Buy ICICI Prudential Life Insurance Company Ltd for the Target Rs. 710 By Prabhudas Liladhar Capital Ltd

Growth momentum to pick up; margin improves

Quick Pointers:

* Weak APE growth in Q2; expect volumes to pick up in H2

* Margin improves to 24.4%; drag from GST exemption to reflect in H2

Q2 APE grew -3% YoY on an unfavourable base due to a decline in ULIP. We expect the momentum to pick up in H2FY26 (15.5% YoY growth), led by uptick in credit life/ ULIP and healthy traction in retail protection and NPAR. VNB margin expanded to 24.4% in 2QFY26 led by a favourable shift in product mix. Shift towards NPAR, higher sum assured and rider attachment rates are likely to offset the drag on profitability from GST exemption. We make marginal changes to our FY26/ FY27E APE growth estimates and increase FY26/ FY27E VNB margin factoring in a strong margin profile in H1FY26. We use the appraisal value framework to value IPRU at a TP of Rs710 (1.9x FY27E P/EV). Retain BUY.

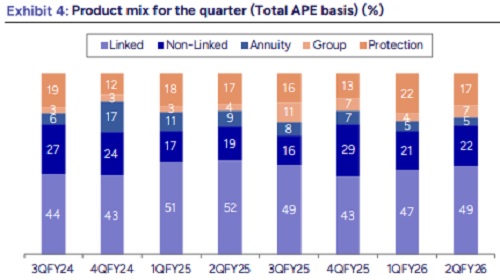

* Expect growth to pick up in H2: IPRU Life saw weak APE growth in 2QFY26 (-3% YoY) due to a decline of 8.5% YoY in ULIP. Protection growth remained flat YoY affected by (1) soft growth in retail protection (1.8% YoY) on a high base and (2) weakness in credit life volumes, especially in MFI. Within the Nonlinked portfolio (+11.9% YoY), company highlighted a favourable mix with a shift in customer preference towards NPAR vs. PAR products. Linked / NonLinked / Annuity / Group / Protection comprised 49.0% / 22.1% / 4.8% / 6.8% / 17.3% of APE in 2QFY26. Company expects strong growth in H2, factoring in a benign base, pick-up in credit life and ULIP volumes and sustained demand in retail protection and NPAR. We build an overall APE growth of ~7% in FY26E, driven by a strong H2FY26E (+15.5% YoY over H2FY25).

* VNB margin improves; drag of GST exemption in H2: While 2QFY26 VNB grew 1% YoY to Rs 5.9 bn, Q2 VNB margin rose to 24.4% (H1FY26 VNB Margin at 24.5%) mainly on account of a favourable product mix (shift towards NPAR). Company continues to engage with distributors on lower commissions and is evaluating several cost optimisation measures to mitigate the impact of the recent GST exemption on FY26 VNB. Higher sum assured/ rider attachment and favourable movement of the yield curve are likely to offset the drag on profitability. While we expect H2 VNB margin to be lower at 23.4% due to the impact of GST exemption, we increase our FY26/ FY27E VNB Margin estimates by 80/90 bps to 23.8%/ 24.3% to account of betterthan-expected performance in H1FY26.

* Impact of ~1% on FY26 EV; persistency trends normalise: Embedded Value grew by 9.7% YoY to Rs 505bn and company has indicated an impact of ~1% on FY26 EV due to the benefit of input tax credit not being available on the existing book. 13M persistency normalised to 85.3% (in-line with FY23 levels) while company highlighted a drop in 61M persistency due to a change in definition. AUM was flat YoY at Rs 3,214.9 bn and company will be exercising a call option for Rs 12bn of sub-debt in Nov-25. Post exercising the call option, it expects the solvency ratio to remain above the regulatory threshold of 150% (currently at 213%).

* Prop channels to do the heavy lifting in H2: Agency/ Direct/ Banca/ Partnership Distribution/ Group contributed 24.9%/14.9%/30.6%/12.6%/17.1% to overall APE in 2QFY26. Proprietary channels (agency and direct) saw a degrowth of 23%/ 9% YoY on a high base and company expects a pick-up in H2. Banca APE was flat YoY and the run-rate for ICICIB was stable (Rs ~1 bn per month). H1FY26 Total Cost/ TWRP improved to 19.2% (vs. 22.0% in H1FY25) and company highlighted positive operating leverage resulting in an improved margin profile.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271