Neutral Jyothy Laboratories Ltd for the Target Rs. 375 by Motilal Oswal Financial Services Ltd

Subdued performance; commentary remains muted

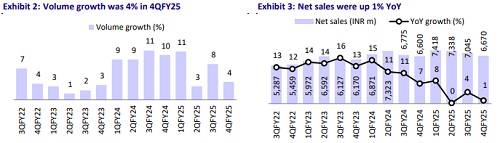

* Jyothy Laboratories (JYL) reported 1% YoY sales growth (below our est.) in 4QFY25. Volume growth was 4% (est. 7%, 8% in 3QFY25). The gap between volume and value growth was due to higher grammage and promotional price subs in select categories.

* Fabric Care delivered 2% value growth (led by liquid detergents), EBIT margin contracted by 60bp YoY to 22.4%, and EBIT declined by 1% YoY. Liquid detergent saw strong growth (20-25%), but the mix is small for JYL as of now. Segment EBIT margin can be 23-24% in the medium term.

* Dishwash posted 3% YoY growth, EBIT margin was flat, and EBIT grew 4% YoY. Large packs of Pril saw good momentum in MT, QC, and ECommerce. Both key brands—Exo Bar and Pril Liquid—delivered doubledigit volume growth in 4Q and FY25.

* HI remained weak and clocked 5% YoY revenue decline, primarily driven by the Coil sub-category. Liquid Vaporizer sub-category continued to register healthy growth. EBIT margin stood at -7% from -10.4% YoY.

* Personal Care continued to disappoint as revenue declined 9% due to a high base and overall softness in soaps. EBIT margin improved 210bp YoY to 10.6%.

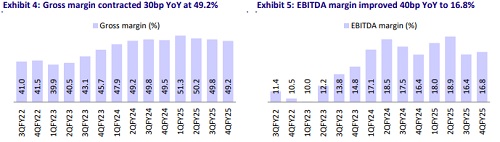

* Gross margin (GM) contracted 30bp YoY to 49.2% (est. 49.5%). JYL’s focus on cost management and calibrated pricing actions enabled it to improve the EBITDA margin by 40bp YoY to 16.8%. EBITDA grew 3% YoY.

* We estimate a CAGR of 8%/9% in revenue/EBITDA during FY25-27E. However, sustaining the operating margins will be challenging due to relatively slow revenue growth and competitive pressure. Going forward, market share gains and the success of new launches will be crucial for JYL’s earnings growth. We reiterate our Neutral rating on the stock with a TP of INR375 (premised on 30x FY27E P/E).

Miss across parameters; 4QFY25 volume growth at 4%

* Volume growth stood at 4%: JYL net sales rose 1% YoY to INR6,670m (est. INR6,944m). Volume growth was 4% (est. 7%) in 4QFY25. Fabric care and dishwashing saw low-single-digit growth, while HI and personal care remained on a declining trajectory.

* Low ad spends support EBITDA margin: Gross margin contracted 30bp YoY to 49.2% (est. 49.5%). As a percentage of sales, staff costs increased 70bp YoY to 11.7%, other expenses fell 40bp YoY to 12.7%, and ad-spends were down 100bp YoY at 8%. EBITDA margin improved 40bp YoY to 16.8%. (est. 16.7%).

* Miss on profitability: EBITDA grew 3% YoY to INR1,119m (est. INR1,159m). PBT grew 4% YoY to INR1,112m (est. INR1,135m). Adj. PAT grew 3% YoY to INR806m (est. INR845m).

* In FY25, net sales/EBITDA/APAT grew by 3%/4%/4%.

Highlights from the management commentary

* While rural demand showed relative improvement in 4Q, it was not sufficient to offset the continued weakness in urban consumption. Higher spends on healthcare, rents, etc. are impacting urban wallet share. Urban demand is expected to stay subdued in 1HFY26 due to macroeconomic pressures.

* The company expects volume growth in 1HFY26 to be in mid-single digits, while it is expected to be in double digits in 2HFY26.

* Washing powder and liquid detergent have a cumulative market size of INR350b, growing at 6-7% YoY. Of which, liquid detergent is expected to be an INR30b market, growing at 20-25% YoY as per JYL.

* The company maintained its EBITDA margin guidance at 16-17% for FY26. 1HFY26 would have slightly higher margin pressure; situation to improve 2HFY26 onward.

Valuation and view

* We cut our EPS estimates by 4% each for FY26E and FY27E.

* We believe that subdued demand sentiment, high RM cost inflation and elevated competitive intensity could limit JYL’s growth in the near term. From hereon, market share gains and the success of new launches will be critical for JYL’s earnings growth. JYL’s margin expansion beyond ~18% is also constrained by its focus on the mass and rural segments. Therefore, we believe its growth potential is adequately priced in at the current valuation. We reiterate our Neutral rating on the stock with a TP of INR375 (premised on 30x FY27E P/E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412