Neutral P&G Hygiene and Healthcare Ltd For Target Rs.11,000 Motilal Oswal Financial services Ltd

Subdued quarter with an all-round miss

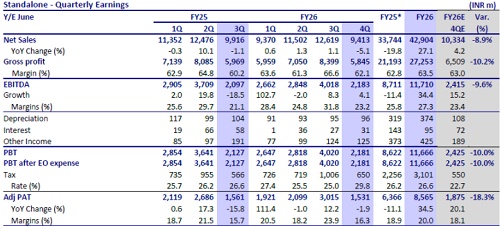

* P&G Hygiene and Healthcare’s (PGHH) 4QFY26 revenue declined by 5% YoY (miss). In the last four quarters, the revenue growth trajectory has been flat.

* Gross margin expanded 190bp YoY but contracted 450bp QoQ to 62.1%, reflecting the usual volatility between quarters. Employee costs rose 15% YoY, A&P was up 9% YoY, and other expenses fell 18% YoY. EBITDA margin expanded 200bp YoY but fell 870bp QoQ to 23.2%. EBITDA grew 4% YoY to INR2.2b (est. INR2.4). PGHH delivered 17% EBITDA growth in the last four quarters.

* PGHH exhibits significant volatility on a quarterly basis, but its annual performance remains stable. We model 27.0-27.5% EBITDA margin during FY27 and FY28.

* We model a CAGR of 8% each in revenue/EBITDA/PAT over FY26-28E. Given the volatility in margins, we find other consumer names relatively better than PGHH for the growth outlook at valuation it offers. We maintain Neutral with a revised TP of INR11,000 (based on 35x Mar’28E EPS).

Miss on all fronts; revenue down 5%

* Revenue down 5%: PGHH registered 5% YoY decline in revenue to INR9.4b (est. IN10.3b). Revenue growth has been weak for the last few quarters.

* Volatile quarterly margins: Gross margin expanded 190bp YoY to 62.1% (est. 63%). GM volatility between quarters is always high. Employee costs rose 15% YoY, A&P was up 9% YoY and other expenses fell 18% YoY. EBITDA margin expanded 200bp YoY to 23.2% (est. 23.4%).

* Muted profitability: EBITDA grew 4% YoY to INR2.2b (est. INR2.4b). PBT grew 3% YoY, while adj. PAT declined 2% YoY to INR1.5b (est. INR1.9b).

Valuation and view

* We cut our EPS estimates by 3-4% for FY27 and FY28.

* Two factors make PGHH an attractive long-term core holding:

1) High growth potential for the feminine hygiene segment, coupled with the potential for market share gains and strategic initiatives, including the strengthening of its competitive advantages

2) the potential to sustain high operating margins from the long-term premiumization trend in the feminine hygiene segment.

* With a portfolio of essentials and healthcare, PGHH remains focused on product innovation-led customer acquisition. While penetration play will continue, it is expected to proceed at a stable pace despite the high scope of user additions. Further, we do not see any medium-term upside trigger.

* We model a CAGR of 8% each in revenue/EBITDA/PAT over FY26-28E. Given the volatility in margins, we find other consumer names relatively better than PGHH for the growth outlook at valuation it offers. We maintain Neutral with a revised TP of INR11,000 (based on 35x Mar’28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)