Buy Prataap Snacks Ltd for the Target Rs. 1,350 by Motilal Oswal Financial Services Ltd

Volume led revenue growth; expect turnaround in margins

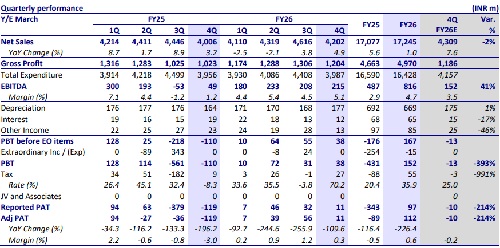

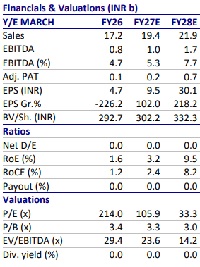

Prataap Snacks’ (PSL) revenue grew 4.9% YoY to INR4.2b in 4QFY26, led by volume growth. Namkeen Snacks outperformed with double digit volume, followed by Potato Chips and Extruded Snacks. PSL undertook ~6-8% grammage reduction (coming at pre-GST level) due to higher inflation of ~9%. Management expects double-digit revenue growth over the next few years, backed by higher growth in Namkeen, followed by Extruded Snacks. Gross margin expanded 310bp YoY to 28.6% for 4QFY26, led by a favorable product mix, while EBITDA margin settled at 5.1% (+390bp YoY). We expect margins to expand further to ~7.7% by FY28, led by cost optimization. We expect PSL’s revenue growth to continue at ~12-13%, led by: 1) a shift from a three-tier distribution to a two-tier model, 2) consolidating plants into one automated facility by FY28, 3) transition from third-party to owned plants in North India, and 4) the addition of new lines for snacks in East India, which helps reduce freight costs.

Steady top-line growth led by the Ethnic portfolio

PSL’s revenue grew 4.9% YoY to INR4.2b in 4QFY26, backed by a deeper technology footprint, which has strengthened execution and enhanced market responsiveness, expansion in distribution network, and stronger presence in emerging channels. Namkeen Snacks outperformed with double digit volume, followed by Potato Chips and Extruded Snacks. Rings witnessed double-digit negative growth, while Chulbule declined marginally. Newly launched product variants continued to gain traction, while the company is also driving sales of higher pack sizes across select categories. PSL undertook ~6-8% grammage reduction (coming at pre-GST level) due to higher inflation of ~9%. Thus, we expect another round of price hikes toward the end of 1QFY27 to fill the gap.

Margin expands on a low base and favorable product mix; expect improvement in H2FY27

In 4Q, gross margin expanded 310bp to 28.6% YoY and 40bp QoQ, led by a favorable product mix. EBITDA grew 333.6% to INR215m, with EBITDA margin at 5.1% (+390bp YoY), despite an increase in employee expenses (+14% YoY). APAT grew 109.6% to INR11m. During this quarter, ~10% inflation has been observed due to higher palm oil (~18-20% of sales), packing material (~15-16% of sales), and corrugated boxes (~7% of sales) prices. We expect some margin pressure in 1HFY27, followed by a turnaround, with margins likely to expand to ~7.7% by FY28.

Valuation and view: Reiterate BUY

PSL experienced a period of underperformance despite favorable industry conditions; however, we believe the company is likely to deliver strong financial performance ahead. During 4Q, the Board also proposed a dividend of 10% per share on a face value of INR5 each, translating to INR0.50 per share. We estimate a CAGR of 13% in revenue and 42% in EBITDA over FY26-28, driven by volume growth and significant margin expansion. We reiterate our BUY rating with a DCFbased TP of INR1,350 (based on an implied P/E of 45x on Mar’28E). Key risks: potential supply chain disruptions impacting production and execution risks related to plant consolidation (refer to our IC note dated Sep’25).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412