Accumulate Kansai Nerolac Paints Ltd For Target Rs.248 by Prabhudas Liladhar Capital Ltd

Steady demand, frequent price hikes a concern

Quick Pointers

* KNPL took price hike of low teens in decorative segment over April and May

* KNPL unlikely to take further price hike if Crude stabilizes below $100

* EBITDA margin guidance sustained at 13-14% band range for FY27

We increase our FY27/FY28 EPS estimates by 2.3%/4.2% led by 1) high single digit overall price increase led by price hike of low teen in decorative segment. 2) Healthy demand outlook for auto with continued recovery in decorative segment and 3) Sustained EBITDA margin guidance of 13-14% despite macro headwinds.

However, we believe that frequent price hikes would have built up trade inventory, it has the potential to choke trade if there is meaningful decline in crude prices. We expect healthy volume growth in auto paints (30% of total sales) till 2Q27 due to carry over impact of GST rate cuts, unless we witness sharp increase in cost of ownership due to higher petrol/diesel prices.

We expect 7.3% volume CAGR growth and ~50bps margin expansion over FY26-28. We estimate a CAGR of 8.6% in sales and 10% EPS CAGR over FY26-28. We value the stock at 25xMar28 EPS and assign a target price of Rs248 (Rs234 earlier). While stock offers reasonable upside in near term, long term cautious view decorative Paints sustains. Retain Accumulate.

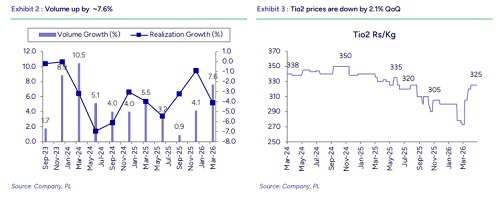

Revenues grew 7.6%; Volume growth ~7.6%:

* Revenues grew by 7.6% YoY to Rs18.7bn (PLe: Rs18.50bn).

* Gross margins contracted by 3bps YoY to 34.6% (Ple: 35.8%).

* EBITDA grew by 21% YoY to Rs2.2bn (PLe:Rs2.07bn); Margins expanded by 127bps YoY to 11.5% (PLe:11.2%).

* Adjusted PAT grew by 7.6% YoY to Rs1.3bn (PLe:Rs1.35bn)

* Company announced a dividend of Rs. 2.50/ share

Concall Highlights:

* Demand remained resilient through Q4, KNPL expects momentum to sustain in the near term led by healthy auto demand and sustained recovery in decorative

* Overall volume grew by high-single digits in Q4, auto segment saw double-digit growth, while powder coatings grew mid-single digits

* Competitive intensity continues to remain high with price hike being taken by all the players including regional ones

* KNPL gained overall market share, driven by stronger performance in Tier-2 & Tier-3 markets

* KNPL may undertake further price hikes in case of sustained crude-led inflationary pressures

* Decorative segment continues to witness recovery with healthy demand traction

* Project business contribution stood at ~10% of total revenue

* 2 Wheelers, 3 Wheelers, Commercial Vehicle & Tractors witnessed strong double-digit growth in 4QFY26

* Company reiterated EBITDA margin guidance of 13–14% over near to medium term

* Industrial segment capacity utilization remains at ~70–75%

* KNPL implemented staggered price hikes (low-teens) in the decorative segment during Q4 with 2/ 5-6/5- 6/5-6% in March/April/May respectively

* In the industrial segment, price increases have been granted in auto, with negotiations being slightly delayed but new prices for channel sales were effective mid-April.

* New pricing in the industrial segment became effective from mid-April

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

Tag News

Accumulate Kansai Nerolac Paints Ltd For Target Rs 240 By Elara Capital