Buy Lloyds Metals and Energy Ltd for the Target Rs. 2,075 by Choice Institutional Equities

Investment View & Target Price: INR 2,075 (17.7% Upside)

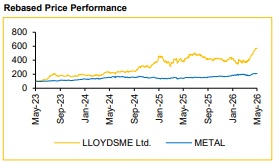

We maintain our BUY rating on Lloyds Metals and Energy Ltd (LLOYDSME) with a revised SoTP-based Target Price of INR 2,075. LLYODSME is structurally shifting from a pure mining play to a higher-margin, integrated metals platform.

Aggressive Volume Visibility: Management has laid out a clear, highvelocity roadmap with FY27E production guidance at 26 MnT for Iron Ore and ~8 MnT for Pellets, ensuring top-line momentum remains resilient

Industry-leading Capital-efficiency: LLOYDSME is operating at an efficiency much higher than its peers, boasting a 35.1% ROE and 25.3% ROCE in FY26 – metrics that underscore the lean, MDO-led execution engine.

A Multi-decade Strategic Moat: With mine leases secured until 2057, LLOYDSME is not just a trade; it is a 30-year annuity on India’s infrastructure build-out. Even at an aggressive run-rate of 26 MnT/year, current reserves provide a ~15 years runway, protected by the lowest cost-curve in the industry via the 85-km slurry pipeline along with legacy mine benefits.

Note: Our current valuation does not consider the Copper Cathode business in the DRC, providing further potential optionality to the target price as commercial visibility improves.

Record-breaking Scale: A Masterclass in Operating Leverage

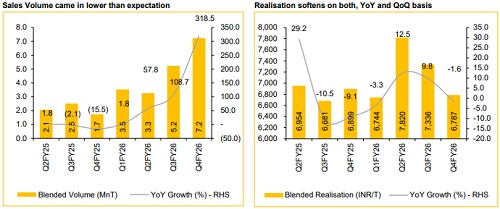

Lloyds Metals (LLOYDSME) has delivered a powerhouse performance for Q4 & FY26, cementing its status as a high-growth leader in the metals and mining space. The company achieved its highest-ever quarterly and yearly Revenue, EBITDA and PAT on a standalone basis.

* Explosive Top-line Growth: Standalone revenue for Q4FY26 surged 311.7% YoY to INR 49,129 Mn

* Annual Milestone: Full-year revenue crossed INR 1,36,806 Mn, representing a 103.5% YoY increase

* Margin Expansion Powerhouse: Standalone EBITDA margin expanded sharply to 32.9% in Q4, an increase of 1,097 bps YoY

* Operational Efficiency: This margin growth was driven by a richer product mix and the rapid ramp-up of the Pellet plant, which reached 100% capacity utilisation on an annualised basis in just four months

* Profitability Surge: Standalone PAT for the quarter skyrocketed to INR 10,656 Mn, a 426.3% YoY increase

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131