Neutral Shree Cement Ltd For Target Rs.27,000 by Motilal Oswal Financial Services Ltd

Earnings growth and superior profitability priced in

Capacity-led re-rating unlikely

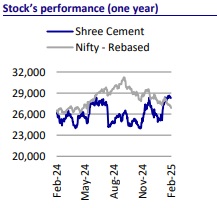

* Shree Cement (SRCM) has outperformed the broader indices and other large players (UTCEM and ACEM) in the last one month, primarily aided by industry-leading profitability in 3QFY25 supported by better cost controls. However, the company disappointed the market with a muted volume growth in 9MFY25 vs. strong volume growth posted by other large players.

* Earlier, during FY14-21, SRCM experienced capacity-led re-rating given its entry into newer geographies, higher capacity utilization, low-cost capacity expansions, market share gain, and a balanced distribution between integrated cement plants and split location grinding units.

* SRCM is anticipated to commission 7.3mtpa (clinker) and 15.4mtpa (cement) capacities in 1QFY26, which will lead to 21%/27% clinker/cement capacity growth. Unlike previously, we do not expect capacity-led rerating this time given the lower capacity utilization, mounting industry supply, lack of geographical distribution, and disproportionate mix of split grinding units and integrated cement plants.

* We estimate SRCM’s EBITDA to clock ~18% CAGR over FY25-27, driven by ~10% volume growth and ~7% improvement in EBITDA/t. We estimate its blended EBITDA/t at INR1,093/INR1,174 for FY26/FY27 vs. INR1,017 for FY25E (average EBITDA/t was INR1,283 over FY20-24). The stock trades at 22x/18x FY26E/FY27E EV/EBITDA (vs. its 10-year average one-year forward EV/EBITDA of 20x). We reiterate our Neutral rating and value SRCM at 17x FY27E EV/EBITDA to arrive at our TP of INR27,000.

Increasing clinker/cement capacities by 7.3mtpa/15.4mtpa in 1QFY26

* SRCM scaled up its capacity expansion plans post-FY22, as its capacity CAGR stood at ~16% over FY23-26E vs. ~5% during FY20-23. The company added 9.3mpta (clinker) and 10.0mtpa (cement) capacities during FY23-25E. In 1QFY26, the company is expected to further increase clinker/cement capacity by 7.3mtpa/15.4mtpa to 42.2mtpa/71.8mtpa.

* It is setting up the following plants: 1) brownfield expansion of 3.7mtpa (clinker) and 6.0mtpa (cement) at Pali, Rajasthan (North); 2) brownfield expansion of 3.7mtpa (clinker) and 3.0mtpa (cement) at Kodla, Karnataka (South); 3) brownfield expansion of 3.4mtpa (cement) at Balodabazar, Chhattisgarh (East); and 4) Greenfield grinding unit at Etah, Western UP (Central).

* SRCM’s expansion plans (up to 75mtpa) are largely focused on existing locations (North, East, and part of South). However, a significant part of the Central and West regions will remain untapped until FY27E. Historically, the company also has a higher share of split grinding unit addition in overall expansions (of the total ~42.9mtpa cement capacity, it added ~25.8mtpa through split GU during FY14-25E). However, this time, out of 15.4mtpa, it will add only 3.0mtpa (~19%) through split GU, while the rest 12.4mtpa is likely to be added at integrated cement plants.

Valuations expensive; reiterate Neutral

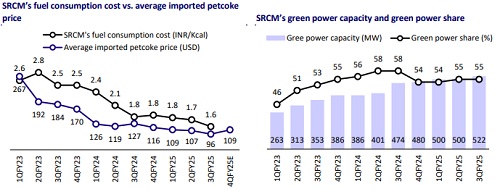

* SRCM is among the least-cost cement producers in the industry, supported by: 1) a higher share of green power (WHRS, solar, and wind power), which meets 55%+ of its power requirements; 2) higher alternative raw material consumption; and 3) lower specific power consumption (68Kwh/t of cement). However, we believe its cost leadership and operational efficiency benefits are already factored into current valuations. Additionally, low capacity utilization, limited regional diversification into newer capacity addition, and rising industry supply (expect ~50mtpa capacity addition in FY26) may constrain any capacityled re-rating in the stock.

* The stock trades at 22x/18x FY26E/FY27E EV/EBITDA (vs. its 10-year average one-year forward EV/EBITDA of 20x). We reiterate our Neutral rating and value SRCM at 17x FY27E EV/EBITDA to arrive at our TP of INR27,000.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412