Buy Varun Beverages Ltd for the Target Rs. 600 by Motilal Oswal Financial Services Ltd

Strong volume drives revenue growth

Earnings above our estimates

* Varun Beverages (VBL) posted a strong quarter with ~16% YoY volume growth, led by strong volume growth of 14.4% in India and 21.4% in international territories. Further, net realization per case improved 1.6% at the consolidated level, fueled by realization growth in international territories (due to favorable currency movement), which was partially offset by 1.5% dip in net realizations in India (due to pack upsizing and targeted price-point launches).

* Going forward, VBL is well placed for healthy 2QCY26 growth due to the El Niñoled heatwave, along with tailwinds from the Twizza and Crickley consolidations.

* Factoring in the consolidation of Twizza and Crickley and higher-thanexpected volumes, we raise our CY26/CY27 earnings estimates by 4%/6%. We reiterate our BUY rating with a TP of INR600 (based on 47x CY26E EPS).

Healthy all-round operations lead to margin expansion

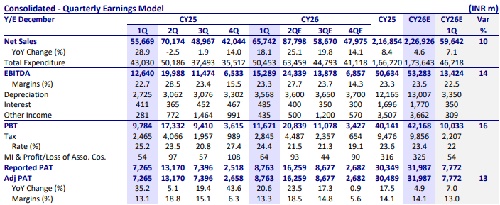

* Consol. revenue grew 18% YoY to INR65.7b (est. INR59.6b) on account of 16% YoY growth in volume to 363m cases and an improvement in realization per case by 1.6% to INR174.

* EBITDA margin expanded ~60bp YoY to 23.3% (est. 22.5%). EBITDA per case grew 12% YoY to INR45.3. EBITDA rose 21% YoY to ~INR15.3b (est. INR13.4b).

* Depreciation increased 30.9% due to the commissioning of new plants of last year (Buxar, Prayagraj, Damtal, and Meghalaya), which were not present in the base quarter. Further, finance costs increased 18% on account of the acquisition of Twizza in South Africa in the current quarter. The income from surplus cash in India is accounted for as other income. Adj. PAT grew 21% YoY to INR8.8b (est. INR7.7b). * The subsidiary’s (consolidated minus standalone) revenue/EBITDA/adj. PAT jumped 36%/3x/16x YoY to INR22.1b/INR8.3b/INR7.8b in 1QCY26.

* CSD/Juice/Water volumes grew 74%/7%/19% YoY to 268m/27m/68m units in 1QCY26.

Highlights from the management commentary

* Packaging: VBL’s aluminum can beverage sales are less than 2%. The company is managing rising costs by cutting discounts. The packaging inventory is covered until next quarter for the domestic market and until the next two quarters for international markets. The shortage of aluminum cans is affecting the energy drinks portfolio, due to which the company is shifting to PET bottles.

* Guidance and outlook: The company remains bullish on domestic demand with no expected adverse impact from inflation. Strong traction in new launches such as Nimbooz (~60% growth) and Tropicana (100% growth), along with the anticipated El Niño-led heatwave, is expected to further boost beverage consumption and support a strong near-term outlook.

* Strategic acquisition: VBL consummated the acquisition of Twizza (9MCY26 revenue of INR8b) through BevCo at EV of ZAR2b (INR11,187m), strengthening its manufacturing footprint. VBL also acquired Crickley Dairy (9MCY26 revenue of INR1.6b) through BevCo at EV of ZAR238m (INR1314.68m), further strengthening its presence in South Africa.

Valuation and view

* We expect VBL to witness improved earnings momentum, aided by an extreme heatwave expected this year due to El Niño conditions (to aid in peak season demand); 2) a scale-up in the international market, driven by South Africa and recovery in the Zimbabwe market; 3) strengthening of on-ground execution in the Indian market; 4) scale-up of the snacking business, backed by the operationalization of the Morocco and Zimbabwe markets in 2HCY25; and 5) an expanding product portfolio (recently launched an energy drink known as ‘Adrenaline Rush’).

* We expect a CAGR of 16%/16%/20% in revenue/EBITDA/PAT over CY25-27. We increase our CY26E/CY27E earnings estimates by 4%/6% and reiterate our BUY rating on the stock with a TP of INR600 (47x CY26E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412