Neutral Piramal Enterprises Ltd for the Target Rs. 1,085 by Motilal Oswal Financial Services Ltd

Accelerated rundown in legacy AUM; growth businesses improve

Retail opex ratio continues to improve; AIF recoveries remain on track

* Piramal Enterprises (PIEL) reported a 4QFY25 net profit of ~INR1b (PQ: ~INR386m). This included an exceptional gain of ~INR3.7b from recoveries in the AIF portfolio. For FY25, the total gain from the AIF portfolio stood at INR9.2b. FY25 net profit stood at INR4.85b (vs. a loss of INR16.8b in FY24).

* NII rose 28% YoY to ~INR8.5b. PPOP stood at ~INR8.3b (PQ: INR7.1b).

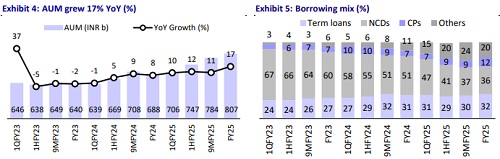

* Total AUM grew 17% YoY and 3% QoQ to INR807b. Wholesale 2.0 AUM rose ~44% YoY and 2% QoQ to INR91.2b, while Wholesale 1.0 AUM declined ~33% YoY/53% QoQ to INR69b.

* Management has guided ~25% YoY growth in total AUM in FY26, primarily driven by a strong ~30% YoY growth in the retail loan segment. The company expects a greater contribution from unsecured products compared to FY25 and intends to scale down its legacy AUM to INR30-35b by FY26.

* PIEL highlighted that asset quality within the growth portfolio remained largely stable. It believes that credit costs for the non-MFI portfolio peaked in 3QFY25, while MFI-related credit costs have likely peaked in 4QFY25. Barring MFI, delinquency trends across other segments remain benign.

* We estimate a total AUM CAGR of ~24% and a Retail AUM CAGR of ~27% over FY24-FY27. While its growth business (excluding one-off gains and exceptional items) is showing signs of improvement, it will still take a few more quarters for the company to mitigate the earnings and credit cost impact of the accelerated decline in the legacy AUM.

* Pockets of opportunity, which we earlier thought would be utilized for inorganic acquisitions in retail businesses or for strengthening the balance sheet, are being directed toward running down the stressed legacy AUM. In the near term, we still do not see catalysts for any meaningful improvement in the core earnings trajectory of the company. We reiterate our Neutral rating with a revised TP of INR1,085 (based on Mar’27E SoTP).

Highlights from the management commentary

* Unsecured disbursements moderated and were down 1% YoY during the quarter vs. secured products, which rose ~22% YoY. The company is going slow in terms of disbursements in business and digital loans. ? The company aims to increase the share of unsecured business by ~4-4.5% in total AUM over the next two years. This shift is expected to be NIMaccretive, contributing positively to margins.

* The company has a tax shield of INR145b, which will ensure that the PAT is equal to PBT for the next few years. Further, the company expects to receive deferred consideration of USD120m in FY26 from the sale of the Piramal imaging business.

* PCHFL, a subsidiary of PEL, was renamed Piramal Finance Limited (PFL) and transitioned from an HFC to an NBFC. PFL is now an Upper Layer NBFC and one of the top 10 private sector NBFCs in India. The company has received the RBI approval for the merger of PEL with PFL and has initiated the NCLT process for approvals, which is expected to conclude around Sep’25.

Retail loans surge ~35% YoY; retail mix improves to ~80%

* Retail AUM grew ~35% YoY to INR647b, with its share in the loan book increasing to ~80% (PQ: 75%). Management shared that the company is going slow in terms of disbursements in business and digital loans.

* Retail disbursements grew ~9% YoY and ~17% QoQ to INR98b. Except for the unsecured business loans, all other product segments exhibited sequential growth in disbursements.

Retail asset quality steady; credit costs broadly stable in growth businesses

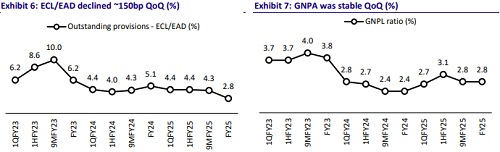

* GS3 was stable QoQ at ~2.8%, while NS3 rose ~40bp QoQ to 1.9%. Stage 3 PCR declined ~14pp QoQ to ~35.7%. As per the policy, the company released a provision of INR1.4b created on the wholesale portfolio during the quarter. Retail 90+ DPD was stable QoQ at ~0.8%.

* Growth business (Retail and Wholesale 2.0) gross credit costs rose ~10bp QoQ to 1.8% (PQ: 1.7%). Total ECL/EAD declined ~150bp QoQ to ~2.8% of the AUM.

Valuation and view

* PIEL delivered a steady quarter, driven by robust growth in the retail loan portfolio, even as the legacy AUM continued to decline. However, this was largely offset by healthy recoveries from the AIF book. Asset quality remained largely stable across segments, while the retail opex ratio continued to show improvement.

* Our earnings estimates for FY26 and FY27 factor in gains from the AIF exposures, deferred consideration of USD120m from the sale of Piramal Imaging, and zero tax outgo in the foreseeable future. Because of the uncertainty and unpredictability around the timing of the monetization of the stake in Shriram Life and General Insurance, we have not factored it into our estimates yet. It will, however, provide one-off gains, which can help offset the credit costs required to dispose of the stressed legacy AUM.

* We expect PIEL to deliver ~1.2% RoA and ~5% RoE in FY27E. We value the lending business at 0.7x Mar’27E P/BV and reiterate our Neutral rating on the stock with a revised TP of INR1,085 (premised on Mar’27E SOTP).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412