Buy Chalet Hotels Ltd for Target Rs. 920 by Choice Institutional Equities

Brand-led Expansion in High-barrier, High-ARR Markets

CHALET’s growth is expected to be driven by brand-led expansion across high-barrier airport and premium leisure markets. While business hotels currently account for ~89% of FY25 keys, the mix is expected to moderate to ~80% by FY30E as resorts increase to ~20%, enhancing portfolio diversification. Business assets are expected to continue driving occupancy, while leisure properties support higher ARR realisation. Backed by expansion in airport - adjacent locations and leisure destinations, CHALET is expected to deliver blended occupancy of ~73%, with an ARR of ~INR 16,030 by FY29E. This is expected to help balance stable corporate demand with highARR leisure upside across cycles. Further, launch of the in-house luxury brand Athiva with 147 operational keys and ~510 under construction is expected to strengthen pricing control and improve return metrics

Asset-sweating Platform with Multi - income Streams

CHALET maximises returns from owned real estate, generating diversified cash flows beyond room revenues. Supported by its Marriott partnership, hotels have sustained ~72–73% occupancy, with ARR increasing from INR 9,169 in FY23 to INR 12,094 in FY25 (CAGR ~15%). Annuity commercial assets contribute ~9–11% of revenue but deliver ~83% EBITDA margin, providing stable rental cash flows. The total commercial leased area stands at ~2.4 msf, expected to expand to ~3.3 msf by FY27E. Additional monetisation through one-time residential sales (~INR 14 Bn revenue expected) and F&B (~20–25% of net revenue) enhances revenue per square foot, positioning CHALET as a defensive, cash-generative hospitality platform.

Operational Excellence and Financial Discipline

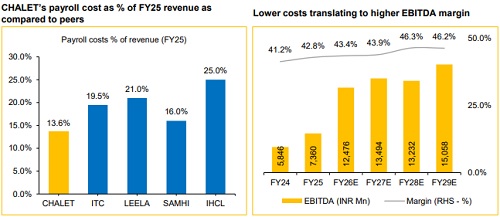

CHALET operates with a structurally efficient cost framework enabling margin resilience. Total operating expenses were ~55.3% of FY25 revenue, significantly lower than peers, supported by industry’s lowest staffing cost (~13.6% of net revenue) and a ~1.0x staff-to-room ratio. This efficiency drives strong operating leverage, with EBITDA margin supported at ~43% in FY25 and expected to peak at ~46% by FY28E, led by ARR-driven RevPAR growth and tight cost control. Strong cash generation supports self-funded growth, even as management plans ~INR 29 Bn of capex over the next three years, with operating cash flows expected to rise from ~INR 9.5 Bn in FY25 to ~INR 12.5 Bn by FY29E. We expect ROCE to reach ~15% in FY26E, and to sustain at that level.

View and Valuation: We believe CHALET offers a differentiated hospitality investment case, driven by disciplined asset sweating supporting balancesheet-led growth. Excluding one-time residential impact, we forecast Revenue/Adj. EBITDA at a CAGR of 15.1% / 15.8% over FY26E - 29E respectively. We initiate coverage on CHALET with a BUY rating and an FY28E EV/Adj. Hospitality EBITDA of 18.0x and assign 14.0x on Annuity EBITDA to arrive at a TP of INR 920, implying an upside potential 28.2%.

Key Risks: Extended geopolitical conflict, lower ARR, slower uptake of Athiva, unoccupied annuity assets.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131