HDFC Asset Management Company Ltd For Target Rs.3,239 by Geojit Investments Ltd

Strong AUM and new launches drive revenue

HDFC Asset Management Company Ltd. (HDFC AMC) is a leading asset-management company (AMC) in India, with assets under management (AUM-closing) of Rs. 8,440bn as on 31 March 2026.

* In Q4FY26, the AMC’s operating revenue increased 16.7% YoY to Rs. 1,052cr, driven by growth in quarterly average AUM (QAAUM) and healthy equity and systematic flows.

* As of Q4FY26, overall QAAUM increased 19.8% YoY to Rs. 927,500cr, translating into an 11.4% share of the overall mutual fund (MF) industry.

* Equity-oriented QAAUM (excluding index funds) increased 22.7% YoY to Rs. 565,700cr, while debt-oriented QAAUM rose 10.8% YoY to Rs. 175,800cr.

* In Q4FY26, systematic transaction value grew 33.7% YoY to Rs. 48,800cr.

* EBITDA grew 15.7% YoY to Rs. 845cr; however, EBITDA margin declined 60bps YoY to 80.4%, mainly due to higher employee costs (+29.4% YoY) and other expenses (+7.1% YoY).

* Consequently, profit after tax fell 2.5% YoY to Rs. 623cr in Q4FY26.

Outlook & Valuation

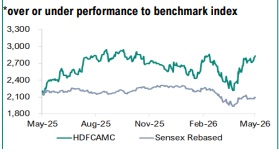

HDFC AMC continued to demonstrate resilient performance, with management emphasising that domestic investors have become meaningfully more long-term oriented and systematic in their approach even amid heightened volatility. Additional momentum is expected to come from passive and hybrid products, along with newer growth engines such as alternatives, PMS mandates and the GIFT City international platform. The company is also increasingly leveraging technology and AI-led capabilities to enhance investment processes, improve customer engagement and drive operational efficiencies. Ongoing investments in digital platforms and analytics are expected to strengthen scalability over time. Hence, we upgrade our rating on the stock to BUY, with a roll-forward target price of Rs. 3,239, based on discounted dividend model valuation.

Key concall highlights

* On TER/BER regulatory change, management guided that the gross impact on the existing book is ~3-4 bps and it intends to largely offset it via commission optimisation and prudent cost management, targeting no material impact on the P&L.

* In Q4FY26, HDFC AMC reported resilient yields across asset classes. The equity yield was approximately 56 bps, including index funds; the debt yield was around 28bps; and the liquid yield was about 13bps. The blended yield for the FY26 was 45bps.

* Management highlighted that it has received all regulatory approvals for SIF, but is not rushing, and will launch only an investment-led, differentiated offering that solves a real client need rather than being first-to-market.

* In Q4FY26, the AUM of its portfolio management services (PMS) was Rs. 106bn, with non-discretionary PMS at Rs. 56bn, discretionary PMS at Rs. 48bn and Rs 1.5bn in advisory.

* AI is being integrated across the organisation as an operating layer from marketing and client engagement to investment processes, risk management and compliance serving as a force multiplier for teams rather than a replacement.

* The company declared a final dividend of Rs. 54 per share.

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer

SEBI Registration Number: INH20000034