Buy Titan Company Ltd For Target Rs.4,000 by Motilal Oswal Financial Services Ltd

Steady performance; EBIT margin guidance intact

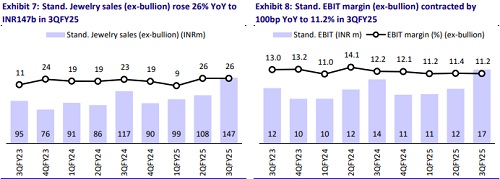

* Titan Company (TTAN) posted consolidated sales growth of 25% YoY in 3QFY25 (in line). Standalone jewelry sales (excl. bullion) rose 26% YoY, driven by strong festive demand, higher gold prices, and a 29% surge in wedding purchases. Studded jewelry grew 21% YoY, though its mix declined by 100bp YoY to 23%. The non-solitaire segment saw healthy double-digit growth, while solitaire sales remained subdued. Net jewelry store additions stood at 46 in 3Q, bringing the total count to 1,055. Standalone Jewelry LFL growth was 22%, and CaratLane posted a robust 25% YoY growth.

* Standalone jewelry EBIT margin (excl. bullion, adjusted for customs duty) contracted 100bp YoY to 11.2% (est. 11.1%) due to a higher gold mix amid rising gold prices. However, CaratLane’s margin expanded 250bp YoY to 11.7%. Management reiterated its standalone EBIT margin guidance of 11- 11.5%.

* Watches segment grew 14% YoY. Analog watches saw strong traction, with Fastrack, Titan, and Helios growing 27%, 31%, and 47% YoY, respectively. However, wearables revenue declined 20% due to an 8% drop in ASP and a 7% dip in volume.

* With the jewelry industry seeing faster formalization, we continue to believe TTAN will keep leveraging the same, driven by store additions, multi-format presence, better designs and customer understanding, and a strong recall of trust. We reiterate our BUY rating with a TP of INR4,000.

Robust growth with in-line Jewelry EBIT margin

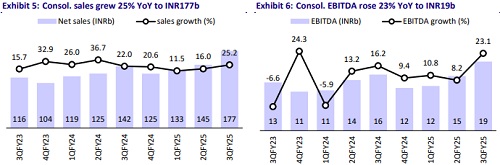

* Healthy revenue growth: TTAN’s consolidated revenue grew 25% YoY to INR177.4b (est. INR184b). Consolidated jewelry sales grew 27% YoY to INR161.3b (est. INR167.0b) (excl. bullion, sales grew 27% to INR160b). Standalone sales (excl. bullion) grew 26% to INR147.0b (est. INR145.1) and CaratLane’s sales grew 25% YoY. The number of jewelry stores grew 17% YoY to 1,055. Watches/Eyewear clocked revenue growth of 15%/17% YoY, while Others remained flat YoY.

* Margin contraction in line with expectations: After adjusting the customs duty effect of INR2.53b, consol. gross margin contracted 120bp YoY to 22% (est. 23%). EBITDA margin contracted 20bp YoY to 10.9% (est. 10.1%). Standalone jewelry EBIT margin (excl. bullion) contracted 100bp YoY to 11.2% (est. 11.1%). CaratLane’s EBIT margin expanded 250bp to 11.7%. Watches’ margin expanded 380bp to 9.5% and eye care margin rose 250bp YoY to 10.2%.

* Double-digit growth in profitability: After adjusting the customs duty effect, EBITDA grew 23% YoY to INR19.3b (INR18.5b). PBT was up 20% YoY at INR16.5b (est. INR16.1b), and Adj. PAT rose 18% YoY to INR12.5b (est. INR12.2b).

* In 9MFY25, net sales grew 18%, EBITDA (adjusted) rose 15%, and APAT grew 6%.

Highlights from the management commentary

* 4Q demand started strong in early January, but the company remains cautious due to record-high gold prices and global volatility.

* Gold lease rates are rising due to US tariff-related changes, leading banks to increase lease costs. The company is monitoring this closely.

* New vs. repeat customer mix in 3Q stood at 48:52. Festive periods typically attract a higher number of new buyers. Growth was driven by both an increasing buyer base and higher ticket sizes.

* GC (gross contribution) margin dilution in studded jewelry was due to a shift in the gold-to-diamond ratio within diamond jewelry amid rising gold prices and stable diamond prices. The company plans to offset this through better material sourcing and cost efficiencies.

Valuation and view

* We maintain our EPS estimates for FY25/FY26.

* TTAN, with its superior competitive positioning (in sourcing, studded ratio, youth-centric focus, and reinvestment strategy), continues to outperform other branded players. The brand recall and business moat are not easily replicable; therefore, Tanishq’s competitive edge will remain strong in the category. The store count reached 3,240 as of Dec’24, and the expansion story remains intact.

* EBITDA margin has been contracting in FY25 owing to a lower studded mix. It will be critical to monitor the margin outlook amid intensifying competition. The non-jewelry business is also scaling up well and will contribute to growth in the medium term.

* We model a CAGR of 17%/19%/22% in revenue/EBITDA/PAT during FY25-27E. TTAN’s valuation is rich, but it offers a long runway for growth with a superior execution track record. Reiterate BUY with a TP of INR4,000.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412