Buy Polycab India Ltd for the Target Rs.9,800 by Motilal Oswal Financial Services Ltd

Soft C&W volumes; positive margin surprise in FMEG

Market share gain continues; long-term growth and margin firm

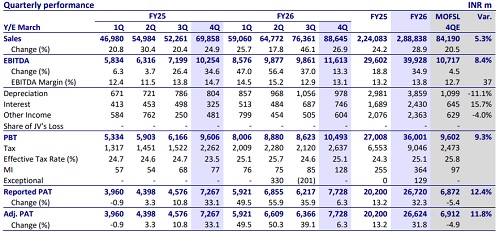

* Polycab’s (POLYCAB) 4QFY26 revenue/EBITDA grew ~27%/13% YoY to INR88.6b/INR11.6b (~5%/8% beat). Cable & wire (C&W) revenue increased ~29% YoY to INR77.6b (~5% beat) and FMEG revenue grew ~39% YoY to INR6.6b. (~22% beat). OPM dipped 1.6pp YoY to ~13% (+40bp vs. our est.), led by a decline of 2.0pp in C&W margin at 13.1% (in line). Adj. PAT was up ~6% YoY at INR7.7b (~12% beat).

* Management highlighted that C&W volume growth in 4Q was in low single digits due to geopolitical disruptions, March demand slowdown, and channel destocking amid raw material volatility. However, FY26 volumes grew ~18%, ahead of industry, reflecting continued market share gains (4pp YoY gain in FY26). It guided sustainable margin in the range of ~11- 13% in the long term. It guided the company’s growth to be 1.5x of industry growth and exports are expected to scale from ~5% of revenues to ~10% by FY30. Capacity utilization remains at ~75%, with aggressive capex ensuring no bottlenecks and supporting growth.

* We increase our EPS estimates for FY27/FY28 by ~3%/5% on account of higher revenue growth in C&W and slightly better margins in FMEG. The stock is currently trading at 42x/34x FY27E/FY28E EPS. We value POLYCAB at 40x FY28E EPS to arrive at our revised TP of INR9,800 (earlier INR9,350). Reiterate BUY.

C&W margin down 2pp YoY to ~13%; FMEG margin up 4pp

* Consolidated revenue/EBITDA/PAT stood at INR88.6b/INR11.6b/INR7.7b (+27%/+13%/+6% YoY and +5%/+8%/+12% vs. estimates). Gross margin contracted 2.1pp YoY to 23.4%. OPM dipped 1.6pp YoY to ~13%. Ad spend accounted for 0.6% of revenue vs. 0.4%/1.2% in 4QFY25/3QFY26.

* Segmental highlights: C&W revenue rose ~29% YoY to INR77.6b, EBIT increased ~12% YoY to INR10.2b (+5% vs. estimate), and EBIT margin declined 2pp YoY to ~13% (in line). FMEG revenue grew ~39% YoY to INR6.6b, EBIT jumped 15x YoY to INR292m (2.2x above our estimate), and EBIT margin expanded 4pp to ~4%. EPC and other’s revenue declined ~9% YoY to INR4.5b, EBIT fell ~33% YoY to INR269m, and EBIT margin contracted 2.1pp YoY to 6.0%.

* In FY26, revenue/EBITDA/PAT stood at INR288.8b/INR39.9b/INR26.6b (up ~29%/35%/32% YoY). OPM expanded 60bp YoY to 13.8%. C&W revenue/EBIT rose ~33% (each) YoY to INR255.3b/INR34.8b and EBIT margin remained flat YoY at 13.6%. OCF stood at INR38.1b vs. INR18.1b in FY25. Capex stood at INR14.8b vs. INR9.7b in FY25. FCF stood at INR23.3b vs INR8.4b in FY25.

Key highlights from the management commentary

* Structurally, C&W demand remains robust, driven by power sector capex, real estate momentum, manufacturing investments, and emerging segments like data centers, EV infrastructure, and defense.

* 4Q EBITDA margins stood at ~13.1%, impacted by multiple factors, including higher institutional mix, weaker export mix due to Middle East disruption, and softer operating leverage due to weak Mar’26 demand.

*Annual capex guidance remains at INR12b-16b, and management reiterated that there will be no scenario where the company runs out of capacity given its proactive investment approach. Under Project Spring, the company remains on track to execute INR60b-80b of capex over the next five years.

Valuation and view

* POLYCAB’s 4QFY26 operating performance was above our estimates, mainly led by better-than-estimated revenue and margin in FMEG, while C&W margin was in line with our estimates. There have been several near-term challenges due to external factors; however, the demand outlook remains strong for the next 2-3 years. Its continued proactive capex ensures no capacity constraints and positions it well to capture demand recovery and maintain strong growth.

* We estimate a CAGR of 19% in POLYCAB’s revenue/EBITDA each and ~18% in PAT over FY26-28. We estimate OPM to range around 13.5-14.0% in FY27/28 (average ~13.5%). Cumulative OCF during FY27-28E is expected to be at INR48.6b vs. INR56.2b during FY25-26 (higher due to sharp increase in acceptances). We estimate a cumulative capex of INR26.0b over FY27-28 vs. INR24.5b over FY27-28. The company’s net cash balance is estimated to increase to INR47.8b vs. INR41.5b in FY26. We value POLYCAB at 40x FY28E EPS to arrive at our revised TP of INR9,800 (earlier INR9,350). Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412