Buy Radico Khaitan Ltd for the Target Rs. 3,950 by Choice Institutional Equities

Market Share Gains in Vodka and Premium Brandy Buoy FY26

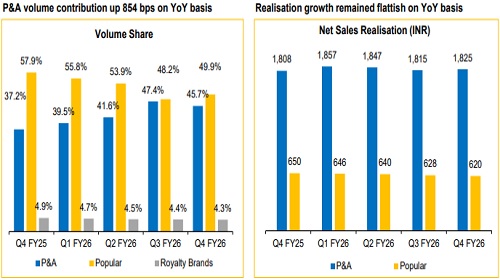

RDCK’s premiumization-led momentum remained intact as indicated by P&A revenue, which rose 30.9% YoY, driven by a strong traction in UP, AP and RJ. Regular segment declined 10.2% YoY due to base effect and policy changes in MH and KA. Jaisalmer Gin continued to command ~50% share in the luxury craft gin market, while Magic Moments stood at 60% of the Vodka market. Recent Luxury launches, such as Rampur 1943 Virasat, Spirit of Kashmyr and Morpheus Rare Luxury Whisky are also gaining traction across markets. EBITDA margin expanded 300 bps aided by benign grain and ENA prices, with the balance driven by premiumization and favorable product mix.

View and Valuation

FY26 was yet another year of strong growth (25% revenue) and margin expansion (+300 bps). We, therefore, revise our net income estimate upwards by 11% / 6% for FY27E and FY28E, respectively. Therefore, we raise our target price to INR 3,950 (vs. 3,410) using the DCF approach. We forecast a net revenue CAGR of 15.8% over FY26– FY29E and expect EBITDA margin to expand by 107 bps conservatively. We upgrade to ‘BUY’, given an upside of 15.9%.

EBITDAM +531 bps in Q4FY26 Supported by Mix Improvement

* RDCK reported a volume growth of 4.0% YoY: P&A segment volume +27.9%, while Popular segment volume saw a degrowth (-10.2% YoY), due to a high base in Q4 FY25

* Net Revenue for Q4FY26 came in at INR 15.0 Bn, growing by 15.3% YoY (in line with CIE estimate). This was primarily driven by the growth in P&A and Bulk Alcohol segments (~28% of revenue), which saw a revenue increase of 29.1% and 20.9% YoY, respectively

* EBITDA margin came in at 18.9% (outperforming our estimate of 14.4%), improving by 531 bps, supported by lower RM cost and revenue mix moving towards P&A.

* PAT improved by 94.9% to INR 1.79 Bn, outperforming CIE estimate by ~24%, leading to a PAT margin of 11.9%

P&A Volume Expanding at a CAGR of 18.2% over FY26–FY29E

RDCK continued to build on its premium growth strategy in Q4FY26 through portfolio expansion, on-trade penetration and traction in Maharashtra MML. The company’s focus remained on scaling up highvalue brands and improving channel mix. Looking ahead, management has guided for 120–125 bps EBITDA margin expansion in FY27E, supported by a favourable mix shift, stable input cost and continued premiumization. RDCK’s disciplined execution, higher traction across multiple brands and categories, product innovation help us to forecast a rise in P&A category volume salience to 52.6% (FY26: 43.6%). We forecast a total net revenue CAGR of 15.8% over FY26–FY29E.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

600-400.jpg)