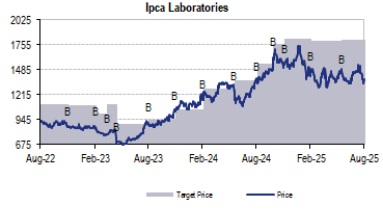

Buy Ipca Laboratories Ltd for the Target Rs. 1,767 by JM Financial Services Ltd

PCA reported mixed numbers in 1QFY26, with revenue, EBITDA, and PAT growing 10%, 6%, and 21% year-on-year respectively. While revenues were in line with expectations, EBITDA and PAT missed estimates by 5% and 12%. EBITDA margins stood at 18%, down 73 basis points YoY, impacted by certain one-offs and increased costs during the quarter. Among key segments, the India business grew 10% YoY, slightly below expectations as the Cardiac therapy segment saw slower growth due to an ongoing restructuring that affected its performance. In exports, the generics segment performed well with 19% growth, along with API exports which rose 28%. However, the performance of subsidiaries remained muted with overall growth of 7%, with Unichem’s growth at 9%. Looking ahead, the company has maintained its consol. topline guidance at 9–10% but lowered its margin expansion guidance to 75bps from 100bps earlier, with Unichem likely to remain a drag on performance. We have revised our earnings estimates by -1%, -3%, and -2% for FY26, FY27, and FY28 respectively. In anticipation of this weaker performance, the stock has already corrected 11% from its recent high (Jul-25) and is currently trading at 24x/20x on FY27/28 EPS, which is at a 16%/17% discount to the peer average. We believe this valuation gap is unjustified given the strong performance in the India business, and we value IPCA at 30x to arrive at a target price of 1767, maintaining our BUY rating.

* Domestic portfolio restructuring: The segment grew 7% YoY with strong growth across all therapies except cardio, where the vertical was reorganised with two additional divisions, internal transfers, and new hires, resulting in only 8% YoY growth. IPCA’s acute therapy grew by 9.8% YoY vs IPM’s acute therapy up 6.9% YoY, while IPCA’s chronic therapies grew 15.1% vs IPM’s chronic therapies up 9.9%. In the cardio vertical, 400 new MRs were added, and no large-scale hiring is planned in any therapy for the rest of the year. Work force is at 7,000, with 3–4% annual additions planned across specialty segments including derma, urology, and CNS.

* International growth robust: In US, mngt expects incremental USD 15-16mn revenues from recently launched products. There are 15–16 products under development for the US market. In UK, high competition and excess inventory led to price pressures, though Unichem recorded a good quarter. API export demand is gradually improving, with 2–3 new API products being introduced annually. All new facilities will be commercialised this year, with no commercialisation in 1QFY26.

* Subsidiaries- under pressure: Unichem’s consol. revenue grew 9% YoY. US business up 12% YoY, Myanmar down 62% YoY due to import license delays, Brazil down 33% YoY, and Europe up 37% YoY. SG&A was impacted by provision of INR 120mn for currency fluctuations due to EUR14mn penalty and euro appreciation, and INR 80–100mn for payments in a closed Italian company. A new subsidiary is being set up in Germany, with initial losses expected. Onyx saw GBP 300k Q1 loss (low launches and limited market funding). Pisgah continues to incur losses, similar to last year, but its injectable project, expected to commercialise in 2HFY26, may improve financials.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361