capacity additions are expected to drive growth; however, margin pressures may persist due to lower realizations in certain established products and the relatively lower profitability of the HALS portfolio compared to the legacy business. At its current valuation of 24x Sep’27 EPS, we maintain ‘HOLD’ rating on CLEAN, with target price of Rs1,002 valuing it at 25x Sep’27 EPS.

* Deline in legacy products sales led to modest topline growth: Consolidated revenue stood at Rs2.4bn, 2.7% YoY/0.7% QoQ (PLe: Rs2.4bn, Consensus: Rs2.5bn). Top 4 products revenue mix declined to 80% vs 84% in Q1FY26. H1FY26 revenue was at Rs4.9bn, 5.5% higher than H1FY25. HALS monthly average volumes stood at 260tn, an increase of 25% QoQ. Gross profit margin was at 60.7% (vs 62.4% in Q2FY25 and 65.5% in Q1FY26), margin declined by 480bps QoQ due to increase in overall raw material cost. Gross profit decreased by 0.1% YoY and 6.6% QoQ.

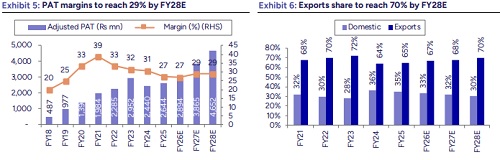

* EBITDAM declines sequentially by 550bps: EBITDA stood at Rs871mn, -2.9% YoY/ -12.8% QoQ (PLe: Rs960mn, Consensus: Rs956mn), EBITDA margin came at 35.6%, declined by 210bps YoY and 550bps QoQ (vs 37.7% in Q2FY25 and 41.1% in Q1FY26), declined due to increase in overhead costs. H1FY26 EBITDA increased by 1.4% to Rs1,869mn. Reported PAT was at Rs554mn, - 5.6% YoY/ -20.9% QoQ. PAT margins were at 23% vs 25% in Q2FY25 and 29% in Q1FY26.

* Concall takeaways: (1) Domestic and Export mix: 37%: 63%. (2) Revenue was hit due to decline in sales of established products, top 4 products sales mix stood at 80% vs 84% in Q1FY26 and 70% in Q2FY25. (3) 25%-30% revenue comes from China, realizations in China are at all time low. (4) HALS monthly average volumes stood at 260tn, total volumes in Q1FY26 were 580tn. (5) HALS 2020 was commercialized during Q2FY26. (6) Value growth was 34% for HALS sequentially. (7) Export: Domestic mix for HALS stood at 75%:25%, which changed from 80%:20% in Q1FY26. (8) Rs1.5bn capex undertaken in subsidiary in H1FY26. (9) Performance Chemical 1 is undergoing chemical trials. (10) Barbituric acid commercialized by repurposing PBQ assets during Q2FY26. (11) BHT got hit due to 55% tariff in USA.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271