Neutral Vedanta Ltd for the Target Rs. 800 by Motilal Oswal Financial Services Ltd

Broadly in-line earnings due to favorable LME and better volume; strong near-term outlook

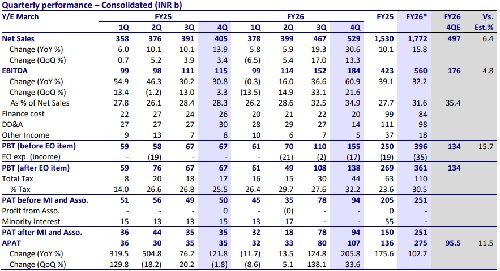

Consolidated result highlights

* Vedanta Limited (VEDL) reported a consolidated revenue of INR528b (+31% YoY and +13% QoQ) vs. our est. of INR497b, driven by higher LME, better volume, and forex gains in 4QFY26.

* Consolidated EBITDA stood at INR184b (+61% YoY and +22% QoQ) against our est. of INR176b, mainly driven by higher LME premiums, forex gains, and higher volumes.

* EBITDA margin stood at 34.9% vs. 32.5% in 3QFY26 and 28.3% in 4QFY25.

* APAT for the quarter stood at INR106.5b (+206% YoY and 34% QoQ) vs. our est. of INR96b.

* In FY26, revenue stood at INR1,772b (+16% YoY), whereas EBITDA was INR560b (+32% YoY) and APAT was INR251b (+85% YoY).

* Net debt stood at INR532b as of Mar’26, translating to a net debt/EBITDA of 0.95x in 4QFY26 vs. 1.22x in 4QFY25.

Segmental result highlights Aluminum:

* VEDL produced 613kt of aluminum, registering a growth of 2% YoY, whereas the alumina production from the Lanjigarh refinery grew 104% YoY to 882kt in 4QFY26.

* Revenue from the aluminum business came in line at INR187b (+17% YoY and +11% QoQ), whereas the EBITDA grew 88% YoY and 21% QoQ to INR85b in 4QFY26.

* Aluminum’s cost of production (CoP) increased to USD1,742/t during the quarter (down 13% YoY) vs. USD1,674/t in 3QFY26. Zinc India (HZL):

* Hindustan Zinc (HZ) reported revenue of INR135b (+49% YoY and +23% QoQ) for 4QFY26, beating our estimate of INR116b. The growth was driven by favorable commodity prices and volume recovery.

* EBITDA came in at INR77b (+60% YoY and +27% QoQ), against our estimate of INR65b during the quarter. The increase was primarily on account of favorable metal prices and a lower cost of production. EBITDA margin stood at 56.9% in 4QFY26 vs 55.1% in 3QFY26 and 53% in 4QFY25.

* Zinc COP (ex-royalty) stood at USD903/t in 4QFY26, declining 9% YoY and 4% QoQ, driven by lower power costs from increased domestic coal usage and better mined grades of 7.9% in 4QFY26 (~7.3-7.4% in FY26).

* APAT stood at INR50b (+68% YoY and +29% QoQ), against our est. of INR41b in 4QFY26.

* Mined metal for the quarter stood at 315kt (+1% YoY and +14% QoQ), driven by higher ore production and better grade.

* Refined metal production for the quarter stood at 282kt (+5% YoY and QoQ), driven by incremental capacity via debottlenecking at Chanderiya and Dariba with a better plant availability. Refined zinc production was 227kt (+6% YoY and +3% QoQ), while refined lead production stood at 55kt (-2% YoY and +12% QoQ) due to partial pyro operation in lead mode. ? Salable silver production rose 11% QoQ and remained flat YoY at 176kt, in line with lead production. Zinc International:

* Mined metal production was down 3% YoY to 49kt in 4QFY26.

* Revenue stood at INR11.7b (+6% YoY), whereas the EBITDA declined by 73% YoY to INR1.1b, led by lower volumes and higher costs.

* During the quarter, the CoP grew by 51% YoY to USD1,912/t in 4QFY26 vs USD1632/t in 3QFY26. Copper:

* Copper cathode production was down 4% YoY to 42kt in 4QFY26.

* Revenue stood at INR94.5b (+54% YoY), led by favorable LME; reported EBITDA profit was INR80m in 4QFY26 against a loss of INR490m in 4QFY25. Iron Ore:

* Iron ore sales stood at 2.1mt, down 1% YoY, and pig iron sales rose 5% YoY to 215kt in 4QFY26.

* Revenue stood at INR17.2b (+13% YoY), while EBITDA came at INR4.1b, up by 32% YoY during the quarter.

Valuation and view

* VEDL’s 4QFY26 performance came largely as expected, supported by better volumes and favorable LME prices. Management targets to maintain strong growth in earnings, driven by the upcoming capacity supporting higher VAP products and a favorable pricing environment. The guided capex plans are progressing well and will likely lead to further cost savings. VEDL remains firm on its deleveraging plans, and going forward, higher cash flows will support both its expansion plans and deleveraging efforts. We largely maintain our FY27E/28E revenue and EBITDA, while increasing our PAT estimates by 20% for FY27/28.

* VEDL to demerge into five independently listed entities w.e.f. 1 st May’26 – 1) Aluminum, 2) Oil & Gas, 3) Power, 4) Iron & Steel, and 5) Vedanta Ltd., with the residual operation, which will retain the HZL business.

* The stock currently trades at 6.6x EV/EBITDA on the FY28 estimate. The combined fair value on the SoTP basis comes to ~INR800/share, with the largest contributing verticals such as Aluminum and Zinc. We reiterate our Neutral rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)