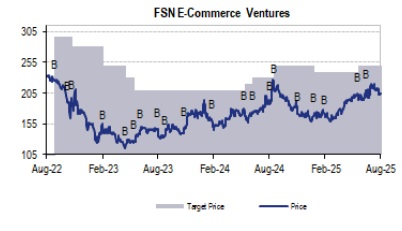

Buy FSN E-Commerce Ventures Ltd for the Target Rs. 260 by JM Financial Services Ltd

Continuing with the recent trend, Nykaa reported another quarter of robust growth with Fashion segment also participating finally. Nykaa BPC delivered 26% GMV growth YoY along with 24% revenue growth while also improving EBITDA margin to 9.0% (+50bps YoY). With growth returning, Fashion segment reported substantial improvement (+300bps YoY) in EBITDA margin to reach INR 180mn in quarterly losses. Overall, the company reported 23% YoY growth in revenue to reach INR 21.6bn with EBITDA margin reaching 6.5% (flat QoQ, +100bps YoY). With core BPC continuing to improve profitability along with a decline in losses in Fashion and eB2B, we expect the company to see accelerated consolidated EBITDA margin improvement. Reiterate ‘BUY’ with Jun’26 TP of INR 260.

* BPC growth momentum continues with margin improvement chugging along: Nykaa BPC reported 26% YoY GMV growth, driven by robust order growth as well as higher AOV (4% YoY), primarily due to premiumisation. Offline retail was also strong (33% YoY) supported by double digit SSSG growth and accelerated store expansion with 250 stores in 82 cities. Furthermore, our triangulation suggests that core BPC (excluding eB2B and Nykaa Man) was at 25%/24% GMV/NSV growth, suggesting sustained strength despite tepid demand environment. Core BPC GM improved 190bps YoY due to rising owned brands salience. However, CM expansion was slower at 70bps YoY due to increase in marketing spends on account of increasing mix of owned brands, hence core BPC EBITDA margin improved only 20bps YoY. We expect the segment to sustain revenue growth along with margin improvement driven by sharper expansion of House of Brands and Physical store margins, along with 30-40bps annual expansion in online platform margin.

* Fashion GMV gains further momentum with margins improving strongly: Nykaa Fashion reported GMV/NSV growth of 25%/20% YoY, indicating recovery for 2nd consecutive quarter. Revenue growth however was lower at 15% YoY due to muted performance of Fashion owned brands and lower LBB mix. Gross margin dipped 20bps YoY and increase in fulfilment expenses by 140bps resulted in contribution margin (as % of NSV) dipping 210bps YoY to reach 8.0%. However, scale efficiencies in Other expenses enabled sharp EBITDAM rise of 304bps. The segment remains on track to deliver EBITDA breakeven in FY26. Management noted that margin expansion is structural in nature and will continue to improve as the business scales. Furthermore, besides women category, Men and Kids are gaining share in the mix with 16% / 5% share respectively as of 1QFY26.

* Reiterate ‘BUY’, Jun’26 TP rises to INR 260: Despite unfavourable demand environment, Nykaa has delivered against the odds to improve margins while delivering industry-leading growth across segments. Our numbers remain largely unchanged with revenue estimates declining marginally while EBITDA margin improves slightly. We expect the company to sustain growth momentum with higher BPC profits getting unburdened of the losses in Fashion and eB2B gradually. We roll forward to Jun’26 TP of INR 260 (INR 250 earlier) as Nykaa remains one of the highest compounding consumption plays in India with track record of delivering across cycles and even against aggressive competition. Reiterate BUY.

* Superstore growth remains robust but profitability will be gradual: Nykaa’s eB2B platform, ‘SuperStore’ (which is part of BPC segment from 1QFY25 onwards) continues to see strong GMV growth of 40% YoY, reaching 305k retailers in 1,110+ cities. Superstore now contributes ~9% to BPC GMV. Gross margin improved 139bps YoY (driven by increasing share of House of Nykaa brands (~7x YoY increase), premium brands and higher service income while contribution margin improved sharply with 309bps YoY due to reduction in freight and packaging cost as company shifts from 3 rd party warehouses to owned warehouses leading to reduction in fulfilment costs. As the business scales, operating leverage kicks in, as evident from 515bps YoY EBITDAM improvement. We expect Superstore business to turn contribution profitable in H2FY27 with EBITDA profitability anticipated in H2FY29.

* Owned brands remain strong with Fashion owned brands seeing strategic distribution channel shift to Nykaa platform: Beauty owned brands have shown strong GMV growth of 70% YoY to reach INR 5.8bn in 1QFY26 driven by strong growth in Dot & key (1QFY26 GMV run rate of INR 15bn+), Nykaa Cosmetics (1QFY26 GMV run rate of INR 3.5bn) and Kay Beauty (1QFY26 GMV run rate of INR 2.5bn+). Meanwhile, Fashion owned brands GMV grew 7% YoY to reach INR 0.97bn in 1QFY26. In Fashion, Nykd has reached INR 1.7bn+ (~3x in 3 years) in 1QFY26. For Fashion brands, company will be refining assortment with focus on only select brands. As 3P fashion marketplaces have struggled for growth, company has revamped its channel strategy by driving higher mix from Nykaa Fashion platform (+26% YoY). Overall, Nykaa’s house of brands portfolio has crossed INR 27bn GMV mark.

* Nykaa Now penetration rises: Nykaa has expanded ‘Nykaa Now’ into India’s most comprehensive rapid-delivery beauty platform, offering the widest range of luxury, FMCG, and D2C beauty products with delivery in 30-120 minutes. The service is live in 7 cities through 50+ rapid delivery stores, having fulfilled 1.3mn+ orders till date. Supported by Nykaa’s integrated network of warehouses, offline stores, and rapid hubs, Nykaa Now addresses growing demand for speed and convenience while maintaining brand experience and product quality. Management noted that it already offers the largest assortment of beauty products for rapid delivery in India and is scaling sustainably with strong resonance among urban consumers while not impacting BPC fulfilment expenses much.

* Nykaa Fashion Edit: Nykaa Fashion introduced Nykaa Fashion Edit, a curated shopping property designed to position the platform as India’s leading style destination. The Edit features occasion-based, festive, and influencer-led stores, combining manual curation with tech-enabled trend-scraping to refresh assortments in real time. This format aims to move beyond transactional retail into a discovery-driven experience, deepening engagement and elevating brand equity.

* BPC EBITDA Margin expansion sustained despite investments in customer acquisition: With the management aggressively investing into new customer acquisition, there has been significant reinvestment in order to broaden the customer funnel. Though, core BPC contribution margin declined sequentially by 50bps, it was mainly due to higher marketing spend on owned brands which are in high growth phase and also have the gross margins to absorb the higher marketing expense. However, it needs to be noted that CM improved 70bps YoY to reach 26.2% despite these investments. With revenue growing in mid-twenties, Nykaa BPC segment is expected to deliver sustained EBITDA margin expansion to reach 12.7%/13.7% in FY27/FY28 from 11.2% in FY25. Our triangulation of BPC mix across eB2B, Physical Stores, Private Labels and Online Platform suggests that Nykaa’s online platform is currently operating at 14% EBITDAM with 30- 40bps annual expansion likely over the next couple of years. However, other channels of BPC are expected to deliver a much sharper margin enhancement to drive mix-related margin accretion.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361

.jpg)