IPO Note : Powerica Ltd by Geojit Investments Ltd

Established Diesel Generator Player with Emerging Renewable Portfolio

Powerica Ltd, founded in 1984, is an integrated power solutions provider focused on diesel generator sets (DG sets) for primary and standby power. A long-standing OEM partner of Cummins India, the company also operates in the medium speed large generator (MSLG) segment through a collaboration with HD Hyundai Heavy Industries. The company manufactures generator sets ranging from 7.5 kVA to 10,000 kVA across its Bengaluru, Silvassa, and Khopoli plants. Powerica has diversified into renewables with 330.8 MW of wind assets in Gujarat and also offers emission control solutions via its associate, Platino Automotive.

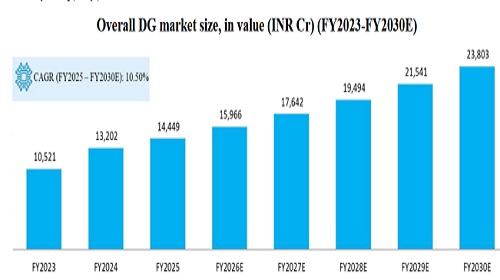

* The DG market in India has grown at a 17% CAGR over the past two years, reaching Rs14,449cr in FY25, and is expected to grow at a 10% CAGR to Rs23,803cr by FY30, supported by infrastructure development, telecom expansion, industrial growth, and data centers. (Source: Frost & Sullivan analysis)

* Powerica recorded topline growth of 5.6% CAGR, reaching Rs2,653cr in FY25 from FY23, driven by steady orders from clients due to long-standing partnership with key OEMs and growth in the wind business.

* Margins contracted by 190 bps from FY23, settling at 12.7% in FY25 for the overall business, with DG sets at 8.3% due to rising input costs and competitive pricing pressure, while margins in the wind business remained stable at 41.0%.

* PAT grew strongly at a 28.6% CAGR, reaching Rs177cr in FY25 from Rs106cr in FY23, supported by topline growth, lower finance costs, and reduced depreciation.

* Powerica's strong technical depth and integrated operations drive quality and cost efficiency, supported by credible OEM partnerships. DG demand remains steady on power deficits and infrastructure growth, while renewables offer policy-led higher-margin diversification.

* The planned debt repayment of Rs525cr from the IPO proceeds will result in substantial savings on interest costs (D/E will reduce from 0.5x to 0.0x), which should also result in an increase in PAT.

* At the upper price band of Rs395, Powerica is valued on adj. P/E of an 28x for FY25 EPS and 19x for FY26E EPS annualized. The company’s topline has improved momentum in H1FY26, with strong demand visibility for DG sets driven by data centers and rising power demand. Its wind energy business provides higher-margin potential, and strong relationships with global players further enhance growth prospects. With healthy ROE of 17.5% and an improved D/E ratio, the balance sheet should be able to support project execution in the wind sector. Hence we assign a Subscribe rating for a long-term investment horizon.

Purpose of IPO

The offer consists of a fresh issue of Rs.700cr and an Offer for Sale (OFS) amounting to Rs.400cr. The purpose of the issue is to i) Repayment/prepayment of certain borrowings and related penalties (Rs.525cr) and ii) remaining for general corporate purposes.

Key Risks

* Segment concentration risk, DG set business contributes 80% of revenue as of H1FY26 therefore any slowdown may significantly impact performance.

* Heavy reliance on Cummins India Ltd and Hyundai Heavy Industries Ltd as suppliers as business with them makes up entire DG set segment revenue.

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer

SEBI Registration Number: INH20000034