Reduce Tata Elxsi Ltd For Target Rs. 5,010 By Prabhudas Lilladher Capital Ltd

Improved performance lay foundation for better H2

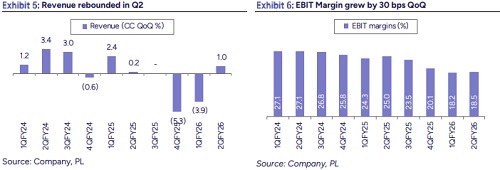

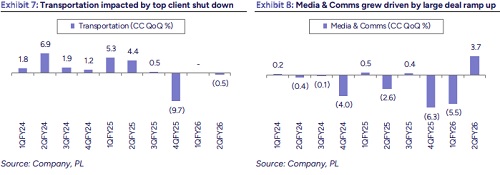

The revenue growth exceeded our estimates with 1% QoQ CC growth & margin improvement of 30bps. Surprisingly, the overall revenue impact on the cyber incident for its top account turns out to be less severe (50-100bps QoQ) than anticipated. Additionally, the ramp up of two large deals within Automotive space compensated the drag within its top account. The underlying demand for Automotive OEMs is recovering, the projects that were kept on hold are being resumed and even the newer projects are seeing timely executions. Although the current growth profiles of US/Europe OEMs are weak, the strong intent to participate and compete against Chinese OEMs are driving the futuristic investments in SDV, ADAS and Connectivity areas. Beyond Automotive, the underlying demand within M&C remains challenging, while Healthcare should drive growth in H2 backed by multiple wins. On margin, it has fairly exceeded our estimate by 100bps QoQ, hence we are passing the benefits to FY26. We are revising our margins up by 20bps/40bps/60bps due to Q2 beat for FY26E/FY27E/FY28E. We expect CC revenue to decline by 5.1% (-5.9% QoQ earlier) in FY26E and grow by 9.4%/11.2% YoY in FY27E/FY28E. Considering the early green shoots on Transportation, we are assigning 36x PE to Sep’27 EPS, translating a TP of 5,010. Upgrade to REDUCE (SELL earlier).

Revenue: TELX reported revenue ahead of both our and consensus estimates, supported by the ramp-up of a large deal in the Media & Communications segment and only a modest decline in Transportation. Revenue grew 1% QoQ in CC terms, compared to our expectation of a 1.9% QoQ decline & consensus estimate 0.9% QoQ decline in USD. The beat was driven by a 3.7% QoQ CC increase in Media & Communications, while Transportation saw a mild 0.5% QoQ CC contraction and Healthcare declined by 4.6% QoQ CC.

Operating Margin: TELX delivered an EBIT margin of 18.5%, improving 30 bps QoQ and beating our expectation of an 80 bps decline. The margin outperformance was primarily driven by higher-than-expected revenue. EBIT came in at Rs. 1.69 bn, up 4.6% QoQ. PAT for the quarter stood at Rs. 1.55 bn (up 7.2% QoQ), translating into a PAT margin of 16.9%.

Deal Wins: TELX secured several notable large deals, including a multi-year, multiyear multi-million-dollar partnership with Bayer Devices to co-develop advanced radiology products. In Aerospace & Defence, the company won a turnkey airport guidance systems development contract from a US-headquartered supplier. Management also indicated that multiple large deal pursuits are currently underway, signaling sustained momentum in the pipeline.

Valuations and outlook: We estimate USD revenue/earnings CAGR of 5.2%/9.3% over FY25-FY28E. The stock is currently trading at 40x LTM Sep 27E earnings, we are assigning P/E of 36x to LTM Sep 27E earnings with a target price of INR 5,010. We upgrade to stock to “REDUCE” from Sell rating earlier.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

600-400.jpg)