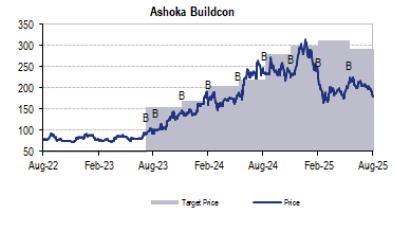

Buy Ashoka Buildcon Ltd for the Target Rs. 243 by JM Financial Services Ltd

Ashoka Buildcon’s (ABL) 1Q26 PAT at INR 306mn (down 25% YoY) missed JMFe/consensus estimate of INR 859mn/INR 612mn due to sharply lower revenue. Execution was impacted due to monsoon and delay in start of newly won projects. While ABL maintained its revenue growth guidance of 10% for FY26E, we believe it is optimistic given weak execution in 1Q and expected weakness in 2Q as well. We have factored flat revenue in FY26. ABL lowered its margin guidance from 10%+ to 9.5-10% for FY26E given the weak 1Q. ABL is confident of ramping up execution in 2H26. Asset monetization remains delayed. ABL now targets to monetize 5 BOT assets by Sept-25 (but will receive only part payment of c.INR 18bn and remainder INR 7bn would come in FY27 on completion of certain condition precedents), 5 HAMs by Sept-25 (inflow of INR 12bn), 4 HAMs in Dec-25 and 2 HAMs by June-26 (inflow of INR 11bn). There is no clarity on monetization of Jaora Nayagaon and Chennai ORR and we have removed it from valuation as well. Given the lower execution, we have cut EPS by 15%/8%/4% for FY26/27/28E. Valuations remain attractive at10x/8x FY27/28 core EPS (adjusted for assets). Maintain BUY with revised SOTP based price target of INR 243.

* 1Q26 PAT missed JMFe due to lower revenue: ABL’s revenue declined decline sharply by 30% YoY to INR 13bn (JMFe: INR 20bn) impacted by monsoon and delay in execution of newly won projects. EBITDA grew by 1% YoY to INR 1.2bn (JMFe: INR 1.9bn) on low base, while EBITDA margins expanded by 70bps YoY to 9.3% on adjusted base (JMFe: 9.5%). Interest costs grew by 27% YoY to INR 841mn (JMFe: INR 750mn) due to higher debt levels. Other income grew by 20% YoY to INR 285mn (JMFe: INR 240mn). Gross debt rose QoQ from INR 20.6bn in Mar-25 to INR 24bn in June-25 (June-24: INR 19.5bn).

* Execution to improve in 2H26; maintains revenue guidance: With order inflows of INR 25.4bn, ABL’s order backlog stood to INR 159bn (2.4x TTM revenues) as of June-25. Backed with robust bid pipeline across verticals, ABL expects order inflows of INR 100- 120bn for FY26E. Despite revenue de-growth in 1Q26, ABL maintained its revenue growth guidance of 10% for FY26E which in our view is optimistic and have factored flat revenue. ABL lowered margin guidance from 10%+ to 9.5-10% given weaker 1Q26

* Asset monetization delayed; proceeds will help pare debt: Asset monetization remains delayed. ABL now targets to monetize 5 BOT assets by Sept-25 (but will receive only part payment of INR 18bn and remainder INR 7bn would come in FY27 on completion of certain condition precedents), 5 HAMs by Sept-25 (inflow of INR 12bn), 4 HAMs in Dec25 and 2 HAMs by June-26 (inflow of INR 11bn). These proceeds will help pare debt

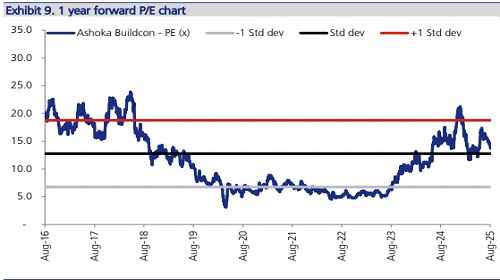

* Maintain BUY with SoTP based revised price target of INR 243: Given the lower execution and margins and delay in asset monetization, we have cut EPS sharply by 15%/8%/4% for FY26/27/28E. Having said that, we expect robust core EPS CAGR of 49% over FY25- 28E mainly led by revenue growth and margin expansion in FY27/28E. Currently, ABL trades at 10x/8x FY27/28E core EPS (ex-other income) after adjusting for value of assets. Current valuations at discount to peers but have room to re-rate if asset monetization goes as planned. We value ABL’s EPC business at 11x FY27E core EPS, assets at INR 92 on P/B basis to arrive at an SOTP-based revised price target of INR 243. Maintain Buy.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361