IPO Note :OnEMI Technology Solutions Ltd by Geojit Investments Ltd

High Growth Digital Lender with Strong Returns

OnEMI Technology Solutions Ltd (OnEMI), incorporated in 2016 is a technologyenabled lender in India, primarily offering digital loans through its mobile application for various consumption and business needs. The company operates under the brand names Kissht (digital lending platform) and Ring (payments app), OnEMI empowers online and offline merchants with seamless consumer credit solutions and EMI-based payments. Its NBFC partner, Si Creva Capital Services, handles loan disbursement, KYC, and EMI collections.

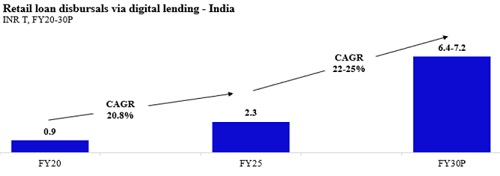

* As of FY25, India’s retail loan disbursal via digital lending stood at Rs.2.3tn and grew at a CAGR of 21% from FY20. The segment is expected to grow at a CAGR of 22–25% till FY30, with growth driven by the younger generation and rising household earnings (Source: 1Lattice analysis).

* OnEMI’s total AUM grew at a 64% CAGR from FY23 to 9MFY26, reaching ?5,956cr as of December 31, 2025, with ~49% comprising off-book loans held by third-party financial institutions.

* OnEMI served 11.2 million customers as of 9MFY26, reflecting a 20% CAGR from FY23, with repeat customers contributing ~51% of AUM, indicating strong customer retention and engagement.

* Driven by consistent growth in AUM, a large customer base, and higher lending rates, OnEMI achieved a Return on Assets (RoA) of 7.1% and a Return on Average Equity (RoE) of 17.7% for FY25, higher than the peer average.

* OnEMI’s asset quality remained strong as of December 2025, with GNPA at 2.9% and NNPA at 0.4%, ranking fourth lowest and lowest among NBFC peers, respectively.

* As of December 2025, OnEMI reported a spread of 15.3%, among the highest in its peer group. Its expansion into Loan Against Property (LAP) via offline branches supports diversification of the liability mix, while a strong capital position (CRAR of 21.1%) provides a solid buffer for growth.

* At the upper price band of Rs.171, OnEMI is valued at ~1.4x P/B (post-issue), which appears fairly priced relative to peers while factoring in inherent risks. Backed by strong growth in AUM and customer base, an omnichannel model, and a rapidly expanding digital lending ecosystem in India, the company is well positioned to scale. We therefore recommend a “Subscribe” rating for high-risk investors for a short to medium term.

Purpose of IPO

The offer consists of a fresh issue of ?850cr and OFS (offer for sale) of ?76cr, totalling an issue size of ?926cr. The net proceeds of ?638cr from the fresh issue will be utilized to augment the capital base of subsidiary Si Cerva to meet its future capital requirements arising out of the growth of subsidiary business and the rest for general corporate purposes.

Key Risks

* Unsecured loans form a majority of AUM (94.2% as of December 31, 2025), making the business sensitive to demand fluctuations.

* As of December 31, 2025, contingent liabilities totalled Rs.1,793.49 crore, which may impact financial performance if realized.

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer

SEBI Registration Number: INH20000034

.jpg)