Buy Indostar Capital Finance Ltd For Target Rs.290 Motilal Oswal Financial services Ltd.

Pick up in business momentum; guides for earnings stability ahead Elevated SR provisions led to reported losses, but provisioning now complete

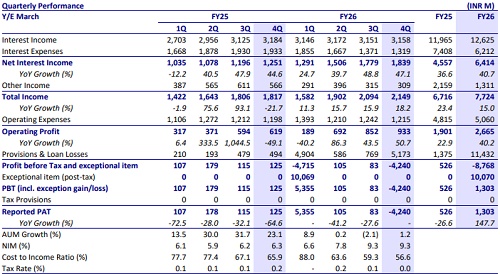

Indostar Capital Finance (INDOSTAR) reported a mixed operating performance during the quarter, with a pickup in business momentum, as evident in the sequential improvement in both disbursements and AUM growth. However, the company reported losses in the quarter due to elevated credit costs from additional management overlay and one-time provisioning on the SR book. Further, asset quality weakened during the quarter, as GS3 rose ~70bp QoQ, due to slippage from the legacy loan book.

Key highlights:

1) Disbursements declined 15% YoY and grew 17% QoQ to ~INR13.1b; AUM grew 1% YoY and grew 5% QoQ to ~INR80.6b

2) Asset quality deteriorated with GS3 rising ~70bp QoQ

3) NIM (calc.) was stable sequentially

4) The company recognized an additional one-time provision of ~INR3.3b on the SR book, along with a management overlay of INR490m as a prudent measure in light of uncertainties arising from the ongoing West Asia conflict.

Valuation and View

* INDOSTAR reported a mixed operating performance during the quarter, with sequential improvement in both disbursements and AUM growth. However, profitability remained impacted by elevated credit costs arising from additional management overlays and one-time provisioning on the SR book. Further, asset quality weakened during the quarter, as GS3 increased owing to higher delinquencies within the legacy loan book.

* INDOSTAR has prioritized the expansion of its loan book in the used CV segment and micro-LAP. A reinforced management team, enhanced processes, opex rationalization, and improved underwriting processes leading to better asset quality are expected to drive an improvement in profitability ratios in the coming years. We expect RoA of the company to expand to 2.7% by FY28E with PAT CAGR of ~62% over FY26-28E. Reiterate a BUY rating on the stock with a TP of INR290 (premised on 1.1x Mar’28E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041