Sell Shree Cement Ltd for the Target Rs. 23,330 by Choice Institutional Equities

Premium valuation limits upside

We maintain our SELL rating on Shree Cement Limited (SRCM) with a revised target price of INR 23,330/share (earlier INR 25,580/share). Our negative stance is due to: 1) Possible cost inflation of INR 150– 200/t in Q1FY27 led by higher power & fuel and PP bag cost, 2) Slower-than-expected capacity expansion, with future addition contingent on demand recovery and utilisation improvement, 3) Limited scope for further structural cost-optimisation as SRCM already operates amongst the most efficient cost structure in the industry, supported by high renewable/green power penetration (~61%), 4) A sub-optimal capital structure with cash & equivalents of ~INR 143 Bn (~15.8% of market cap), which continues to be an overhang on return ratios and 5) Rich valuation multiple despite moderating growth prospects.

While SRCM remains one of the best-in-class cement companies in terms of governance, execution, brand strength, operational efficiency and EBITDA/t, we believe the current valuation adequately prices in these strengths, leaving limited scope for further re-rating.

We estimate SRCM’s EBITDA to expand at a CAGR of 8.8% over FY26–29E, supported by volume growth assumption of 5%/6%/7% and realisation growth of 1.5%/0.5%/0.5% across FY27E/FY28E/FY29E, respectively

Our valuation is based on a robust EV/CE (Enterprise Value to Capital Employed) framework, wherein we assign a FY28E EV/CE multiple of 2.6x to derive a 1-year forward target price of INR 23,330/share. Although SRCM’s ROCE is expected to improve, from 10.5% in FY26 to 13.1% in FY29E, we believe the pace of earnings growth and return expansion remains insufficient to justify the stock’s premium valuation

Q4FY26 result: Volume growth strong; profitability remains under pressure

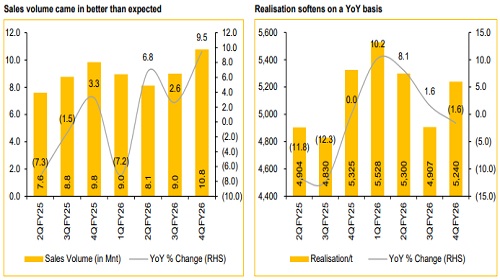

SRCM reported Q4FY26 revenue and EBITDA of INR 56,430 Mn (+7.7% YoY,+27.8% QoQ) and INR 12,503 Mn (-9.5% YoY, +45.3% QoQ) vs CIE estimate of INR 50,359 Mn and INR 11,724 Mn, respectively. Total volume for Q4 stood at 10.8 Mnt (vs CIE estimate 10.1 Mnt), (+9.5% YoY, +19.7% QoQ)..

Realisation/t, which came in at INR 5,240/t (-1.6% YoY and +6.8% QoQ), is higher than CIE’s estimate of INR 5,008/t. Total cost/t came in at INR 4,079/t (+4.0% YoY and +3.2% QoQ). As a result, EBITDA/t came in at INR 1,161/t (-17.3% YoY and +21.4% QoQ), which is in line with the CIE estimate of INR 1,166/t.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131