Buy Sapphire Foods Ltd for the Target Rs. 220 by Motilal Oswal Financial Services Ltd.

KFC recovery underway; limited impact from LPG disruptions

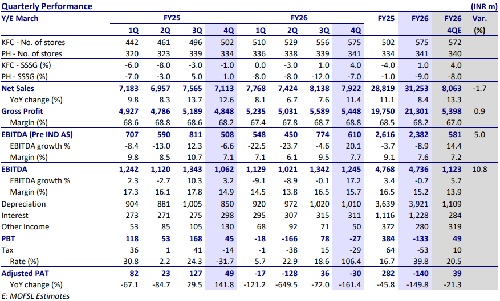

* Sapphire Foods India (SAPPHIRE) reported a revenue growth of 11% YoY (in line) in 4QFY26. KFC sales grew 15% YoY with an SSSG of 4% (est. 4%; ex-Navratri: 6%). Pizza Hut (PH) franchise remained weak, with its revenue dipping 6% YoY as same-store sales declined 7% (est. -8%). In contrast, Sri Lanka posted healthy revenue growth of 16% YoY (+15% in LKR), driven by 11% LKR SSSG and 7% store growth.

* Demand trends in KFC are improving despite LPG shortages and ongoing inflationary pressures. April 2026 demand remained in line with 4QFY26 trends. The company implemented a ~2% price hike across KFC and Pizza Hut in April and does not expect any further price increases in the near term. Despite LPG supply disruptions in March, no KFC stores were shut, although select outlets operated with limited menus or reduced timings. A few stores of PH (less than ~5% of total PH stores) remained closed for 10-15 days in Mar’26, which narrowed to 3% in Apr’26.

* KFC’s ROM expanded 110bp YoY to 16.8% (est. 15.4%), supported by better GM (subsidized RM from vendor partners). PH’s ROM was -6%. (est. -6.2%, -3.3% in FY26). Sri Lankan ROM contracted 20bp YoY to 14.6%. At the company level, EBITDA (Pre-Ind-AS) was up 20% YoY to INR610m, with a 60bp expansion in margin to 7.7% (est. 7.2%). Management highlighted that despite a sharp 25-40% increase in LPG prices, their impact on EBITDA was limited to 30-50bp.

* The weak unit economics have been a big concern for QSR players over the last two years, given fast store expansion. However, KFC’s performance is showing an improving trajectory, supported by its twopronged consumer recruitment strategy, though we need to monitor the sustainability of this trend. Further, the Devyani–SAPPHIRE merger is expected to unlock scale benefits and strengthen execution across brands and geographies. SAPPHIRE expects the merger to be completed by FY27, with CCI approval likely within the next 35-40 days. We reiterate our BUY rating on the stock with a TP of INR220 (based on 18x Mar’28E pre-IND-AS EV/EBITDA).

Operational beat; KFC’s SSSG and margins improve

* KFC shines; PH remains a drag: Consolidated sales grew 11% YoY to INR7.9b (est: INR8.1b). KFC revenue grew 15% YoY (in line) to INR5.5b with samestore sales rising 4%. Ex-Chaitra Navratri, SSSG was 6%. KFC’s ADS grew 1% YoY to INR109K. PH’srevenue declined 6% YoY (est. -9%) to INR1.2b with same-store sales declining 7%. PH’s ADS decreased 7% YoY to INR39K. PH in Tamil Nadu continued to grow in double digits, backed by mass media advertising. Sales in Sri Lanka grew 16% YoY (+15% in LKR terms) to INR1.2b, and SSSG was 11% in LKR terms. ADS grew 9% YoY to INR104k.

* Store additions on expected lines: The number of stores grew 9% YoY to 1,052. It added a net of 24 stores in the quarter (19 KFC, 2 PH, and 3 in Sri Lanka).

* KFC improves operating margins: Consolidated gross profit grew 12% YoY to INR5.4b (est. INR5.4b). Consolidated GM expanded marginally 60bp YoY to 68.8% (est. 67%). Reported EBITDA margin expanded 80bp YoY to 15.7% (est. 13.9%). EBITDA grew 17% YoY to INR1.2b (est. INR1.1b). Consolidated ROM (PreInd-AS) expanded 100bp YoY to 13%. EBITDA (Pre-Ind AS) margin expanded 60bp YoY to 7.7% (est. 7.2%). EBITDA (Pre-Ind AS) grew 20% YoY to INR610m (est. INR581m).

* Loss before tax was INR27m vs. a profit of INR45m in 4QFY25.

* Loss after tax was INR30m vs. a profit of INR49m.

* In FY26, net sales grew 8%, while EBITDA declined 1%.

Highlights from the management commentary

* KFC’s performance was driven by the two-pronged consumer recruitment strategy. In evolving chicken-consuming markets (North & West), the marketing mix involves recruitment advertising with a strong value call to action (INR99 Chicken Krisper Burger Meal). In more developed chicken-consuming markets (South), they offered disruptive, abundant value on select days.

* PH Tamil Nadu continues to deliver positive double-digit SSSG and restaurant EBITDA performance over the rest of the country.

* In Sri Lanka, the business continued to deliver strong performance under the same dine-in-forward omni-channel strategy, supported by consistent innovation and marketing investments.

* The merger can take 12 months (from the date of announcement) to be completed; until then, both companies will continue to function independently. The management further alluded that it expects SEBI approval to come in within the next 30-45 days, following which it will go to NCLT for the merger and also seek CCI. SAPPHIRE expects the merger to be completed by the end of FY27.

Valuation and view

* We increase our EBITDA estimates by 3-4% for FY27 and FY28.

* The ongoing LPG shortage and inflationary pressures have had a limited impact on SAPPHIRE, with a 25–40% increase in LPG prices translating into a ~30–50 bps impact on EBITDA margins. There were no store closures for KFC, while Pizza Hut witnessed temporary closures in a small portion of stores (~3% of total PH stores). The company also implemented a ~2% price hike across both KFC and Pizza Hut. Sri Lanka is delivering double-digit revenue growth.

* The weak unit economics have been a big concern for QSR players over the last two years, given fast store expansion. However, KFC’s performance is improving, supported by its two-pronged consumer recruitment strategy, though we need to monitor the sustainability of this trend. Further, the Devyani–SAPPHIRE merger is expected to unlock scale benefits and strengthen execution across brands and geographies. SAPPHIRE expects the merger to be completed by FY27, with CCI approval likely within the next 35–40 days. We reiterate our BUY rating on the stock with a TP of INR220 (18x Mar’28 pre-IND-AS EV/EBITDA).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041