Reduce Sansera Engineering Ltd For Target Rs. 1,460 By Choice Broking Ltd

Future-focussed Growth, Limited Upside

Strategic Diversification and High-growth Non-Auto Focus: The Aerospace, Defence and Semiconductor (ADS) segment is a key strategic focus for SANSERA and is identified as the primary long-term growth driver for the non-auto business. The management expects ADS to contribute INR 3,000–3,200 to revenue in FY26. The company is actively pursuing high-value added products in ADS and moving towards higher value per part. The ADS division delivered a top line of INR 496 Mn in Q2FY26 and the current capacity for ADS can cater up to about INR 6,000 to 6,500 Mn of the existing orderbook. This segment is showing resilience to geopolitical developments owing to diversified end markets and exemption to aerospace customers. We believe SANSERA's diversified portfolio in segments (auto, non-auto), geographies, customers and product ranges positions it well to navigate market disruption and deliver profitable growth.

View and Valuation: We revise our FY26/27E EPS estimate downwards by 1.8%/0.1% and maintain our target price of INR 1,460. We value the company at 25x (maintained) on the average FY27/28E EPS. We maintain our ‘REDUCE' rating on the stock, considering the current valuation and limited upside potential from the present level.

Revenue, EBITDA in line; PAT Better than Estimate

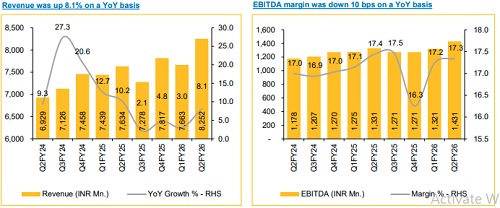

* Revenue was up 8.1% YoY and up 7.7% QoQ to INR 8,252 Mn (vs CIE est. at INR 8,244 Mn).

* EBITDA was up 7.5% YoY and up 8.3% QoQ to INR 1,431 Mn (vs CIE est. at INR 1,443 Mn). EBITDA margin was down 10 bps YoY and up 10 bps QoQ to 17.3% (vs CIE est. at 17.5%).

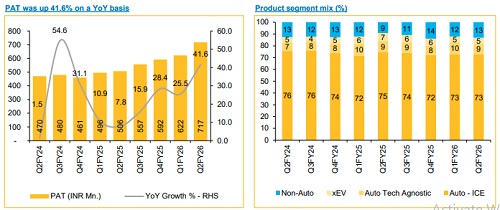

* APAT was up 41.6% YoY and up 15.3% QoQ to INR 717 Mn (vs CIE est. at INR 665 Mn).

Robust Order Book and Revenue Visibility: As of September 30, 2025, SANSERA boasted of a robust order book of INR 21,458 Mn. More than 60% of the orders originate from international sources, providing significant revenue visibility. These orders were primarily from the ADS segment (35%), xEV (7%), tech agnostic (10%), PV+CV (31%) and the 2W segment (17%). The company is engaging with new as well as existing customers who are exploring a transition, from in-house production to outsourced solutions.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131