Reduce Fusion Finance Ltd for the Target Rs.170 By Emkay Global Financial Services Ltd

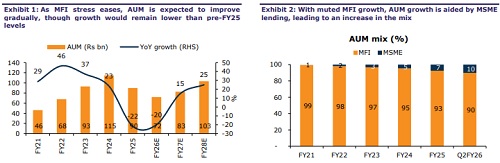

Survives existential risk, although full turnaround will take time

We met Fusion’s new MD and CEO, Sanjay Gayali, to discuss the ongoing business transformation initiatives and the MFI recovery story, with early green shoots visible across the industry. While the new MD has not directly managed MFI business in the past, he comes from pedigreed institutions, and is focusing on strengthening assurance, risk, and control functions to prevent a recurrence of past lapses that led to near-existential risk for Fusion. He indicated that net flow forward into the PAR 0+ bucket has stabilized at 0.5-0.6%, from a high of ~3% last year, while X bucket’s collection efficiencies have improved to 98.5%, leading to lower formation of fresh stress and thus, credit cost. With capital in place (second tranche of Rs4bn to come soon) and stress flow rates easing, disbursements are also picking up. Fusion may soon turn profitable on a quarterly basis, although we believe that full business turnaround and regaining old charm will take time, subject to no further external shocks. Thus, we retain REDUCE with a TP of Rs170 (1x Sep-27E ABV). Within the MFI space, we prefer South-based players, including Ujjivan SFB and CREDAG, for now; we will remain watchful of Fusion’s turnaround.

Focus on fixing operational gaps before the next leg of growth begins

Fusion has undertaken significant governance reforms, making assurance, risk, and other key control functions fully independent and delinking them from business KPIs. Decisionmaking, earlier concentrated among a few individuals, has now been broadened, easing the load on the MD and CEO and improving supervision across functions. As part of guardrail reinforcement, credit personnel have been placed across ~250 large branches to meet customers directly and ensure adherence to guardrails and bureau data norms. Process and operational gaps have been fixed and thus, fresh disbursements (Rs13bn in 2Q, up 37% QoQ) have accelerated as well. Margins inched up by 55bps QoQ to 10.9% in 2Q due to lower stress flow and cost management. The management expects margins in the stable-to-positive zone as borrowing costs ease further; we believe capital infusion too should help the margins.

MFI’s fresh stress flow easing, resulting in lower credit cost

Fusion was early to enter the stress cycle but is now gradually catching up with the MFI recovery story, in line with peers. Gross slippages declined to 6.9% of loans from the high of 25% in 2QFY25, while higher write-offs led to 82bps QoQ improvement in GNPA to 4.6% in 2QFY26. The net flow forward into the PAR 0+ bucket has stabilized at 0.5- 0.6%, from a high of ~3% last year, while X bucket’s collection efficiencies have improved to 98.5%, leading to lower formation of fresh stress and thus, credit cost. The share of Fusion’s customers with exposure to ≥3 lenders has fallen to 13.9% (vs 18.1% in Mar25), though still high vs peers. Regional trends remain resilient, with UP outperforming (CE: 98.6%) and Bihar posting the best recovery rate. Recovery in the hard bucket too has improved with the independent recovery vertical delivering better outcomes.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354